Monetary & Fiscal Dominoes at the ready.

Macro Perspectives

Yesterday we talked about an important dissent at the Fed, with the San Francisco Fed President being the first to push back against the tide of Fed voices that have, for the better part of the past year, relentlessly promoted the idea of suffocating the economy with higher and higher rates.

That's the monetary policy side. On the fiscal policy side, similarly, we've had two years of unrestrained transformational policy execution in Washington, with virtually no dissenting voice. That's changing too.

The next two years, with a divided Congress, we will get gridlock on Capitol Hill, and, as important, we will get scrutiny of the excesses of the past two years. That scrutiny will likely come in the form of investigations and legal challenges to Biden's executive orders.

The question is: How many dominoes will fall?

For markets and the economy, probably the more the merrier (as it will dampen the destabilising overreach).

We are just two weeks removed from the midterms, and already:

The Biden student loan cancellation has been blocked by a federal judge, as unlawful. This cools the inflation outlook, as it removes the prospects of half a trillion dollars worth of consumer liabilities, being freed up to become consumption.

We have several dominoes falling that are deconstructing the abused power dynamic in DC. CBS News has suddenly (after two years, and just after the midterm elections) found it quite easy to verify the validity of the Hunter Biden laptop, which is said to implicate the President in corrupt business dealings.

The private cryptocurrency market is unravelling. As I’ve said throughout the years, here in my Macro Perspectives notes: "in its short history, Bitcoin has a record of being a tool of corruption and money laundering."

With the failure of the biggest crypto exchange, FTX, we're finding that the crypto market indeed looks like a tool of corruption and money laundering. At the very least, at this point, we know that the founder was heavily funding democrat political campaigns.

The question is, with whose money?

PS: If you, or anyone you know, would benefit from receiving actionable insights with the foundation of institutional grade models, click on the link below and join other decision makers taking control of their funds.

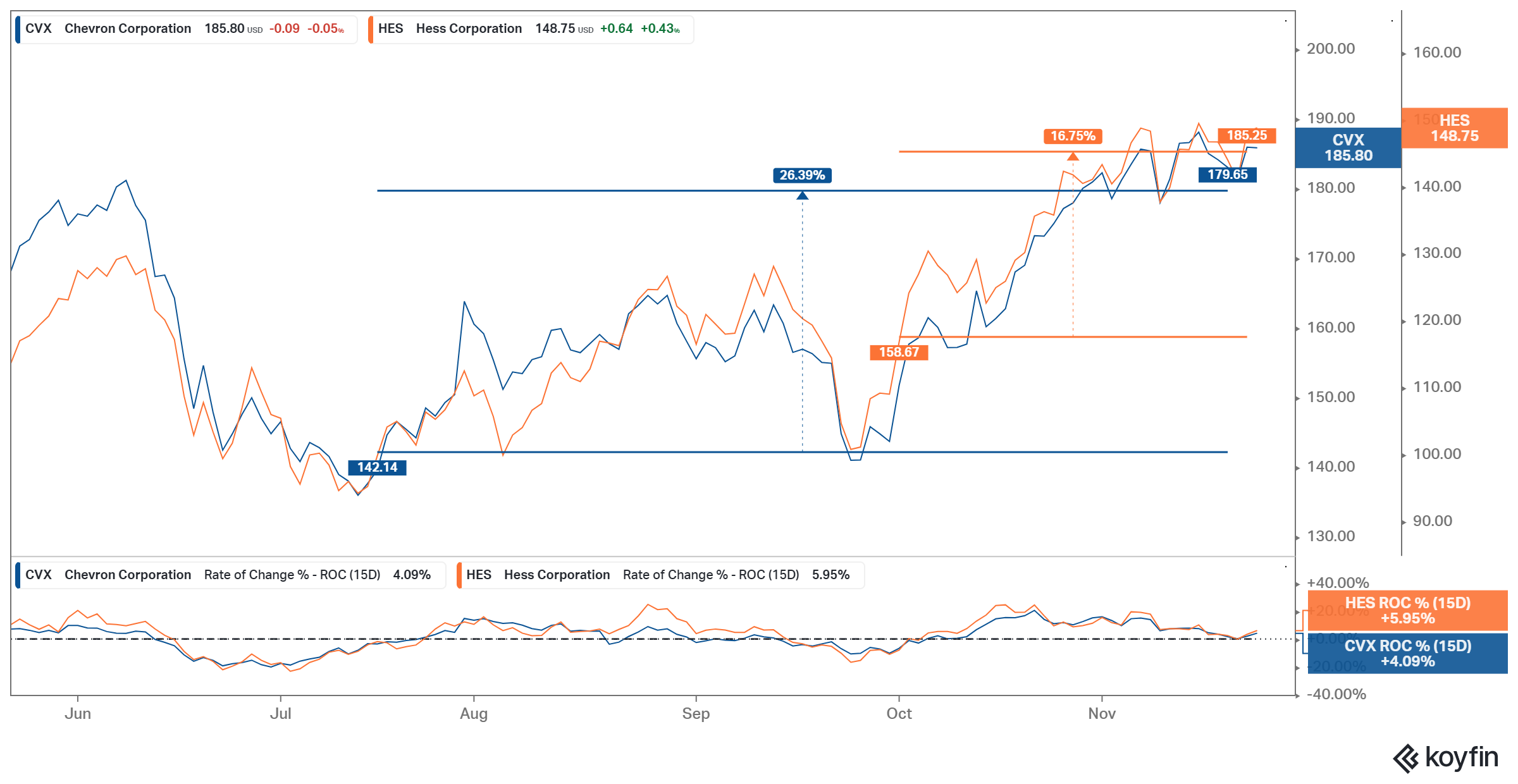

As an example, within the Uncorrelated Convexity portfolio, we recently closed out two positions in CVX 0.00%↑ and HES 0.00%↑ .

nb: the width of the %gain lines indicates trade duration.