Monetary Airbags

US stock futures edged higher on Friday, with the S&P 500 on track to snap a four-week losing streak.

The Dow also remained in positive territory for the week, while the Nasdaq Composite appeared set for a fifth consecutive weekly decline.

Fed Chair Jerome Powell sought to reassure markets by calling tariff-driven inflation "transitory," though concerns persisted.

Meanwhile, the Fed downgraded its economic growth forecast and raised its inflation outlook, stoking fears of stagflation.

In extended trading, Nike and FedEx tumbled 5.2% and 5.6%, respectively, following disappointing quarterly results.

From the 52-week high to the recent lows, the NASDAQ and S&P 500 traded down by over 10% in one of the fastest sell-offs in market history. Inflation and growth expectations changed principally in reaction to tariff announcements.

The Federal Reserve is projecting 2025 GDP growth of 1.5-1.9%, down from the December projection of 1.8-2.2%.

It sees PCE inflation of 2.6-2.9%, up from its prior projection of 2.3-2.6%.

The U.S. economy has a cash airbag to reduce the force of a potential economic blow - U.S. checking accounts have a balance of $5.3 trillion (as of end of 2024), up from $1.53 trillion at the end of 2019 (pre-Covid).

Funds in checking accounts are typically designated for near-term consumption. Bank of America’s CEO said last week that consumers are spending about 6% more this year than the same time last year.

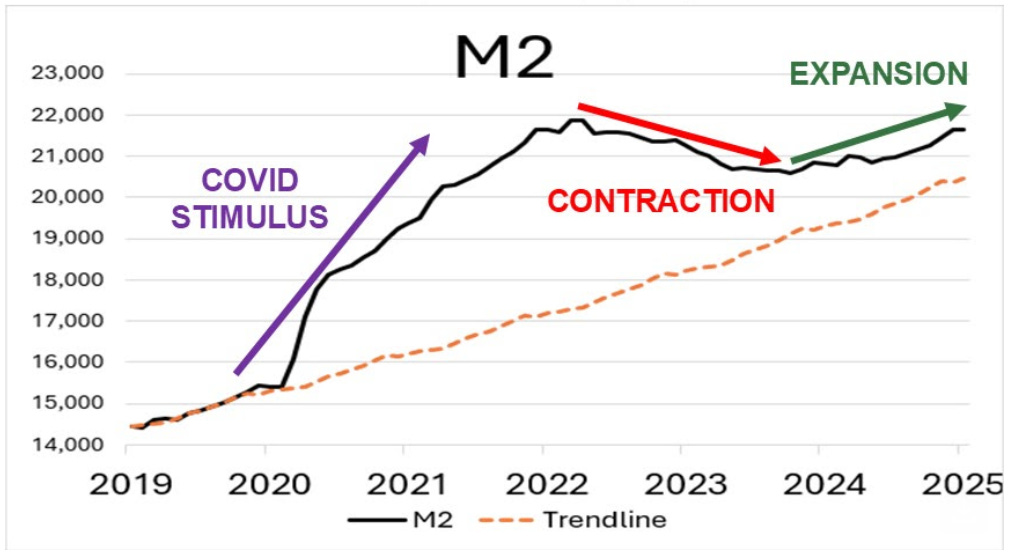

If you look at the combined balances of checking, savings and money market funds, the balance is $21.6 trillion, up from $14.8 trillion at the end of 2019.

There has been rising concern regarding consumer credit levels and default rates with automobile and credit card debt. Yet, household debt service as a percentage of disposable personal income is at a “normal” level relative to the past 45 years and consumer credit delinquencies remain at below “stressed” levels.

In addition to the cash airbag, the U.S. economy has an easy money liquidity airbag. The Federal Reserve announced last week it is slowing the pace of its quantitative tightening.

Monthly redemptions of treasury securities will be reduced from $25 billion to $5 billion.

This should ease financial conditions by keeping more money in the system. The money supply is rising at about a 4% annual rate.

More money in the system allows banks to make more loans. Banks are easing lending standards currently rather than making them more restrictive. Below are two examples showing banks making commercial and industrial loans to large and middle-market firms and auto loans easier to obtain. If banks were worried about rising delinquency rates and recession, they would not be making loans easier to obtain.

Fed Chairman Powell acknowledged that he doesn’t know anyone who has a lot of confidence in their economic forecast. On the other hand, the hard data (versus “soft” data like consumer confidence) suggests the economy is not headed for recession. Without a recession, stock market pullbacks of 10% are a buying opportunity.