Second only to the midterm elections, inflation and (related) Fed policy continue to be a key theme influencing the market and economic outlook.

On that note, we heard from the central figure in this theme, Jerome Powell, when he gave a prepared speech at the Brookings Institution, and took questions.

Unlike the very friendly post-FOMC Q&A sessions, where financial media tend to lob soft questions at Powell, in this Brookings environment, he's speaking to peers, and was questioned by market participants (banks, funds).

The outcome? Markets liked it.

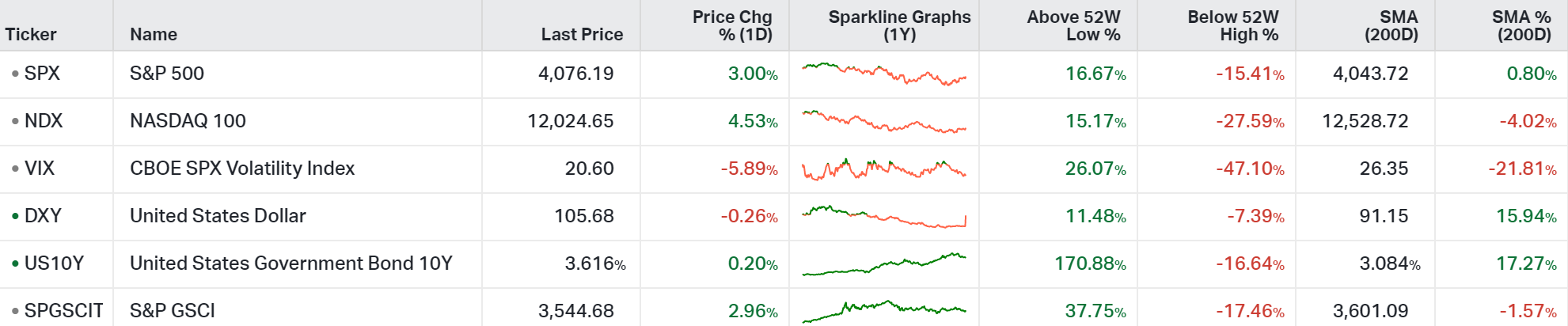

We've been watching this 200-day moving average in stocks (the purple line) . . .

. . . that broke yesterday. Not only do we get a close above this much looked at technical level, but it's the only close above the 200-day moving average since the Fed has been engaged in this rate hiking cycle.

And as you can see in the chart, we should get a test, over the next two days, of the downward sloping trendline (green line), which frames this Fed-induced drawdown in stocks.

In this world, where the Fed has been pursuing a weaker job market, a negative surprise in Friday's jobs report would be a positive catalyst for stocks. For clues, we can look at yesterday morning's ADP jobs report. It was weak. In fact, it showed the weakest job gains since the start of 2021. Again, bad news is good news.

So back to Powell. What did he say that markets responded so well to?

Mostly, that it now "makes sense to moderate the pace" of rate increases. Moreover, the "time for moderating the pace of rate increases may come as soon as the December meeting."

Now, in the Q&A session (where there's a chance for some candor to slip through the typically well measured words of the Fed chair), Powell said two very important things:

He said, "I don't want to over tighten." This is news. To this point, the Fed has told us they would err on the side of over tightening.

He said, it's "not appropriate (to execute some shock and awe strategy) to crash the economy and clean up afterwards." That's good news, given that their language to this point, has suggested that destroying the economy is precisely the strategy.

So, we enter December with some positive developments. As we've discussed in my notes, stocks historically do well in the twelve months following midterm elections. Now, add to this, the data is beginning to reflect the impact of the Fed's rate hikes, which should give the Fed impetus to take its foot off of the brakes on the economy.

Position yourself well for a rebound in stocks by joining us in my premium advisory service. Hit the button below for details ...