Weekly Market Signals

Performance of SIX trading strategies (more information); Tactical asset allocation, mean reversion, cross-sectional momentum, and equity long-short with weekly and monthly updating.

Performance of the six strategy ensemble and benchmarks

Comments

After a spike in geopolitical and political risks to unprecedented levels the previous week, a geopolitical event occurred, as expected. Commodities and gold rose, but the stock market reaction was not severe due to expectations of a quick resolution.

The S&P 500 index fell 1.1% due to the geopolitical conflict on Friday, June 13, 2025, while gold rose 1.3% to new, all-time highs, and crude oil gained more than 7%. Many traders expected the stock market to fall more on Friday, but defense and energy stocks provided solid support.

The ETF cross-sectional momentum strategy gained 1.5% on the week due to exposure in gold, and it is up 4.7% year-to-date. Despite a loss this week, asset cross-sectional momentum is still providing solid performance. Dow-30 long-short managed to stay slightly in the black this week, while Dow-30 mean-reversion experienced losses as soon as it became active again. Our plans for next year include a possible reduction of the exposure to mean reversion and an increase of the exposure to cross-sectional momentum and dynamic asset allocation. However, we will make the final decision later this year.

You can access everything the above strategies produce: trade alerts, market updates, and other informational content by clicking on the button below.

Daily Mean Reversion is one of the strategies that is available as part of the “One Solution, Multiple Benefits” ten (10) strategy rule pack (more information).

Daily Mean Reversion

The mean-reversion strategy uses our algorithm to generate long-only signals for two ETFs and now with S&P 100 stocks in the daily timeframe. The updates are typically available by 7:00 a.m. (ET) on weekdays.

Daily Mean Reversion | Performance with SPY and QQQ (ytd)

* 50% SPY ETF and 50% QQQ ETF

Daily Mean Reversion | Performance with S&P 100 stocks since March 24, 2025

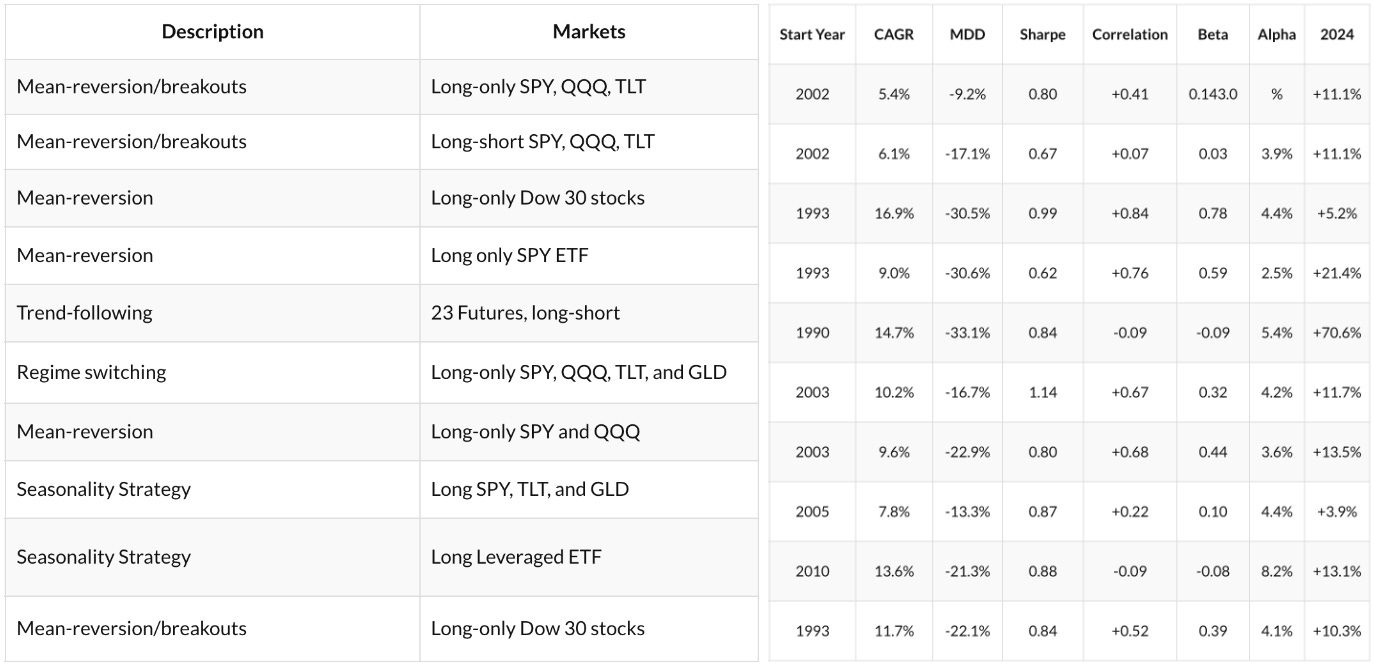

Summary Table | Ten Strategy Pack

The strategies we have developed are based on the following two principles: simplicity and economic value.

Simplicity reduces the probability of overfitting and data-mining bias. Economic value is necessary in the form of reasonable alpha and risk-adjusted returns.

The rules of 10 strategies are available for sale in a bundle. The rules we provide are sufficient for programming the strategies on a trading platform. The strategies are not data-mined and have simple rules.

Delivery: The trading rules are in the form of “private content” sent out via email seven days after payment.

Terms: We make no refunds on any purchase, and all sales are final. No refunds are given for cancellations or under any circumstances, and there is no exception.

Strategy code: We provide the rules in plain English. The customer will need to convert those rules to code before testing them on a backtesting platform.