Market Signals for Decemebr 16, 2024

Market recap, open positions, new signals, and performance of six trading strategies. Tactical asset allocation, mean reversion, cross-sectional momentum, and equity long-short with weekly and monthly updating. Access the full report with a GRYNING | Quantitative membership.

Performance of the ensemble and benchmarks

Weekly return of the ensemble: -1%

This week, the equity of the equally weighted strategy ensemble fell 1%.

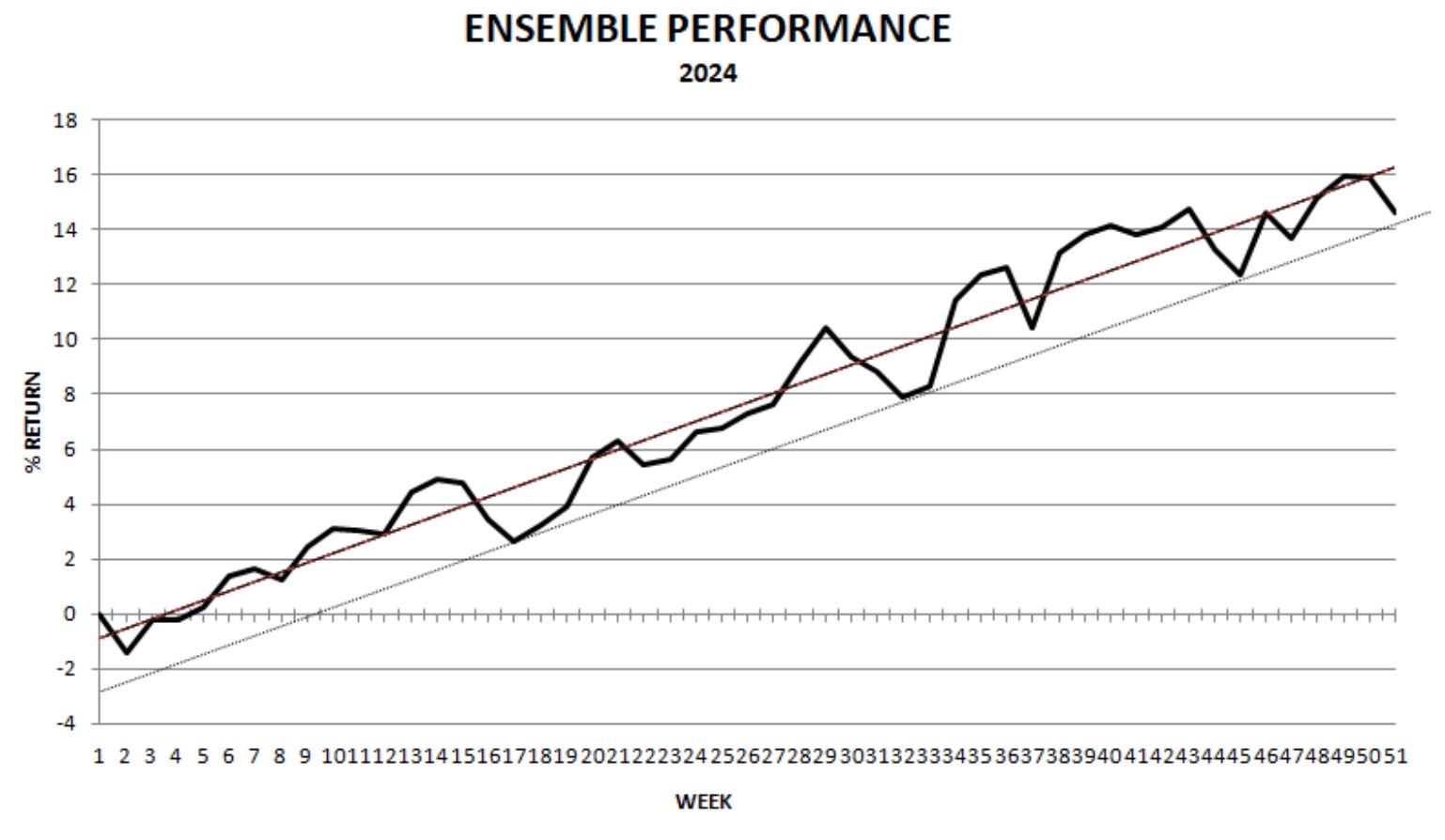

Year-to-date performance (Backtest, no leverage)

On a risk-adjusted basis, the ensemble outperforms both the SPY ETF and its equal-weight counterpart, the RSP ETF. At 2x leverage, the strategy ensemble outperforms the S&P 500 total return this year on both an absolute and risk-adjusted basis.

Recap and Comments (December 9–December 13, 2024)

This was a difficult week for systematic trading due to deteriorating breadth in the stock market and rising uncertainty. It could have gotten worse, but Dow-30 long-short provided a small convexity this week with a gain of 0.7%. Despite suffering a 2.6% weekly loss, Dow-30 mean-reversion remains the top-performing strategy with a 26.3% return year-to-date.

Regarding the Santa Rally in stocks, our analysis indicates that it has been more of an expectation or wish than a legitimate seasonal anomaly. See thoughts below for more details. Some doubts about massive reforms are surfacing, and the uncertainty may lead to increased volatility and further deterioration in stock market breadth. Simultaneously, the desire to sustain equity valuations appears to drive monetary policy, disregarding its potential impact on inflation. After realising this, the bond market fell this week and erased three weeks of gains.

As we near a potential change in administration, psychosis levels are increasing due to the potential for a “wealth redistribution.” Social media has witnessed the emergence of conspiracy theories, prompting rational investors to limit their exposure until the situation stabilises. We cannot make any forecasts, and we have long surrendered this intellectual activity to those who have abilities to predict the future. We hope the strategy ensemble will generate reasonable risk-adjusted returns and help us navigate changing market regimes, no matter what their drivers are.

For positions, strategy performance, and signal summary for next week, click on the button below.

Santa Rally?

The “Santa Rally” performance in the last 32 years has been mostly due to three outliers, in 1997, 2008, and 2018. Apart from those three outliers, the performance has been essentially stagnant. The long-term expectation is probably zero.

In this article, we define the Santa Claus Rally as a calendar effect anomaly in the stock market, where stock prices typically increase during the last week of December and the first two trading days of January.

Below is a chart of the Santa Rally performance in the S&P 500 index from 1992 to 2023 (including the first two days of 2024).

There are three outliers: 1997, 2008, and 2018. The last two were down years for the stock market. Below is the performance in table format.

The average performance of the Santa Rally in the last 32 years has been 0.67%. However, in the last 11 and 5 years, the performance has dropped to 0.37% and 0.32%, respectively.

Note that the average monthly performance of the S&P 500 since 1945 has been 0.72%. On average, the Santa Rally has not outperformed the monthly performance and has underperformed in the last 5 and 11 years.

Furthermore, if we remove the outliers in 1997, 2008, and 2018 by setting them to 0%, the average performance has been 0.18%.

Probably, in the limit of sufficient samples, the expectation from the Santa Rally converges close to 0% when adjusted by the monthly return performance. There’s no need to search for the causes of this calendar anomaly, as we believe there are none. This is simply a result of the limited sample size.