Market Signals for December 23, 2024

Market recap, open positions, new signals, and performance of six trading strategies. Tactical asset allocation, mean reversion, cross-sectional momentum, and equity long-short with weekly and monthly updating. Access the full report with a GRYNING | Quantitative membership.

We wish you and your family a Merry Christmas and a Happy New Year!

Thank you for being a reader The GRYNING Times. We are so honoured to have your time, attention, and support.

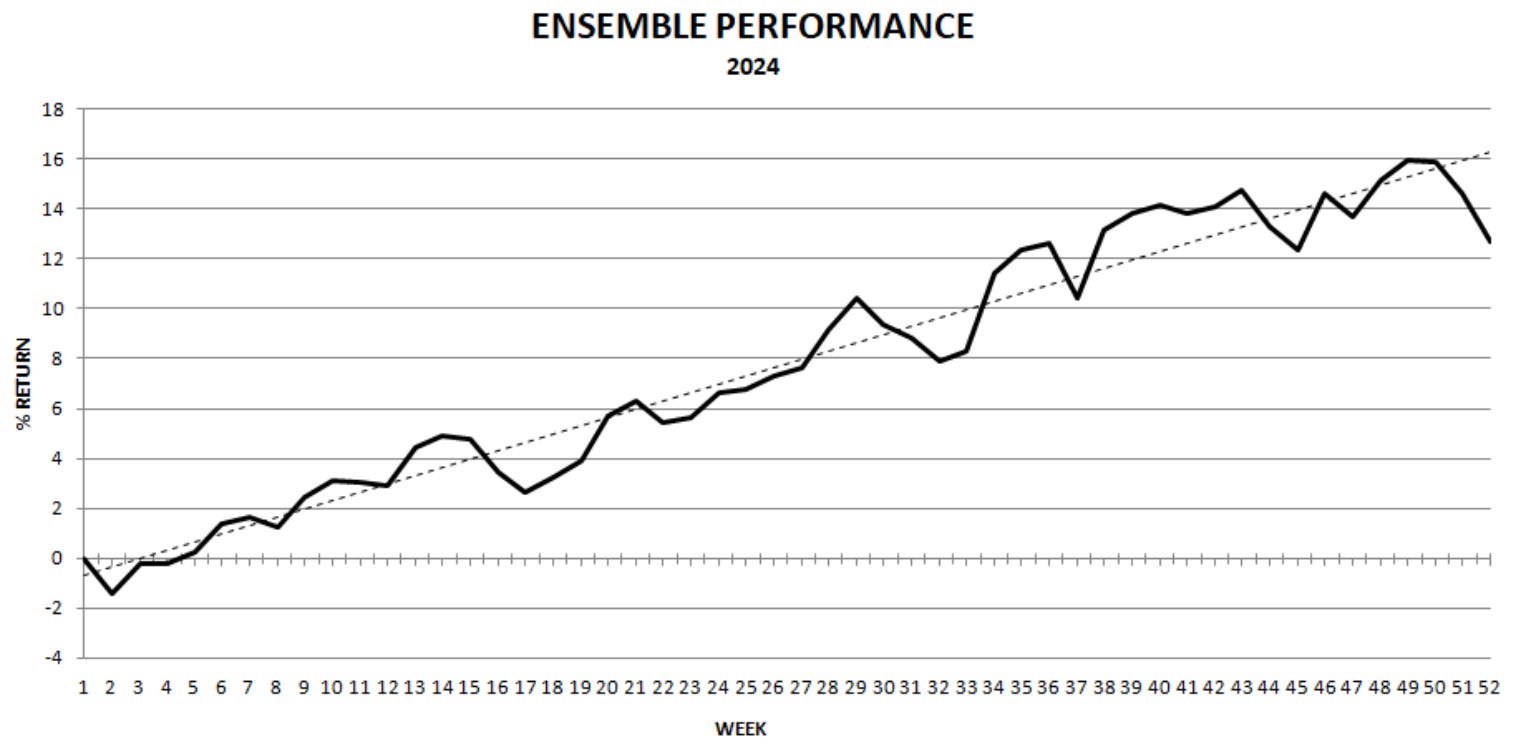

Performance of the ensemble and benchmarks

Weekly return of the ensemble: -1.6%

Year-to-date performance (Backtest, no leverage)

At 2x leverage, the strategy ensemble closely matches the S&P 500 total return this year on both an absolute and risk-adjusted basis and outperforms its equal-weight counterpart by a wide margin.

Recap and Comments (December16–December 20, 2024)

This week was a repeat of last week but with rising volatility. Below is an excerpt from last week’s report, and if we change the numbers in the order appearing, 0.6% from 0.7%, 4.5% from 2.6%, and 20.6% from 26.3%, it still holds for this week:

“This was a difficult week for systematic trading due to deteriorating breadth in the stock market and rising uncertainty. It could have gotten worse, but Dow-30 long-short provided a small convexity this week with a gain of 0.7%. Despite suffering a 2.6% weekly loss, Dow-30 mean-reversion remains the top-performing strategy with a 26.3% return year-to-date.”

This indicates that while the overall trends remain similar, the fluctuations in the data have intensified. Such changes suggest a growing uncertainty in the market dynamics compared to the previous week.”

The ensemble performance remains within our performance expectations before leverage. With 2x leverage, the performance matches that of the S&P 500 total return and exceeds that of its equal-weight counterpart by a wide margin. Last week, we wrote:

“We hope the strategy ensemble will generate reasonable risk-adjusted returns and help us navigate changing market regimes, no matter what their drivers are.”

This week, the annualised 21-day volatility of the S&P 500 index jumped from 7.9% at the end of the previous week to 12.7%. The VIX index surged to 28.3% midweek and closed at 18.4%. Stocks, bonds, and commodities fell. All assets fell with the exception of the US dollar. All in all, it appears as a group of market participants booked profits while another group that has missed the equity market rally interpreted the correction as a buying opportunity. Time will tell which group was right or wrong. Investors and long traders were looking for an excuse to sell, and the debt ceiling debacle offered that.

All in all, the probability of increased market turbulence for next year is rising. We believe that the main losers of higher volatility will be discretionary technical and macro traders. Systematic traders face frequent setbacks, but over time they have a higher probability of capturing a positive expectation, especially when they use a robust ensemble of strategies.

For positions, strategy performance, and signal summary for next week, click on the button below.