We had the October U.S. inflation report yesterday morning.

How big of a deal is that?

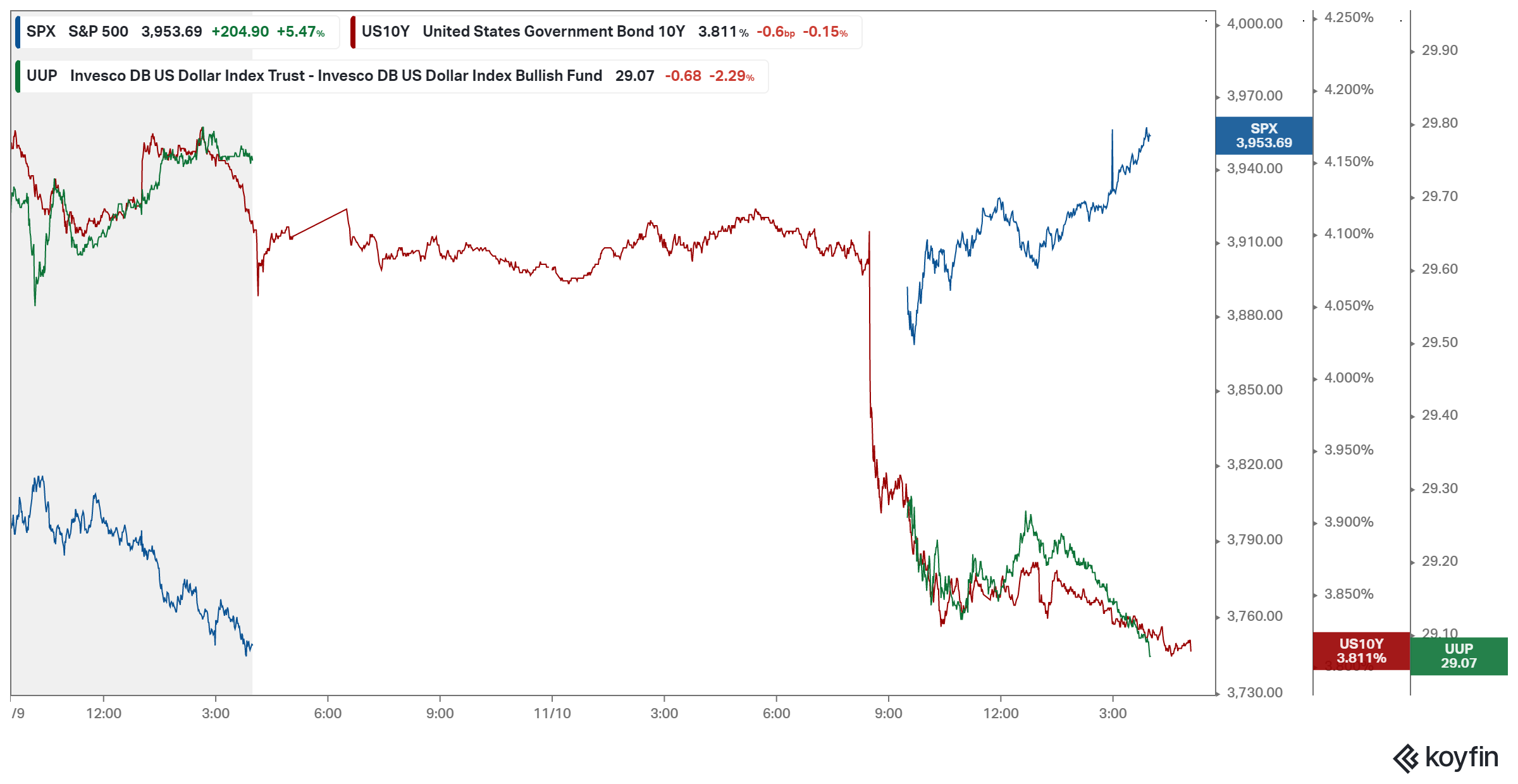

The past two reports triggered moves in stocks, of a magnitude that has historically only been associated with very significant moments. We looked at this chart last month, following the September inflation data.

These outsized ranges are associated with major market crises, policymaker intervention, policy change (via elections/votes) and market liquidity crises.

The two on the far right, however, came as the result of an inflation report. And yesterday will add another data point to this history.

The October inflation report came in cooler than expected;

Stocks (S&P futures) finished the day up 5.4%.

Ten-year Treasury yields collapsed.

The dollar was down big.

This looks like a regime change for markets.

While the government's (lagging) inflation report wasn't spectacularly different from the prior few months, we know from real-time inputs (like new and used cars, rents) that prices have been rolling over for months. Add to this, we are now past the midterms with a very high likelihood that we get at least a split Congress, which should quash any new government spending (less inflationary pressure).

As we've discussed, the 4%+ area of the benchmark U.S. 10-year Treasury yield (which has been the result of the Fed's rate hiking campaign and tough talk about the path of rates) has proven to the level that exposes vulnerabilities in the global financial system. In each stint above 4%, over the past six weeks, we've seen fireworks:

the blow up of UK government bonds,

an intervention to defend a downward spiraling yen,

and now the blow up of a major crypto exchange.

With that in mind, this chart below suggests we may have seen the last of that 4% level, at least for a while ...

PS: I would like to invite you to join the Gryning Portfolio - agnostic views coupled with a systematic approach to investing, to create actionable, market beating insights.