Market Participants VS Fed

Macro Perspectives: Fri 5 Mar 2021

We talked about the 10-year yield yesterday, as the spot to watch for market stability. On cue, whilst yields have been doing this...

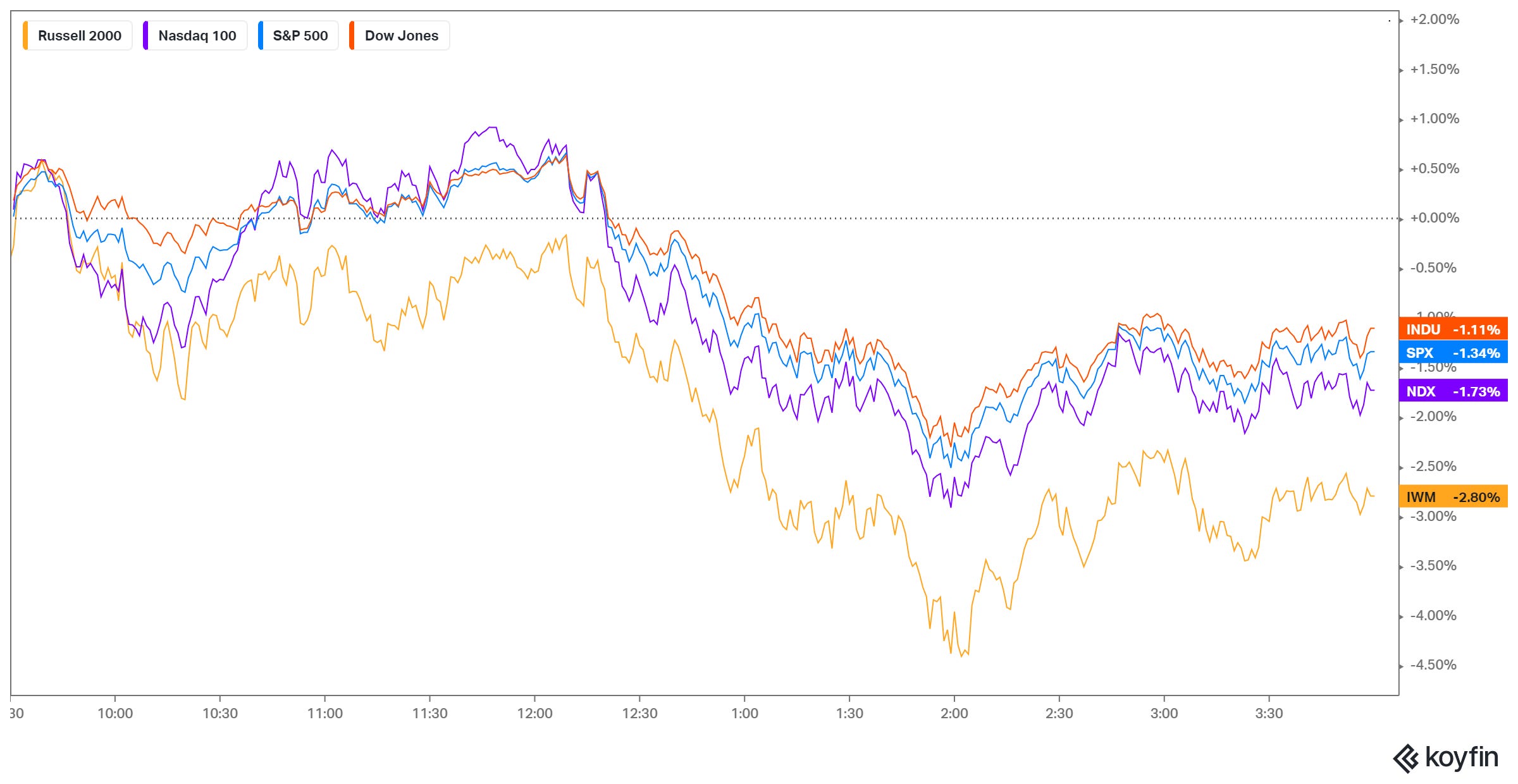

And stocks did this...

As we discussed, the sharp rise in yields, since the beginning of the year, may be a signal that the Fed has it very wrong on the inflation outlook.

On that note, the Fed Chair, Jay Powell, had a perfect opportunity to atone for any mis-positioning on the inflation outlook, in a scheduled interview with the Wall Street Journal. He declined that opportunity and stumbled through excuses - the markets didn't like it.

Following on from my note a couple of weeks ago, we should all know that Powell's intent is to signal to markets that rates will stay ultra-low and QE will continue as far as the eye can see. This is meant to set the expectations (for markets, consumers and businesses), that the Fed will be providing maximum support for years. The intent is to keep any possible impediments to the economic recovery (like behavioral changes from fears of rising prices) out of the picture, to best secure the recovery.

Market participants are smart enough to see through it and I suspect they will continue to push the interest rate market in the direction of reality (up, and stocks lower), up to the point that the Fed will have to respond (probably very soon).

History shows us that the Fed will easily regain control of the bond market (to keep rates low, to continue unbridled fuel for the recovery). However, subverting market interest rates, at this stage in the recovery, will only create far bigger challenges when they are forced to deal with rapid inflation.