Leading on the way Down.

Macro Perspectives

As we discussed yesterday, nothing has had more influence on stocks over the past sixteen months than inflation, and the fears over a draconian Fed response to it.

We looked at the trajectory of U.S. CPI earlier this week. By June, prices will be measured against a higher base (of the year prior), and that should deliver us a year-over-year inflation number in the mid 3s (percent), if not in the high 2% area.

This trajectory of U.S. inflation aligns with the producer prices, reported from China - the rate-of-change in producer prices has crashed into deflationary territory.

This is the equivalent of "skating to where the puck is going." The price of the products we will be buying in the months ahead, will be determined (in large part) by the inputs into Chinese production.

This Chinese PPI was at 26-year highs when the Fed was telling us back in 2021 that there was no inflation. It led on the way up (for global price pressures) and it is leading on the way down.

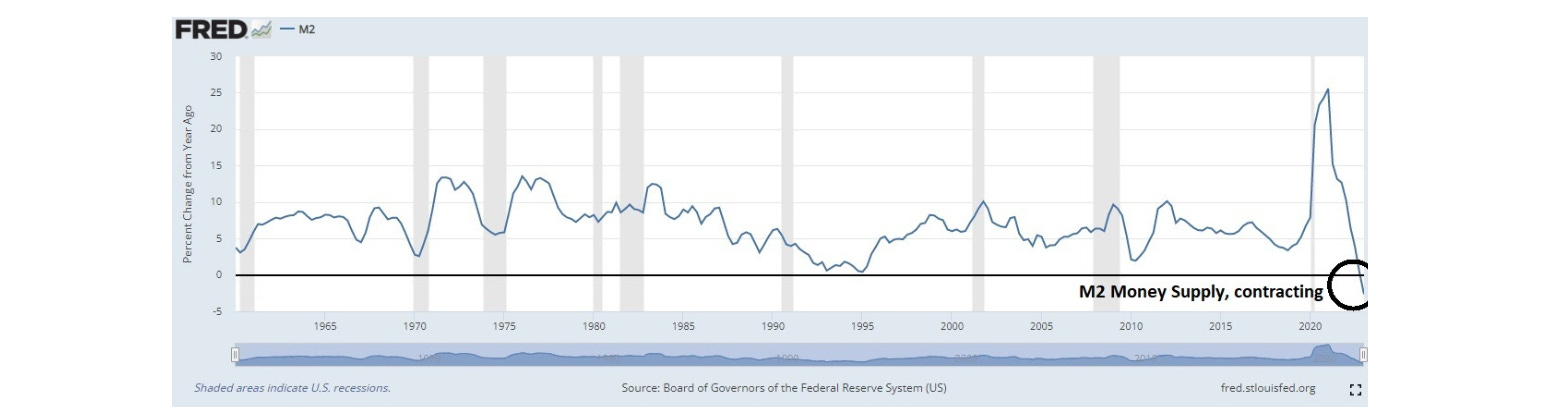

This also aligns with the record contraction in money supply.

What is typically associated with a contraction in the supply of money and credit (both are happening)? Deflation.