Jackson Hole & Quantitive Tightening?

Macro Perspectives

The market attention has turned to the gathering of global central bankers, at the end of the week, in Jackson Hole. The headline event will be a prepared speech by Jerome Powell (the Fed Chair) on Friday at 10am EST.

If we take the cues from a few well-placed, timely pieces in the Wall Street Journal, a known mouthpiece for the Fed, we should expect Powell's speech to focus on the Fed's "quantitative tightening" program.

This is the reversal of "quantitative easing," which is how the Fed injected liquidity into the economy throughout the pandemic. As we've discussed in my daily notes, this exercise of ending QE, much less reversing it (and extracting liquidity), has a bad track record - both globally and domestically, the "quantitative tightening" experiments have resulted with more QE - by necessity (i.e. by emergency).

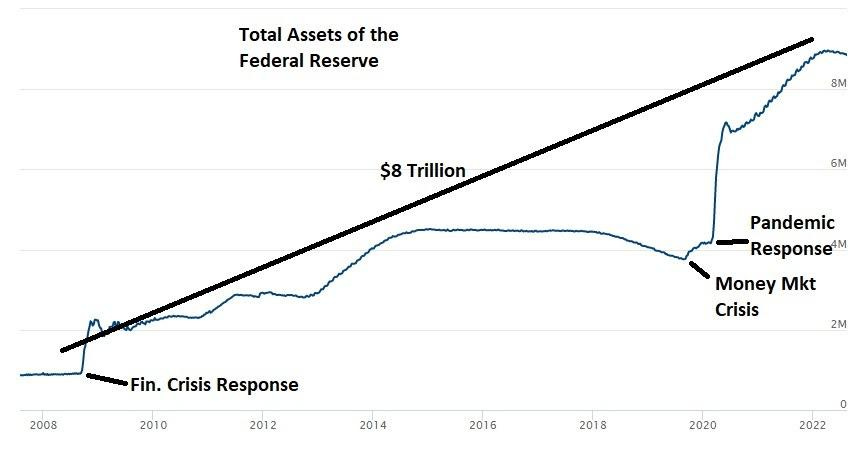

For perspective, let's take a look at what the Fed is trying to reverse here. Below is the chart of the assets on the Fed's balance sheet - since the Fed started outright buying assets, in response to the Global Financial Crisis, they've since pumped $8 trillion into the economy.

The intent was to promote stability and confidence in the economy - pinning interest rates at low levels, to promote economic activity (spending and risk taking). It has worked to avert economic disasters, but it has become a life support for what has been a sluggish economy through most of the past fourteen years.

Again, the record of successful exits of QE isn't a good one. The best guide to how this proceeds is in Japan. The Bank of Japan has been engaging in the quantitative easing experiment for the better part of 20 years now . . . they now own half of the Japanese government bond market.

The Fed now owns a quarter of U.S. government debt.

What does it all mean? It means the major economies of the world (this includes Europe) are in a vicious cycle of printing their own money, to finance their own debt.

On that note, Jerome Powell and company have talked a big game about aggressively raising interest rates, but they haven't. And they've talked a big game on shrinking their balance sheet (reversing QE), but they haven't. Friday will likely just be more talk (on the latter).

But as we discussed in my last note, the real topic of conversation at the meetings in Jackson Hole, with other global central bankers, will likely be about the solution to end this vicious cycle (a cycle that leads to ultimate insolvency). The solution seems to be moving toward a coordinated move to central bank-backed digital currencies (and likely some sort of global debt restructuring). We will see if any disclosures are made, on that front, in this week's meetings.

A message from the Sponsor

Today marks my 38th trip around the sun.

I started The Gryning Times with the objective to empower individuals' financial decisions through the democratization of investment research via concise, actionable content - looking to provide value to the retail community and to all parties that have investment performance responsibility or those that manage financial risk.

In an attempt to bridge the gap between Institutional and Retail, I have an offer for you;

As readers of The Gryning Times, when you sign up to The Gryning | Portfolio with a yearly subscription, I’ll disclose (for free) the allocations & weighting’s for the two flagship portfolios; Anti-Constrained and Uncorrelated Convexity. Subscribe below and lock in the allocations.

The offer is valid for the first 38 subscribers.