It's A Not A Sputtering Economy.

Macro Perspectives

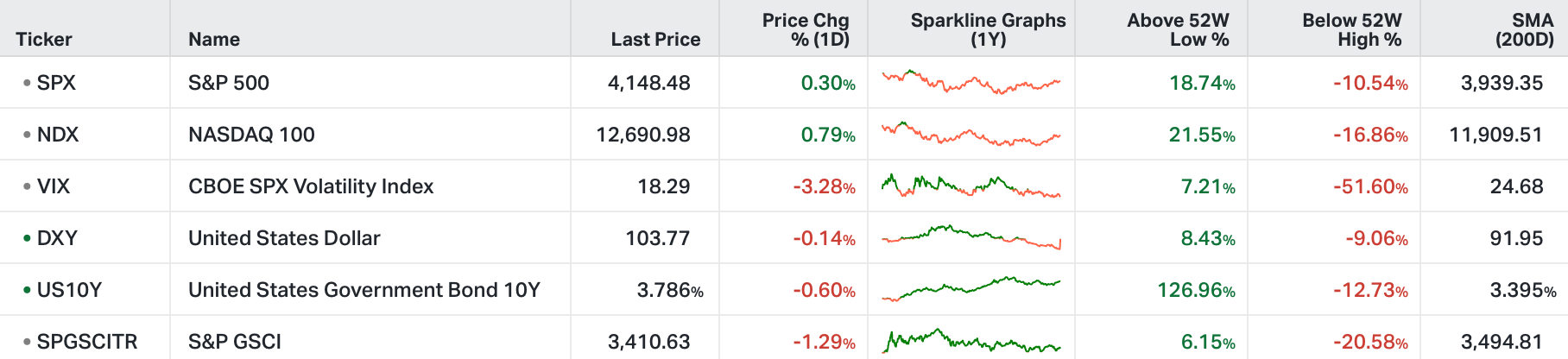

Reminder: going back to 1950, there has never been a 12-month period, following a midterm election, in which stocks were down. The average one-year return following the eighteen midterm elections of the past seventy years was 15% (about double the long-term average return of the S&P 500).

That said, we came into the year with a lot of negative expectations priced into markets;

the rate path,

earnings erosion,

recession.

On the rate path, Jay Powell has since signaled in recent weeks that the end is near, if not here. On earnings, we're about three-quarters of the way through fourth quarter earnings, and 69% of companies have beat estimates (not far from the 10-year average), and the contraction in S&P 500 earnings overall is in-line with expectations. As for recession, the consensus view coming into the year questioned not "if," but "how severe" it will be. So far, no signs of the economy faltering (quite the opposite).

And keep in mind, we've already had a technical recession (in Q1 and Q2 of last year), in reaction to high inflation, and in anticipation of higher interest rates. We've since had a 3.2% annualized growth quarter in Q3, a 2.9% quarter in Q4, and thus far, the Atlanta Fed model is projecting 2.4% for Q1 of this year.

And as we discussed in my January 27th note (here) we are in a hot economy, where demand has been throttled by the Fed. It's a not a sputtering economy with a demand problem. Yesterday's retail sales number supports that: up 3% on the month.

Excluding the covid period, that is the hottest month in over 20 years.

As I've said, the Fed is holding the beach ball under water. As they back off, we need the economy to boom, and for the wage level-to-price level gap to start closing (to restore standard of living).

The GRYNING Portfolio is expanding its offering to 6 portfolio’s, with 2 new additions - Option geared Equity (postcard shown below) and a Crypto Portfolio.