Is the Fed Overly Tight?

Macro Perspectives

5 Points

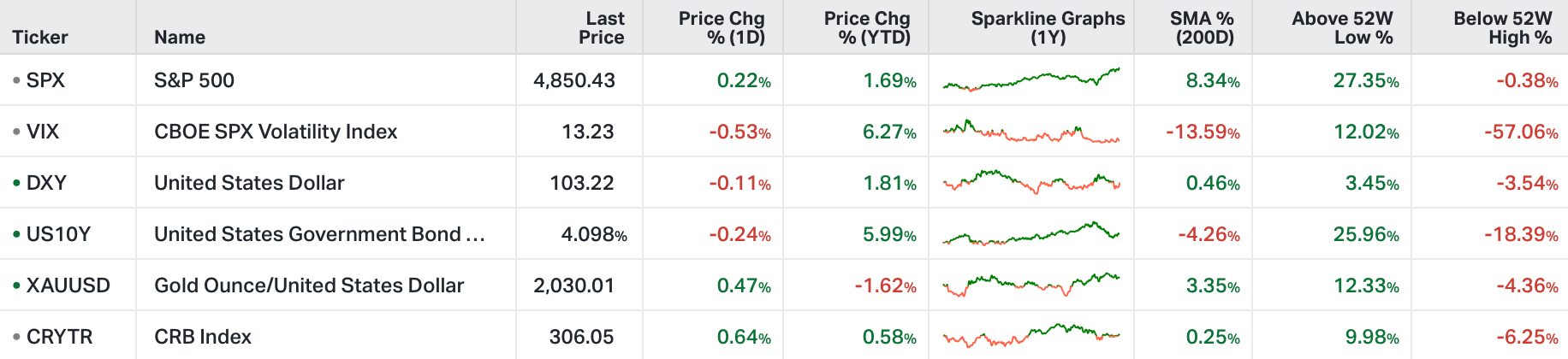

Wall Street's major averages closed at record highs on Monday as the S&P 500 added 0.2%, hitting a fresh record high after its Friday all-time high close.

Similarly, the Dow Jones and Nasdaq 100 reached records high, gaining 0.4% and 0.1%, respectively.

Macy’s rose 3.5% after rejecting a $5.8 billion proposal to take the retailer private.

SolarEdge jumped by 3.9% following the company's announcement of a 16% workforce reduction.

This week, the earnings season continues with J&J, Netflix, Verizon, 3M, Tesla, IBM, Intel.

Macro Perspectives

Stocks are on record highs, as we head into this week's inflation report - December core PCE on Friday.

This is the Fed's favored inflation gauge, however, the Fed already set the expectations on this report.

In the December Summary of Economic Projections, they saw core PCE ending the year at 3.2% (year-over-year). Last week Fed Governor, Chris Waller, got even more granular, giving an expectation for December monthly change - based on the recent CPI and PPI data, he expected core PCE to come in at a 0.2% monthly change.

He went on to say that the December report would show inflation around the Fed's target of 2% (based on the recent three and six month averages). Let's take a look ...

If Waller's right on the monthly change in core PCE, then the 12-month change will come in lower than the Fed projected last month. It will leave the 6-month average annual change in core PCE at 1.9%, and the 3-month change at just 1.6%.

This should be concerning territory for the Fed (deflationary risk). If the Fed isn't going to act sooner (than they've projected), then they may have to do bigger cuts in the coming months (50 bps, maybe 75 bps).

Remember, as we've discussed often, as the trend of falling inflation continues, it makes current Fed policy more and more restrictive (i.e. current policy puts more downward pressure on the economy, and on prices). And it's self-reinforcing.

With that, we'll get the first look at Q4 GDP on Thursday, which is expected to come in around 2.5% - that's a good number, relative to the slow growth era following the global financial crisis. It's also a good number relative to the recession calls we've heard for the better part of the past year.

But is it a good number, considering the economy had a decade's worth of money supply growth over a span of just two years?

We looked at the chart below last month - money supply remains significantly elevated. If we extrapolate out the pre-pandemic trend growth, the economy still has more than $3 trillion in excess money sloshing around. The question is;

Where would economic growth be, if the Fed weren't overly tight by nearly 300 basis points (relative to where they have told us they see the long-run Fed Funds rate when inflation is at their target of 2%)?

How sharply will the economy surge when the Fed removes the choke hold?