Inflation measures: Unemployment & Wages.

Macro Perspectives

Back in March, when the Fed made its first rate hike, Jerome Powell launched a verbal attack on demand.

In his press conference, he was asked what mechanisms he would use to reduce demand? He said this:

"If you look at today's labor market, what you have is 1.7-plus job openings for every unemployed person. So that's a very, very tight labor market - tight to an unhealthy level . . . We're trying to better align demand and supply, let's just say in the labor market. So, if you were just moving down the number of job openings so that they were more like one to one, you would have less upward pressure on wages [and] you would have a lot less of a labor shortage" . . . "and that, over time, should bring inflation down."

So the case the Fed has made for attacking jobs, has been to reduce the leverage that workers have in commanding higher wages. Higher wages are inflationary (but also a requirement to maintain a standard of living in a world where the level of prices has been reset higher).

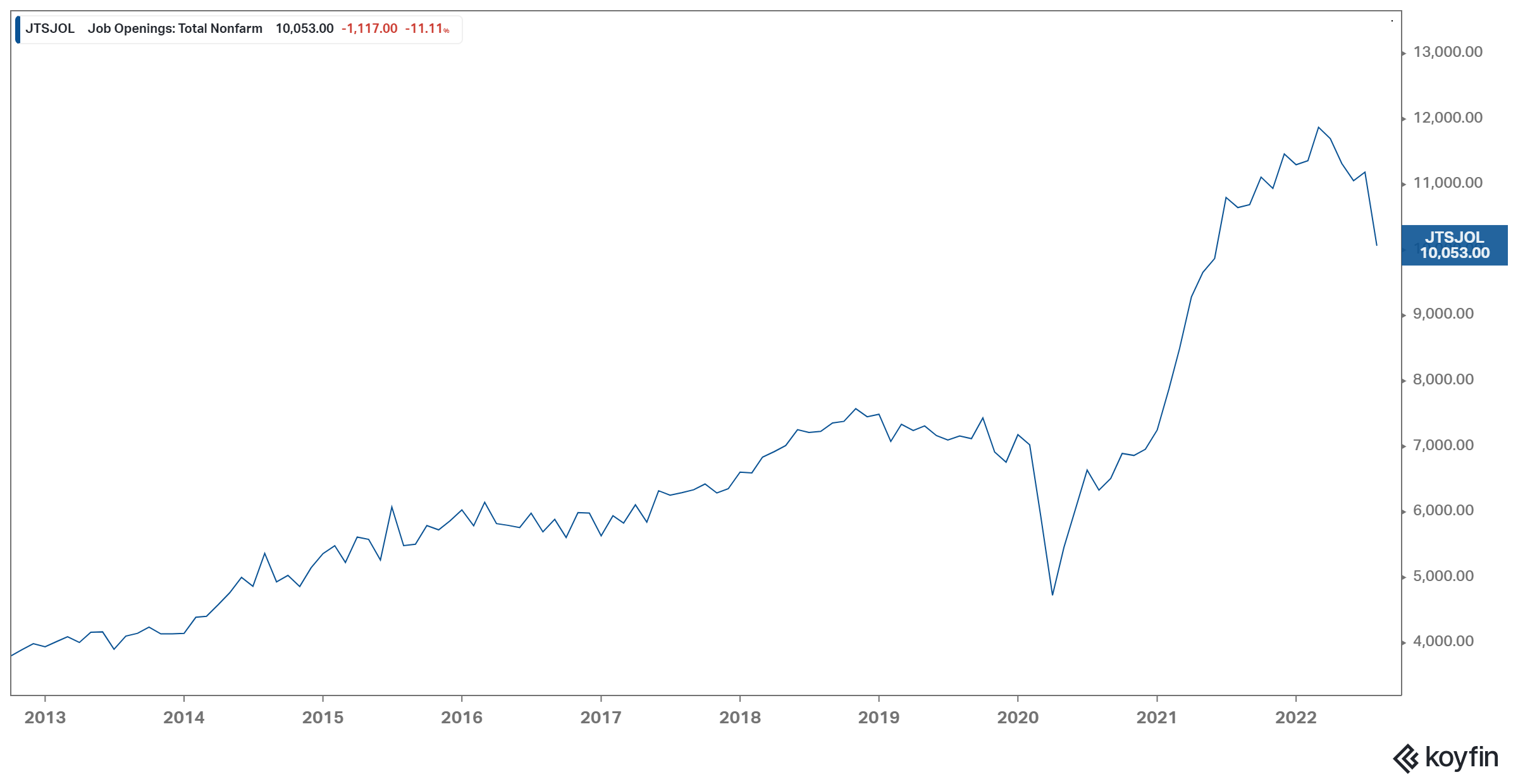

This is the chart of the jobs opening data Powell was referencing.

With about 6 million people unemployed, job openings peaked in April at nearly 12 million. That's two jobs for every unemployed worker, and the Fed has been using that data point throughout the last five months to justify tough talk about the rate path.

But as we know, the rate path already created a shock to the global financial system—enough to bring two major central banks off of the sidelines and back into the game of emergency policies (i.e., both the Bank of England and the European Central Bank: backstopping sovereign bond markets).

This destabilization in the financial system creates a conundrum for a Fed that's threatening bigger and bolder rate moves, as the job gap they've been touting as their objective has shown little signs of change.

On Monday, they were thrown a lifeline. The August report on job openings from the U.S. Bureau of Labor Statistics magically collapsed by 1.1 million jobs. Over a million jobs vanished in a month.

To put that in perspective, that was the biggest change on record (by far), only slightly behind the April 2020 collapse in job openings (when the economy was practically shut down).

That brings the job openings to worker ratio down to about 1.6 to 1.

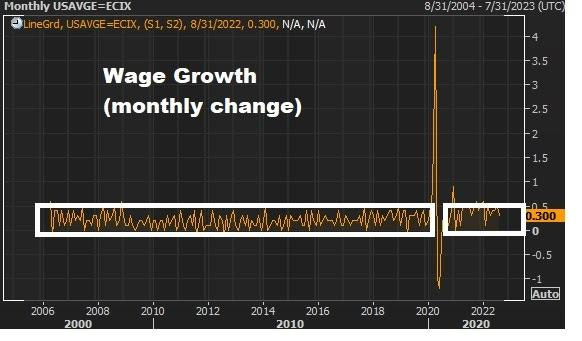

And as you can see in the next chart, wage growth is tame, within the range of pre-pandemic and running around 3.6% annualized in August (monthly change).

We get the September jobs report today (08:30 EST). The Fed needs the cover of an uptick in unemployment and soft wages.