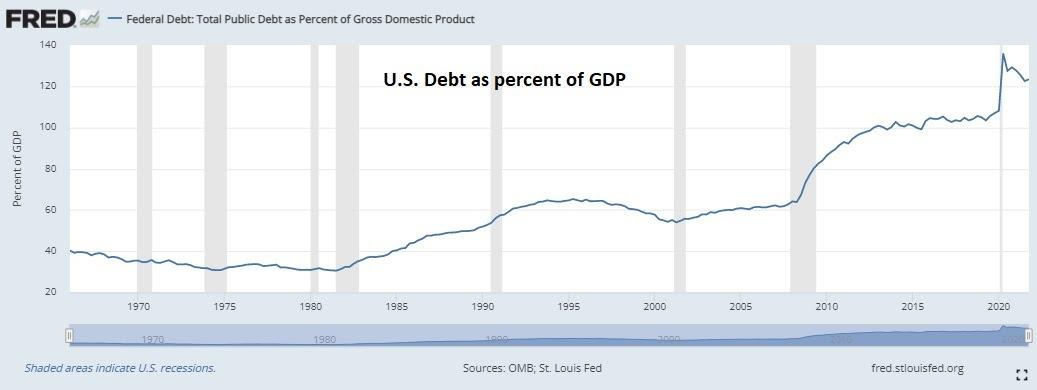

Inflating Away Debt

Macro Perspectives: Tue 05 Apr 22

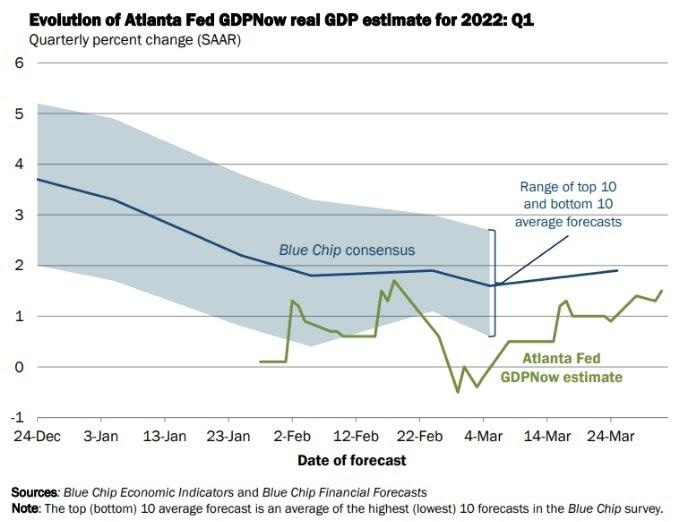

The banks will kick off earnings season next week - they will be reporting on a quarter that slowed to an annualised growth rate of somewhere between 1.5% and 2%.

Let's take a look at the trajectory of the growth projections over the past quarter.

We've heard a lot of "slowing economic growth" chatter. If we look at the chart above, we can see the consensus from the economist community (the blue line), what started as an expectation for a little better than 3.5% growth, is now coming in closer to 2%.

That looks anemic against the nearly 7% annualised growth in Q4, but that was the book-end of the fastest growth since 1984.

For more perspective, if the Q1 growth comes in around where the Atlanta Fed and economists are projecting, it would be about in line with the trend levels of the decade that preceded the pandemic.

That said, it doesn't feel like a slowing economy - this is not a weak demand economy - this is an inflation thief economy. Inflation is crushing "real" growth. Conversely, we may very well have double-digit nominal growth this year. As we've discussed, this is the "sprint on a treadmill" economy, where the economy is hot, yet it's increasingly harder to maintain a standard of living.

Reference point? If we look back to the inflation spikes of the early 70s and early 80s, nominal GDP grew by an annual rate of better than 10% during those periods.

With that magnitude of inflated growth, the U.S. economy (nominal GDP) could balloon to a $30 trillion economy within the next few years.

This is precisely what we talked about shortly after the government and the Fed fired the monetary and fiscal bazookas, to respond to the initial covid shut-down (back in March 2020). They went unimaginably big, and with the intent of inflating growth, devaluing money and inflating away debt. That initial response was probably enough to accomplish the mission. But then the new administration had an agenda to execute, and continued to fire more fiscal bullets, in the name of "crisis."

They may not be done . . . We shouldn't be surprised if we get another fiscal spend - the "Build Back Better" plan, packaged as a wartime response. With that, nominal GDP would continue to float higher.

As I said, this strategy of inflating growth and inflating away debt was always intentional/by design. You can see that starting to reflect in this chart (to the far right).