How far will Rates Run?

Macro Perspectives: Tue 26 Oct 21

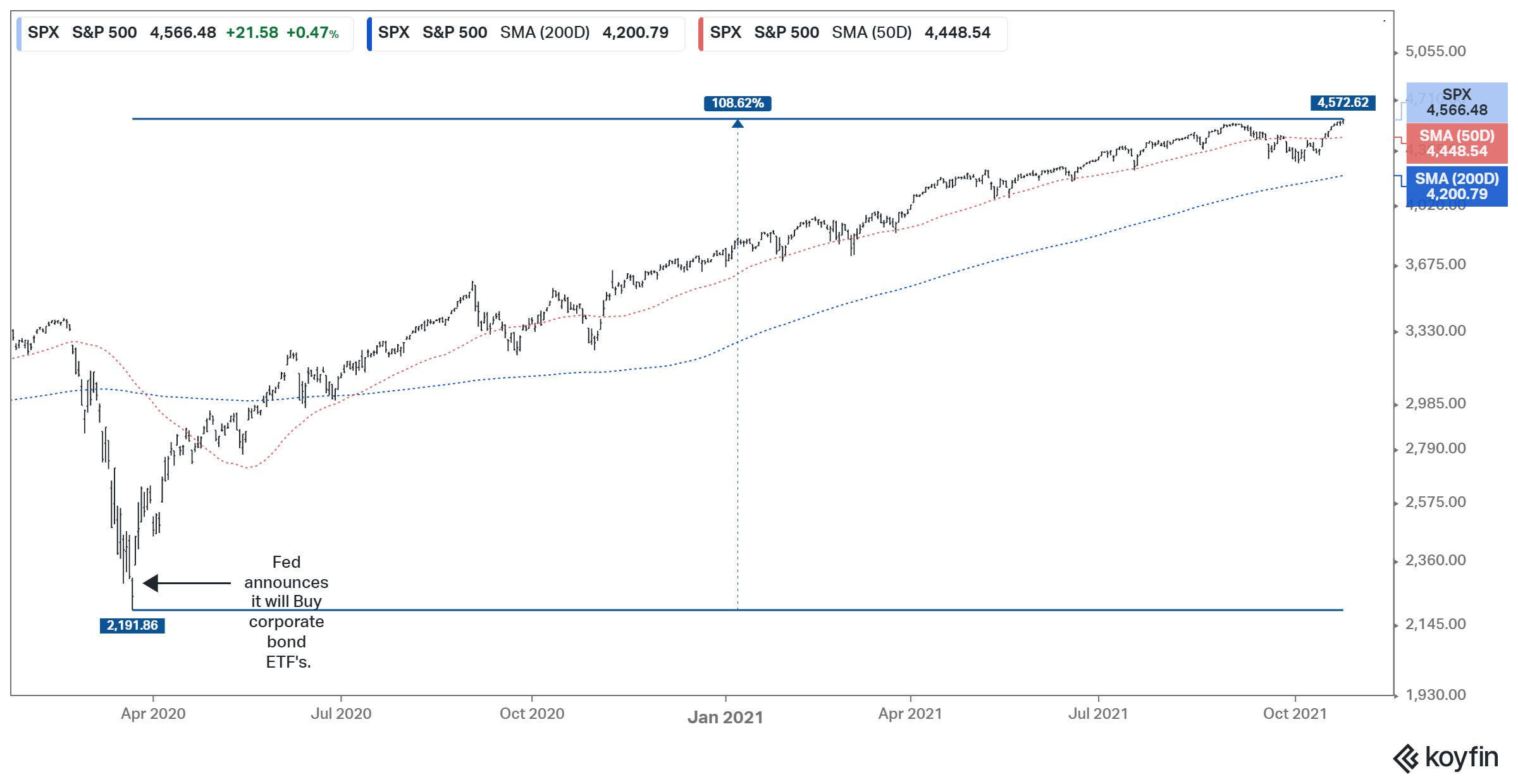

As we approach the big Fed meeting next week, let's look at a couple of charts. First, we'll take a look at stocks, which have quickly returned to new record highs.

As you can see in the chart, in addition to its QE formula of the post-financial crisis era, the Fed had to go nuclear (outright buying ETFs) to get control of the stock and bond market last year. That explicit "Fed put" has led to this doubling of the broad market in nineteen months.

With that in mind, in eight days the Fed will begin the end of emergency policies.

As we know, also contributing to this chart of stocks, was about $5 trillion dollars of fiscal stimulus. While the "Fed put" has given people the confidence to invest. The fiscal response, which protected the balance sheets of consumers and businesses, has given people the confidence to spend.

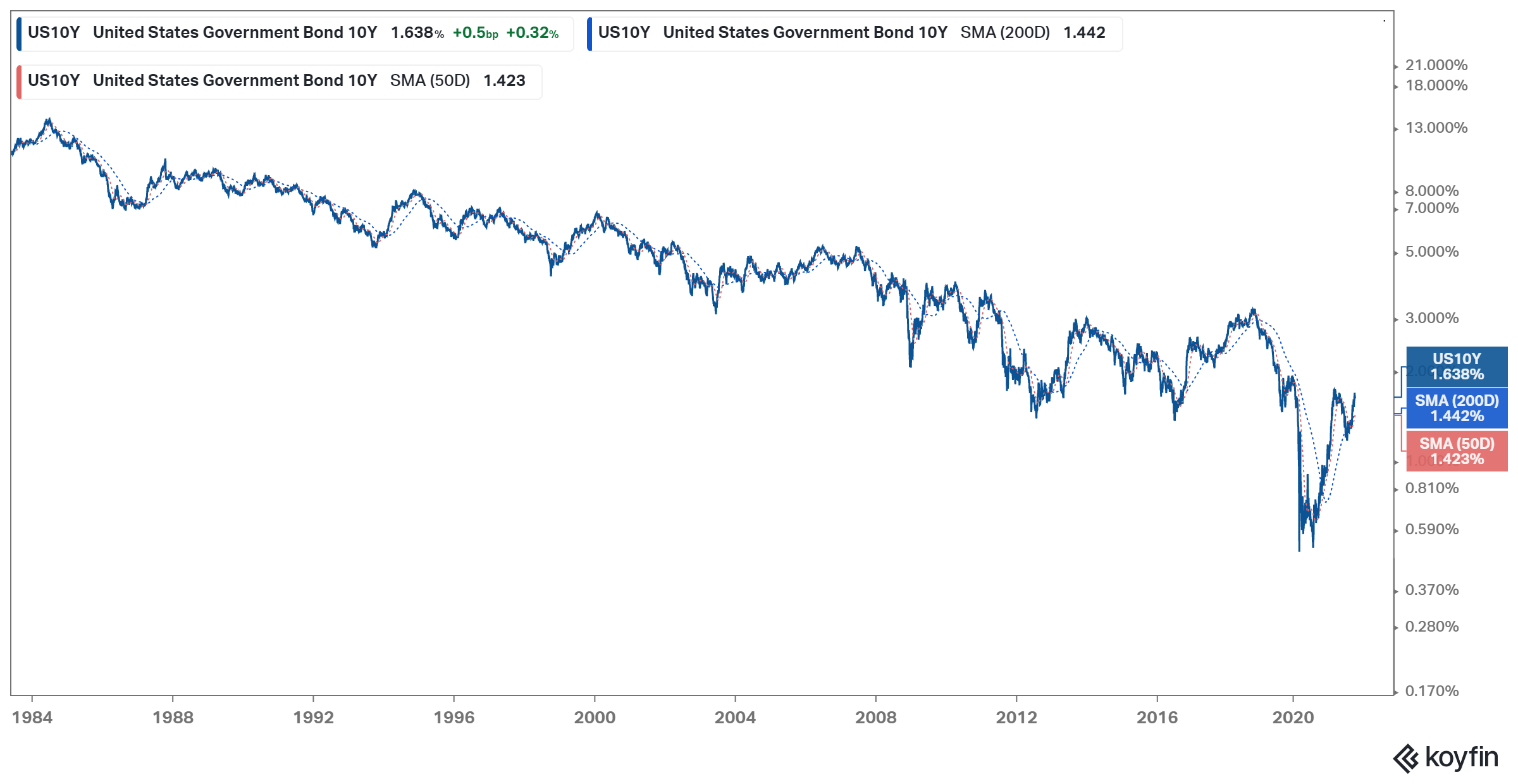

As a result, we have inflation running at levels we haven't seen in four decades. Yet the bond market is behaving as it did in the post-financial crisis environment, when we had no inflation.

We had no inflation in the post-financial crisis era because we were emerging from a debt crisis. In debt crises, you can incentivise people to borrow and spend, through monetary policy, but those people buried in debt tend to want less debt, not more - they save and they pay down debt.

In the case of the pandemic, we've had a supply and demand shock...and it's clearly resolving itself in inflation. Of course, whether or not that inflation is short-lived or a total reset of prices, depends on how much economic output was lost in the shock, relative to how much stimulus they poured into the economy to plug the gap.

We already know the answer to that. The economy contracted by $2.2 trillion in 2020, from Q1 through Q2. If we just look at the increase in money supply ($5 trillion), we can see that the response has been far greater than the damage.

So the reset of prices (too much money chasing too few goods) is clearly at work. The question is, when the Fed stops suppressing interest rates, how far will rates run (to levels of 80s era inflation?)? That will determine how heavy the headwinds will be for stocks (particularly growth stocks).