Housing to Slow, Economy to Run

Macro Perspectives: Wed 1 Sept 2021

Jim Bullard is the president of the St. Louis Fed. He is one of several Fed presidents that the Fed rolled out on a media tour last week, to confirm their hawkish pivot. Bullard will become a voting member on monetary policy beginning in January of next year, and is one of few that has warned that the Fed may very well face an inflation storm - a storm they will be forced to fight.

Additionally, he's one of few that has directly said that the current asset purchases, at this stage, are not helping the economy, but possibly fueling a housing bubble. Directly saying "the Fed doesn't need another housing bubble."

On that note, let's take a look at the housing data from yesterday morning.

Thanks to a powerful formula of tailwinds for housing (largely including Fed policy), the July report showed a 19% rise in prices over the past year.

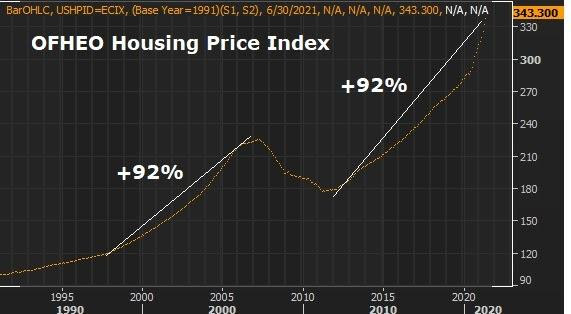

This past year is, of course, only an acceleration of the bull trend in housing of the past ten years. Here's a look at what the trajectory of this housing price run looks like compared to the housing bubble of the early 2000s...

As you can see, if we measure the ten-year trend, in each case, the appreciation in house prices is similar...up ~90%. The Case-Shiller Home Price Index paints a similar picture…up ~100%.

With that, it just so happens that the catalyst for an end of this run is here. The Fed has been buying $120 billion a month of bonds, $40 billion of which are mortgage backed securities. That has ensured that the flow of credit into housing would be easy and plentiful. As such, housing prices have boomed.

But with the Fed now positioned to begin the end of bond purchases, expect their first move to be curtailing the mortgage bonds (cutoff the housing fuel) - that should put the brakes on the aggressively rising housing market. Of note, unlike the 2000s bubble burst, the economy still has room to run, employment has room to boom, and we don't have the cliff of mortgage rate resets that triggered the defaults in housing back in 2007.