Housing Market in Moderation

Macro Perspectives

We've talked over the past few weeks about the demand headwind that has come from:

the negative net worth effect from the decline in stocks

the tax effect from the rise in gas prices.

We've also talked about the other piece of the net worth effect: housing.

To this point, housing has had a positive net worth effect and prices remain at record levels. Will it sustain through the demand headwinds and the record spike in mortgage rates?

Let's take a closer look … The Case Shiller housing price data for March was released yesterday morning - this is now two months old, but the reports showed new record highs for house prices...

That said, we've already seen evidence that this bull cycle for housing may be over - existing home sales topped in January, housing inventory bottomed in February.

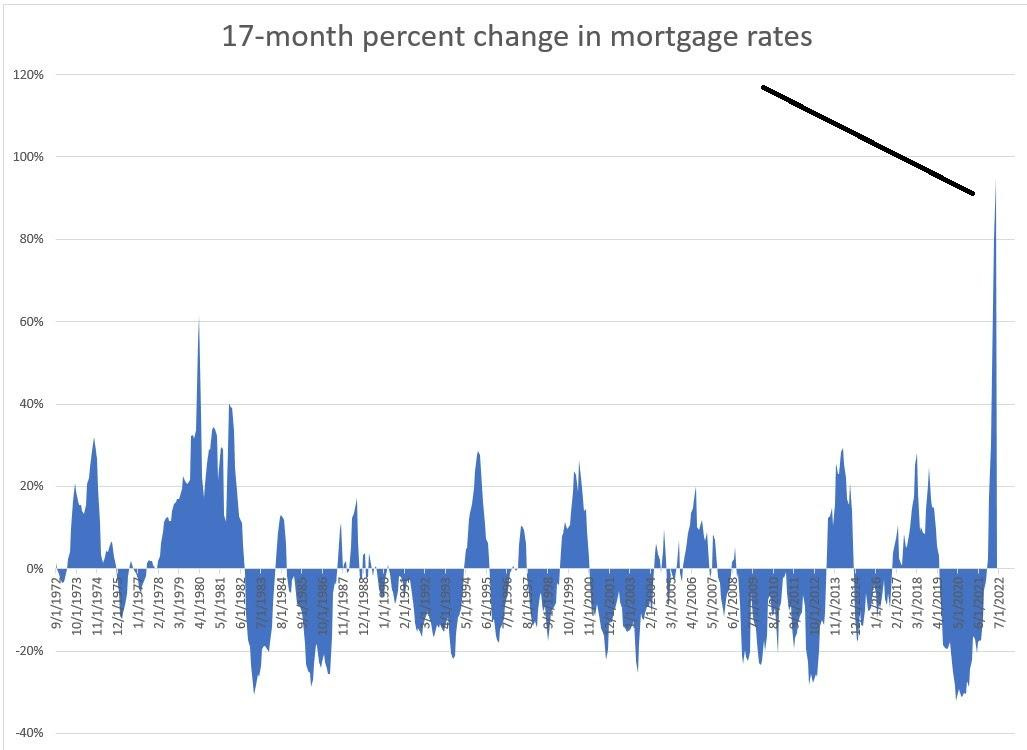

And while the Fed has moved only 75 basis points in this tightening cycle, and the effective Fed Funds rate has yet to rise above 1%, mortgage rates have exploded higher - In just 17 months, the 30-year fixed mortgage rate has spiked from 2.68% to over 5.25%.

That's a near doubling in mortgage rates - it's the fastest change on record.

One might argue that this spike in rates is coming from a record low base. That's true. But this has translated into a spike in the cost of ownership as a percent of income, to levels of 2006 and 2007 (near 40% of median income, to cover housing).

So, is the housing market set up for another bust? Unlikely.

More than half of mortgage holders have a fixed rate of 3.5% or less and only 10% of mortgages have adjusted rate mortgages - and those ARMs have a fixed rate component, on average, for between 7 to 10 years. So this isn't the fragile mortgage market of the 2008 housing crash, where 40% of all mortgages were ARMs.

What the housing market IS set up for, is a moderation, and that's another headwind for demand.

For the late cycle home buyers, the spike in the cost of ownership is destructive to discretionary spending (another tax effect). And a moderation in prices and turnover activity should be enough to knock down the animal spirits of existing home owners with significant home equity (i.e. the fearless consumption we've seen that has been underpinned by the net worth effect).

Add this, to the haircut in equity valuations and record high gas prices, and (again) the markets are doing the Fed's job for them: bringing down demand.