Housing - Cut the Intervention

Macro Perspectives: Mon 20 Sep 21

US Index Performance, Week 37.

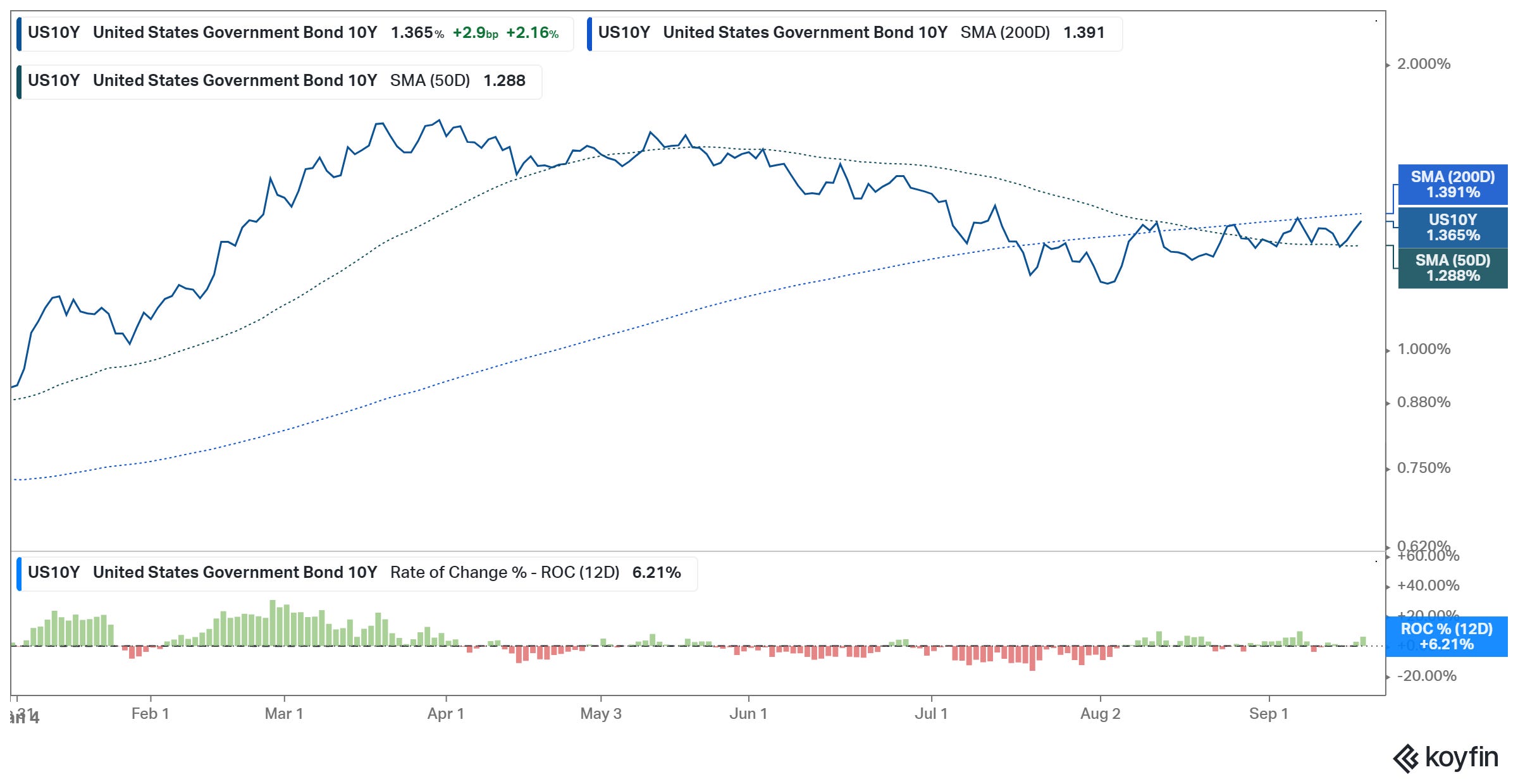

As we start Week 38 and head into the Fed meeting; stocks have closed down eight of the last nine trading days (chart above), and the 10-year yield (the benchmark interest rate market) is trading at the top of the range of the past two months.

This looks like a market showing respect for a change in the direction of monetary policy. That "change in direction" is what will happen when the Fed will/should announce plans to dial down asset purchases - the steps the Fed will likely be taking, early on, should do little to slow economic activity.

Most likely, they will just extract some of the fuel from the extremely hot housing market.

The Case Shiller Housing Price Index is up 22% from pre-pandemic levels (about 18 months ago). That's a much more aggressive pace of price appreciation than we even saw in the final stages of the early 2000s housing bubble (around 12% for an equivalent period, up to the peak in prices).

Despite this rapid rise in home prices, the Fed has continued to buy $40 billion worth of mortgage backed securities every month. In fact, if you include the front-loaded MBS purchases by the Fed during the worst period of the economic crisis (March-April 2020) and the Fed's reinvestment of MBS bonds that have matured, the Fed has bought more than a trillion dollars worth of mortgage bonds in response to the crisis.

This activity from the Fed has flooded the housing market with credit, and has pinned the 30-year fixed mortgage rate to around 3%. With a hot economy, household net worth at record highs, and an undersupplied labor market, bidding wars have dominated the housing market - clearly housing is no longer in need of Fed intervention.