Highs

US stocks closed higher in a shortened trading session on Friday, with the S&P 500 and Dow Jones adding 0.6% and 0.4%, respectively, to set new record highs, while the tech-heavy Nasdaq outperformed, rising 0.8%.

Semiconductor and equipment makers led the gains, including Nvidia (2.2%), Applied Materials (2%), and Lam Research (3.2%), following early reports that US restrictions on semiconductor equipment and AI memory chip sales to China would be less stringent than previously expected.

Retailers also saw gains thanks to Black Friday sales, with Walmart (0.7%), Target (1.7%), and Costco (1.1%) rising.

For the month of November, the S&P 500 gained 5.6%, its best month of the year; the Dow Jones surged 7.5%, its best month of the year; and the Nasdaq rose 4.9%.

These gains reflect optimism that a second Trump administration will adopt a more business-friendly approach, with growing expectations that the President-elect's Treasury secretary pick will help temper tariffs.

Hope you had a great Thanksgiving.

If you are reading this note, there is a high likelihood you have benefitted from the exceptional appreciation in the stock market this year. If the S&P 500 were to end the year this week at up about 26%, it would be the strongest performance in an election year since 1980.

The Dow Jones Industrial Average and the S&P 500 logged all-time highs this week. U.S. equity investors have much to be thankful for.

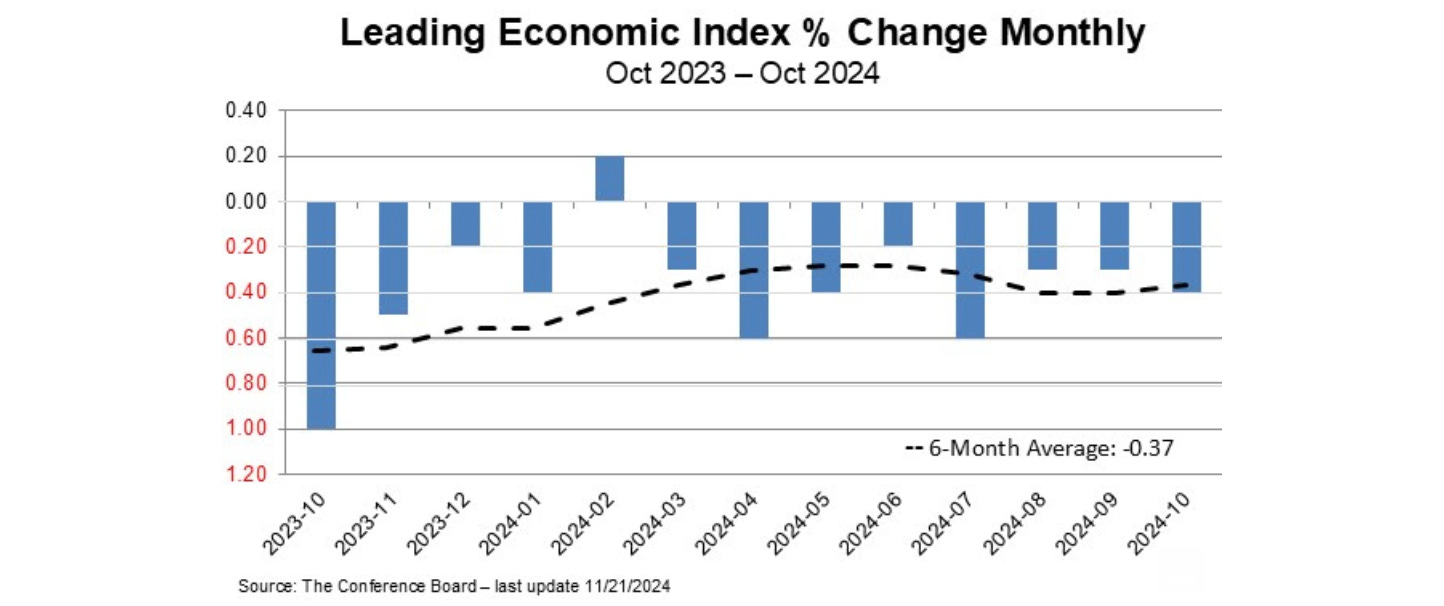

The Conference Board’s consumer Confidence Index shows consumers are becoming more confident in healthy economic growth and a solid labour market.

If consumers feel confident about their job security and/or ability to find a new job, they are likely to spend more freely on discretionary goods/and services. Last week we learnt;

real disposable personal income increased 0.4%,

weekly initial jobless claims are at low levels,

home sales jumped 2% in October.

consumers’ 12-month inflation expectations are at their lowest level since March 2020 (pre-pandemic inflation spike).

The fundamental momentum of 2024 is expected to be sustained in 2025 by real income growth, easing financial conditions, and strong productivity growth.

As we transition into 2025, a number of fiduciaries will likely recommend considering hedged ETFs, fixed income and small capitalisation stocks as ways to diversify exposure to the Magnificent 7 dominated S&P 500.