Higher Wages = Inflationary Pain = Build Back Better

Macro Perspectives: Tue 03 May 22

Tomorrow (Wednesday 04 May 2022) we will get the second move from the Fed in this early stage tightening cycle.

We go into this meeting with the last inflation reading at 8.5% (year-over-year) - if we extrapolate out the monthly change in prices from February to March (which was 0.9%), we are looking at double-digit annualised inflation.

Now, as we know, the Fed has done an about face on the inflation threat - they spent much of last year telling us that inflation was due to supply-chain disruptions (bottlenecks), and "base effects" (i.e. the inflation data was misleadingly high, as measured against depressed prices of the lockdown period). Jay Powell told us, flatly, that the Fed didn't have the tools to solve the supply chain disruption (not their job).

Never did they talk about demand. Never did they talk about the government handouts, which inflated demand: the overly generous and prolonged government subsidised unemployment checks, the PPP loans, debt moratoriums, the "child tax credit" handouts (that neither required a child, nor a taxable income...nor was it even a credit - it was a direct payment).

It was clear to see, on the ground, as consumers, that these easy money fiscal policies had distorted prices, but it wasn't politically palatable to admit it.

All along the path last year, the administration was trying to push through even more excessive spending (the most profligate of them all = "Build Back Better"). Acknowledging the demand distortions would have been a disqualifier for a new spending bill (ultimately it was, thanks to a couple of democrat hold outs in the Senate).

Suddenly, the switch flipped.

This year, the talking points from the Fed, the Treasury and the President have been about "bringing down demand."

But the economy is slowing - contracted in the first quarter. The savings rate has gone from ballooning in 2020, back to pre-pandemic levels, if not below.

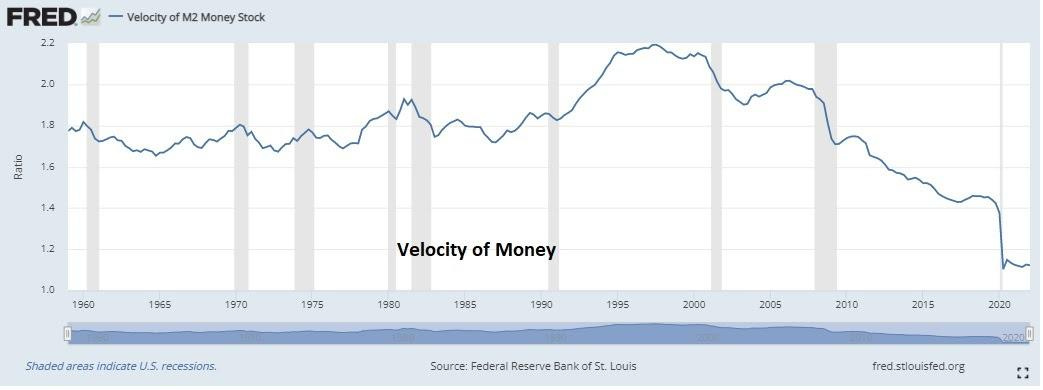

The velocity of money is at record lows - this is the rate at which money circulates through the economy. It's supposed to represent the demand for money.

What's the takeaway?

The Fed may indeed have no tools to deal with the rise in the level of prices - demand destruction is already happening.

There is nothing they can do to reverse bad energy policy-making, which has choked off investment in new oil exploration and production, and regulated away incentives to produce - which has led to a structural supply problem - guaranteeing high prices.

There’s nothing they can do to influence food supply disruptions, driven by the Russia/Ukraine conflict (which has resulted in elevated grains prices).

Short of inducing a deflationary collapse, the solution will be higher wages, to close the gap with higher prices - it has started, but there is a long way to go. It will take a while, and will be painful.

And I suspect the pain will create a political opportunity to push through "Build Back Better."