Has Operation Twist Already Begun?

Macro Perspectives: Wed 17 Mar 2021

We had some surprisingly negative economic data yesterday morning that set the tone for stocks.

For the first time since May, month-over-month industrial production contracted in February.

After nine consecutive months of improving capacity utilization (to near pre-Pandemic levels), that also declined in February.

So, the "operating rate" of the economy declined last month and the momentum in retail sales slowed in February, and with a bigger decline than expected.

This is surprising, but with checks hitting accounts from stimulus this week, and, moreover, another $1.5 trillion in stimulus being disbursed, the March economic data should bounce back aggressively.

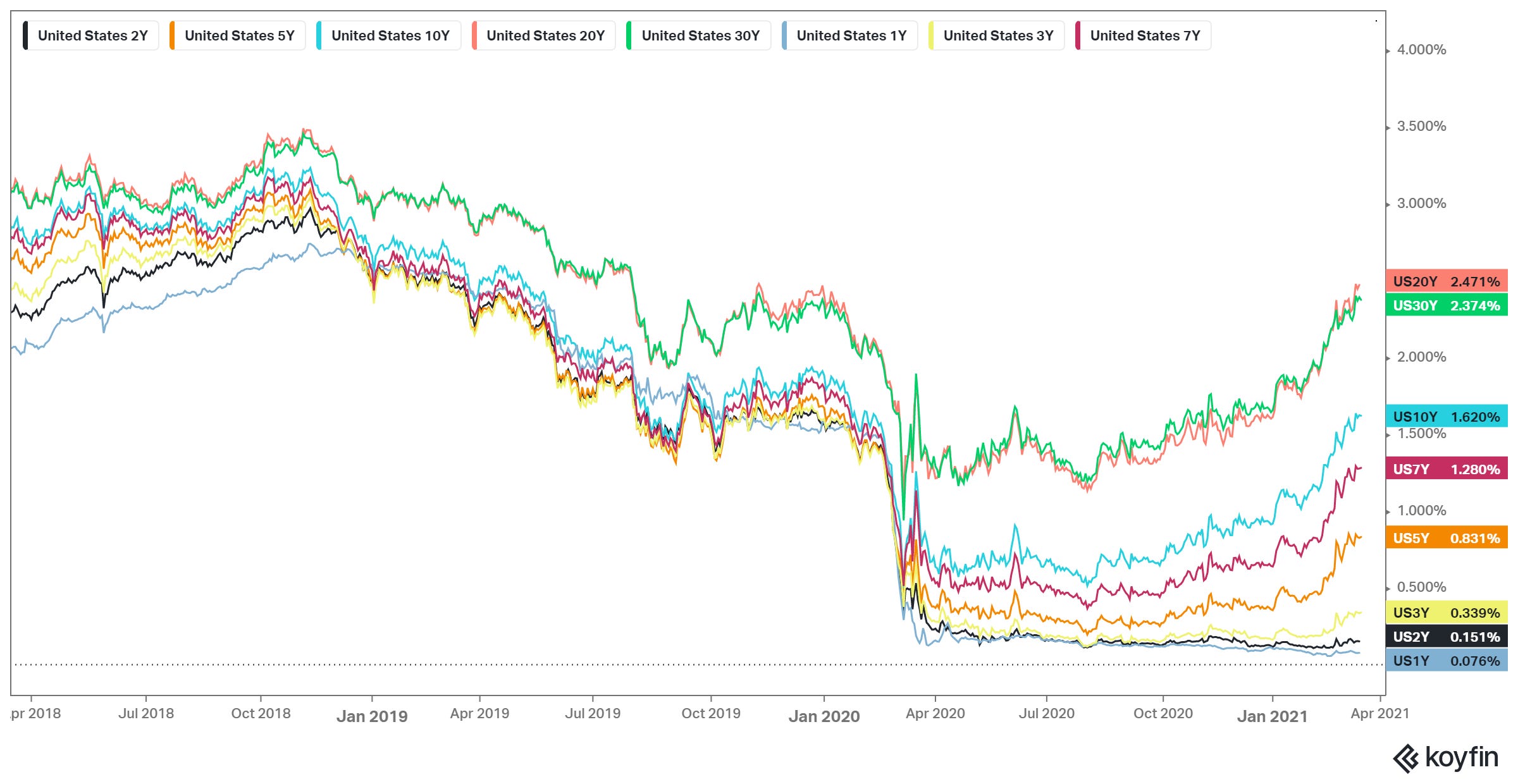

We talked about the Fed meeting in my note yesterday. They will begin a two-day meeting today, concluding with a press conference on Thursday afternoon. Markets will be sensitive to any signals from the Fed that they might be looking to take action against the rising 10-year yield (i.e. market interest rates, which affect mortgage and consumer rates).

As we discussed, there has been some chatter that the Fed might consider another round of "Operation Twist," where they would sell short term bonds, and use the proceeds to buy longer term bonds (i.e. to tamp down the 10-year yield). Former "bond king" Bill Gross said he suspects they might already be in the market, executing a program to keep longer term yields in check.

What's the impact? Ultimately, keeping rates in check will keep the economic momentum going. That means hotter growth but it also means hotter inflation to come - it's a matter of when.