We talked about the significance of the G7 finance ministers meeting last month - this is the meeting that tends to prepare the groundwork for the G7 leaders to meet.

Recap: Despite the economic conundrum of four-decade high inflation, record high debt and deficits, and record low interest rates, the economy was not the priority issue (for the most powerful finance officials in the world!). In their communique, "support for Ukraine" was top priority;

Ukraine was mentioned twenty times throughout the communique,

The word economy was mentioned only four times,

Inflation, only three times.

The word most used throughout the communique was climate - for much of the post-financial crisis era, these meetings were about globally coordinating policy to avert economic disaster. Now it's about globally coordinating to execute the transformation agenda (climate and social).

With all of the above in mind, the G7 leaders meeting is now underway and not surprisingly, supporting Ukraine is the broad theme. Bringing down inflation, and restoring quality of life for the Western world (which gets amplified in the developing world), is not the priority.

In fact, in the face of the ballooned global money supply of the past two years, and the subsequent four-decade high inflation, the Ukraine-centric focus is fueling even more profligate spending from G7 countries (none of which have the money to spend). This wartime-like spending only underpins inflation. Add to this, in the G7 leaders statement, they are doubling down on the inflationary input of high oil prices, by committing to "accelerate the transition on the dependency on fossil fuels."

What do high oil prices give us? Higher food prices. A World Bank study from 2013, analysing 52 years of data, found that "of all the drivers of food prices, crude oil prices mattered the most."

No coincidence, what was also widely discussed in Germany at these G7 leader meetings? Food crisis.

As with oil, global leaders deflect blame of food supply and prices onto Russia/Ukraine. But as we know, these are results of intentional policy making - when you promise to kill the fossil fuels industry, and then you begin to make good on those promises, by regulating away supply, choking off investment in new exploration, and (consequently) ceding control of prices to Saudi Arabia, you get much higher oil prices.

And as I said in my 4th March 22 note (click here), just a week after Russia invaded Ukraine, "a predicted-future climate crisis has led to policymaking that has created an immediate energy crisis. Next up, looks like food crisis." Updated chart shown below…

From the chart above, you can clearly see that the food prices were already nearing record highs, before any impact on Ukrainian food supply (now 16% higher).

This is a squeeze on the standard of living for rich countries. For poor countries, it's a full blown crisis.

Bottom line, the global agenda continues to drive the outcome. And it's well coordinated. This agenda will continue to fuel higher prices through supply shortages. We've seen it in oil. We're going to see it more clearly in other commodities, through the secondary effects of high oil prices, only exacerbated by the "green" regulatory burden.

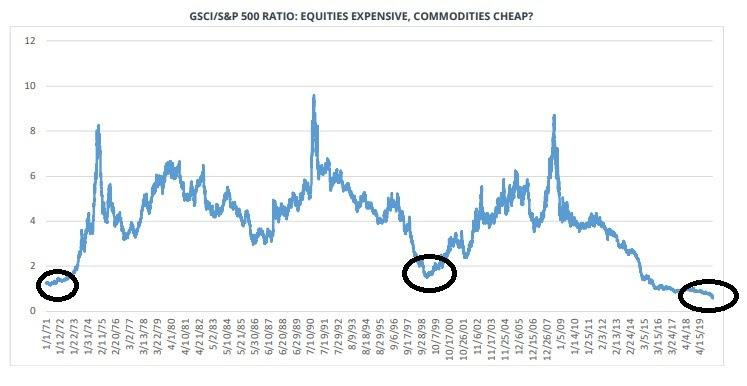

This all sets up for what history tells us should be a long-term bull cycle in commodities prices, and therefore, commodities investing. Remember, we looked at this chart at the beginning of the year - the ratio of commodities prices to stock prices.

As you can see, heading into this inflationary environment, commodities are coming out of a period of significant underperformance, relative to stocks - commodities haven't been this cheap, relative to stocks, in 50 years. You can see how sharply this valuation divergence corrected back in the early 70s period - which shared the ingredients of oil crisis and inflation.

Chart below shows 1 year S&P GSCI Commodity Index.

Bottom line: The Fed-induced slow down in the first half of the year has driven speculation that the deflationary forces of the past decade may return. But the spending required in the transformation (political) agenda, and this commodities/stock valuation cycle suggests that higher prices and higher than average growth are the new economic regime. But it comes with a lower standard of living, until the wage/price gap closes (which won't be soon).

PS: Subscribe to The Gryning Portfolio for an actionable, do-it-yourself way to beat the markets.