Four

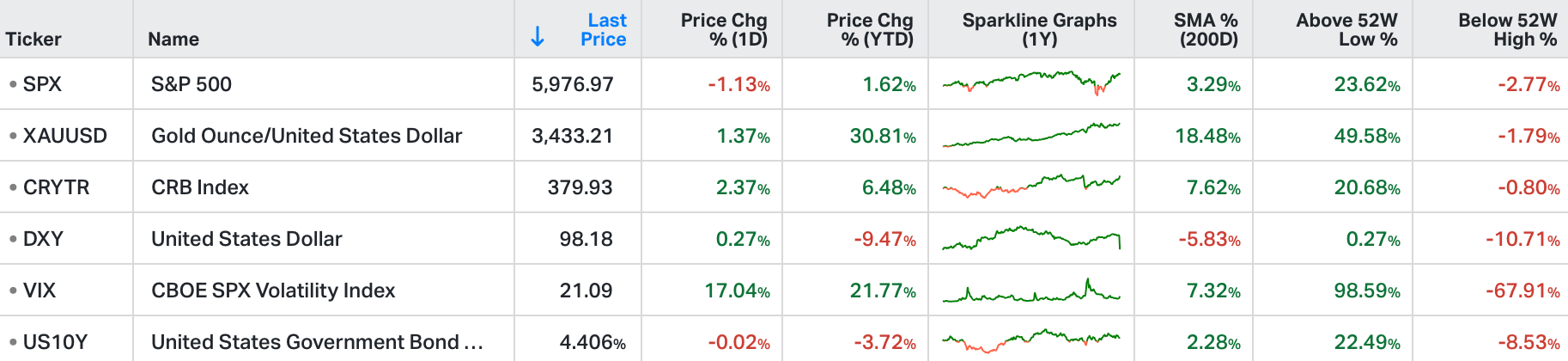

US stocks closed sharply lower on Friday as risk appetite faded after Iran denounced Israel’s airstrikes as a “declaration of war” and responded with missile attacks late Friday local time.

The strikes targeted Iran’s nuclear and military facilities, significantly escalating geopolitical tensions and unsettling global markets.

Financials and tech led the losses, with Nvidia down 2.1%, Apple off 1.4%, and Visa and Mastercard sliding over 4%.

Airline stocks also sank, with American, Delta, and United down between 4.5% and 5%.

Meanwhile, energy and defence shares outperformed as oil prices surged nearly 7% on supply concerns; Exxon rose 2%, and Lockheed Martin, RTX, and Northrop Grumman climbed more than 3%.

The S&P 500 has drifted higher in June and is less than 2% below its all-time high. What is pulling the market higher are the four horsemen: earnings, jobs, inflation and tariff talks.

Earnings: For the first quarter, earnings per share of S&P 500 companies rose 12.7% year-over-year. The Wall Street consensus analyst expectation was for a 6.5% increase. This was the seventh consecutive quarter of earnings outperformance.

Inflation: Total CPI was up 0.1% month-over-month in May versus consensus expectations of 0.2% and after increasing 0.2% in April. Core CPI, which excludes food and energy, was up 0.1% month-over-month versus consensus expectations of 0.3% and after increasing 0.2% in April. On a year-over-year basis, total CPI was up 2.4%, versus 2.3% in April. Core CPI was up 2.8% year-over-year, versus 2.8% in April.

Jobs: We learnt that the unemployment rate is 4.2% and average hourly earnings rose by 0.4%, which translated into a better-than-inflation 3.9% year-over-year growth rate. Strong employment and wage gains should keep consumers spending and the economy on a growth trajectory.

Tariffs: U.S. - China trade talks in London led to China supplying rare earth elements to the U.S. immediately and a pull back in the tariff rate from 145% to 55%. Bloomberg is reporting that a deal between the U.S. and the European Union could be forthcoming, making the July 9 deadline less important. Reuters noted that an interim deal with India might be announced by the end of June.

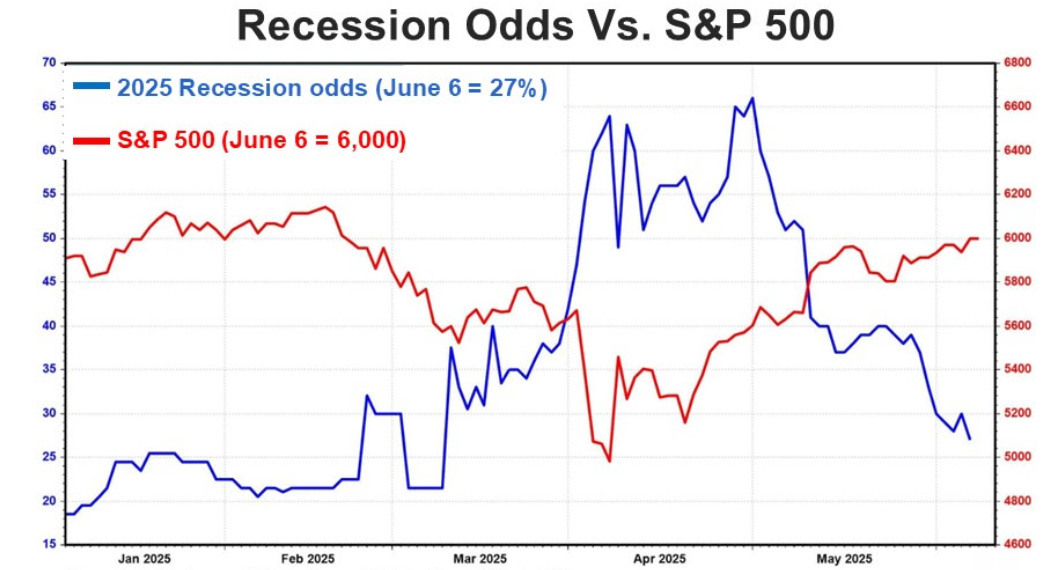

Polymarkets.com, the largest prediction/betting market on future events, shows the odds of a recession are back down to 27% from a recent peak of 66% on May 1.

The fear is economic activity has been pulled forward as consumers and businesses attempt to “get ahead” of tariff price increases and inflation is subdued as tariff price increases have yet to take full effect.

However, a geopolitical risk premium came back into the oil market following Israel’s strike on Iran. Unsurprisingly, safe haven assets rallied; the dollar has strengthened; and US/global equities are lower.

Will we see another run UP in yields, on the prospects of inflationary outcomes: an oil price shock? The chart below is from our Global Trend Model - where we aim to highlight potential market turning points.

To mark 5 years on substack, we have opened up our institutional offering to a monthly subscription, where you’ll get, at minimum;

Monthly Global Trend Report.

Weekly Commodity Chartbook.

Weekly 100 ticker of your choice Trend Model Chartbook with Future Price Scenarios.

Daily Trend Summary plus notifications on the top 3 trends to watch / trade.

Experience the future of financial risk assessment - a dynamic approach to helping traders & investors stay ahead of bubbles and crashes.