Fitch Downgrades US Credit Rating . . . and why thats Bullish!

Macro Perspectives

Fitch downgraded U.S. government debt, after the market close.

Does it matter?

Fitch is one of the three "Nationally Recognized Statistical Rating Organizations" designated by the SEC. It was Fitch, and its two counterparts (Standard & Poors and Moody's) that brought us the real estate bubble, which turned into the global financial crisis.

Yes, that real estate bubble was primarily driven by credit agencies stamping AAA ratings on high risk/high yielding mortgage securities. These unwarranted ratings were a mix of fraud, mal-incentives, and incompetence (on the part of the ratings agencies).

With a AAA rating and a high yield, massive pension funds had no choice, if not an obligation, to plow money into those investments. With that insatiable demand, mortgage brokers and bankers were incentivized to keep sourcing them and packaging them. And the bubble was blown.

With that, it's perplexing that they (the ratings agencies) are still in business, much less have credibility.

Yesterday's downgrade comes as the economy is running hotter than most expected, and is on a path for a potential economic boom, which gives the U.S. a chance to grow out of the debt burden . . .

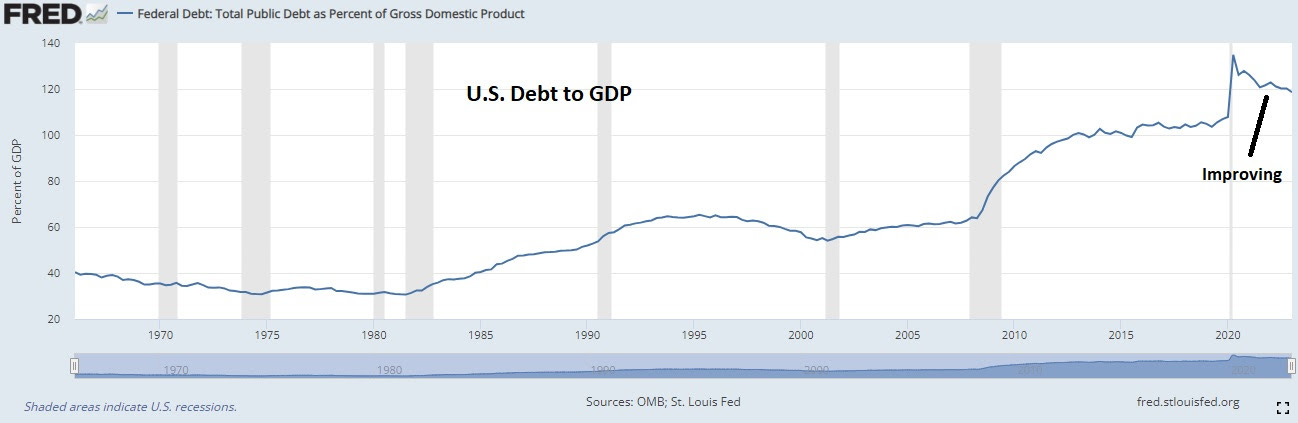

Keep in mind, the absolute value of government debt doesn't mean much. What matters is debt relative to the size of the economy, and as you can see in the chart above, that's been improving (thanks to hot nominal growth).

Nonetheless, let's take a look at what happened when Standard & Poors downgraded U.S. debt back in 2011.

That downgrade, too, came shortly after the end of a debt ceiling standoff.

One might expect a downgrade in the credit rating of U.S. Treasuries, what the world has known to be the safest, most liquid government bond market in the world, would result in capital flight.

It was just the opposite.

Money flowed into Treasuries. Prices went higher, yields went lower.

Why? Because it was still the safest, most liquid government bond market in the world.

The U.S. stock market bottomed a few days after the downgrade . . . and so did the dollar.

It turns out the downgrade in U.S. debt amplified the relative safety, value and liquidity of U.S. markets, because it amplified the greater vulnerabilities in sovereign debt outside of the U.S., namely in Europe.

Indeed, downgrades followed in Europe and the sovereign debt markets of the weak spots in Europe, particularly Italy and Spain, became targets of speculative selling, sending borrowing rates soaring to unsustainable levels. These countries were on default watch, and with default would have come a collapse of the European common currency (the euro).

The European Central Bank (Mario Draghi) finally stepped in (they crossed the line in the sand), vowing to do "whatever it takes" to save the euro, and to maintain stability and solvency in the euro zone.

The ECB was the last of the world's most powerful central banks to cross the line, to rip up the rule book and become an explicit market manipulator. They haven't looked back. With that, we should expect any impact from this downgrade, if any, to be subdued (either by central bank action, or the implicit threat of action).