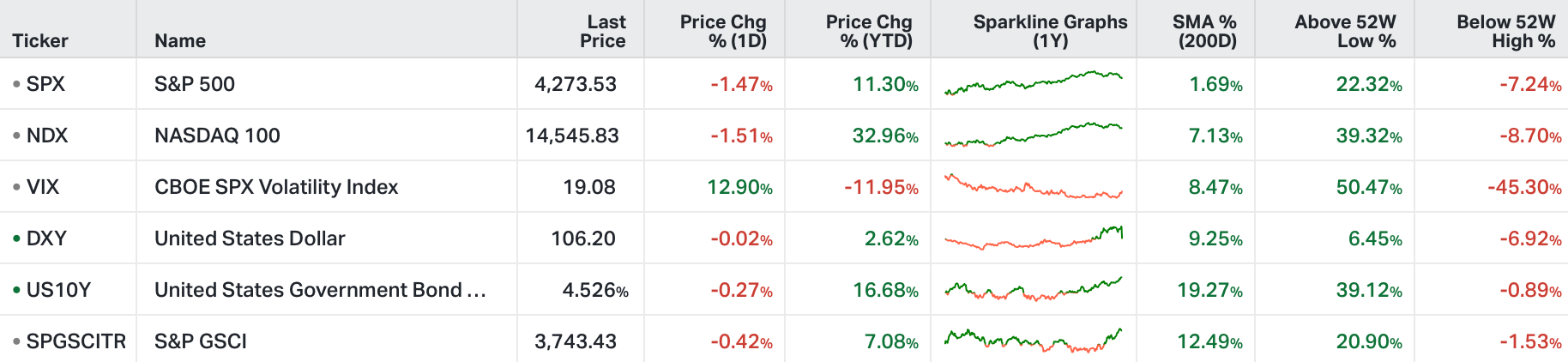

We looked at this chart on Friday . . .

The technical break-down in stocks has been driven by the pain of a sharp 25 basis point rise in the U.S. 10-year yield, in response to the Fed's meeting last week. That pain has spread to stock and bond markets in Asia and Europe, as well.

You don't have to look too hard to find bad news to compound what looks like vulnerable levels in key financial markets. But that's not unusual, especially in the recent history of the past 15-years - in the post-Global Financial Crisis world. Speaking of history, let's take a look back to late September of 2021 - two years ago. This was another rough September, which left the S&P down 5%.

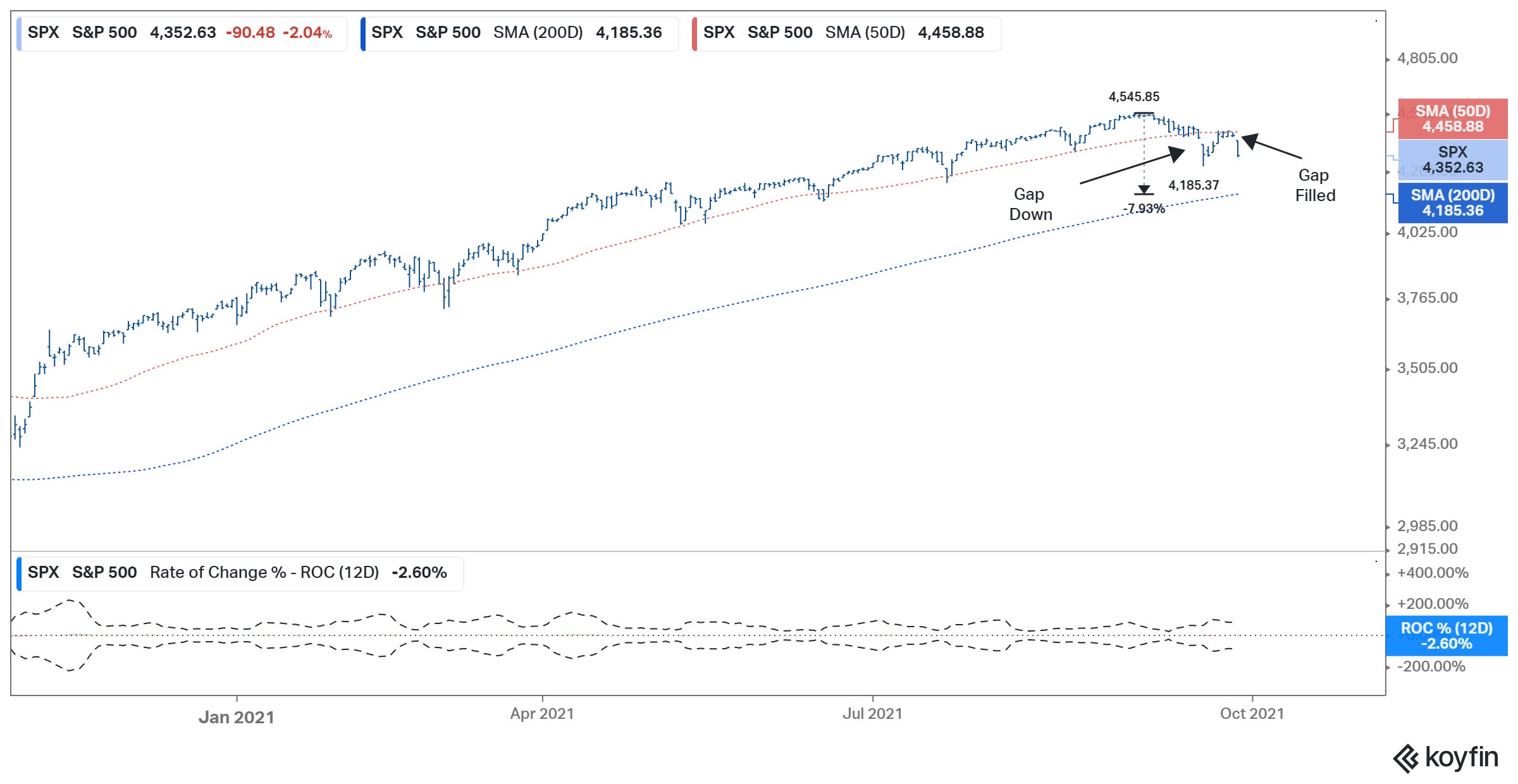

This is what stocks were doing at the time . . .

This chart is from my September 29, 2021 note (here). The "pain" catalyst was mostly driven by a move UP in interest rates (the 10-year yield). The Fed had turned hawkish, finally telegraphing a change in the direction of monetary policy, from easing to tightening, which is historically bad for stocks. Add to that, there were two other negatives weighing on stocks back in September of 2021: 1) concern about the Chinese financial system, namely a default by its biggest real estate developer, and 2) a potential U.S. government shutdown.

Sounds very familiar.

The trendline in the 2021 chart represented the 40% climb from election day, on anticipation of a massive fiscal spend. The break of that line turned out to be a minor technical correction, lasting a little less than a month - stocks rallied 12% in the fourth quarter of 2021, finishing on the highs.

Let's turn attention back to the current chart.

First, you'll notice the level of the S&P 500 is right where we were two years ago (low 4300s). So, after two years of rate hikes and (indirect and direct) demand suppression by the Fed, the global risk proxy (the S&P 500) is nearly unchanged.

The factors weighing on stocks are similar to that of September 2021 (rising rates, a threat of government shutdown, problems in the Chinese property market).

But now we have a Fed that is, at worst, one more rate hike away from telegraphing a change in policy direction (from tightening to easing). At best, they are already there.

With all of the above in mind, going back through almost 80 years of data, we have a 10% decline in stocks, on average, about once a year. We've yet to have one this year. If we test the 200-day moving average (the green line in the top chart), that comes in at 9% below the July lows - that's just 2.3% lower than yesterday's close.

This puts us on the path toward Q3 earnings in a couple of weeks, where expectations have, again, been dialed down - which sets up for positive surprises.