Fed's New Financial Conditions Index

Macro Perspectives

On Friday we heard from Jerome Powell where he delivered some prepared remarks for a Fireside Chat at Spelman College.

Keep in mind, in the last Fed meeting, Powell signaled the end of the tightening cycle, and attributed it (in part) to the tightening of financial conditions over the preceding months, resulting from:

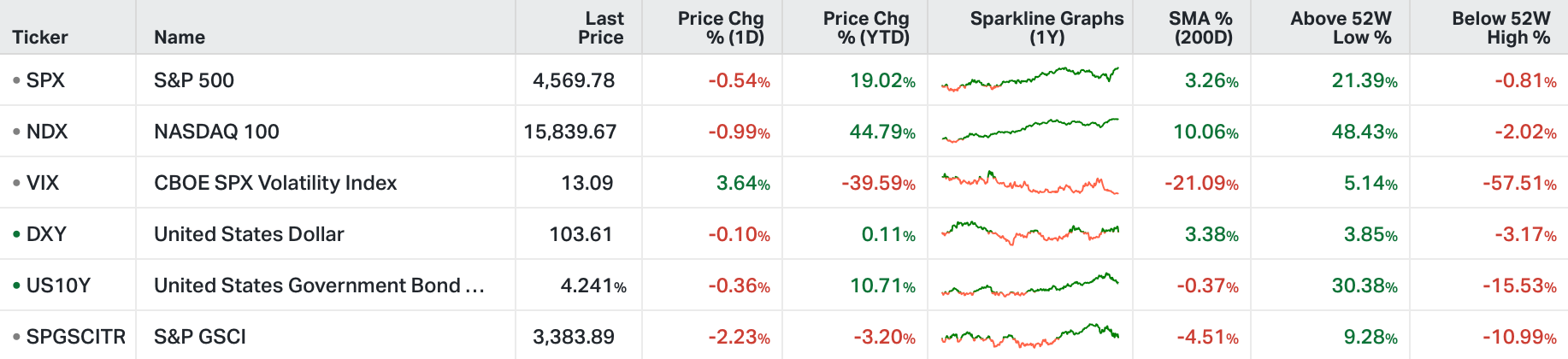

the bond market (higher bond yields),

the stock market (lower stocks),

the dollar (stronger).

All of these market measures have since reversed course.

That said, he did nothing to push back against the market expectations on rates, which now projects the next move as a rate cut (perhaps as early as March). Notably, in his prepared remarks he included a footnote directing attention to the way the Fed measures financial conditions - its new index to gauge the impact of financial conditions on future economic growth. Let's take a look at where that new index stands ...

This index is designed to incorporate the lags of monetary policy, and project (in this case) one-year forward what the impact will be on real GDP growth. If the line is above zero, it's a drag on growth (restrictive policy). If it's below zero, it's a boost to growth (stimulative policy).

So, when factoring in the current Fed Funds rate, the 10-year yield, the 30-year fixed mortgage rate, the lowest investment grade corporate bond rate, the DJIA stock market index, the Zillow house price index, and the value of the dollar, the Fed's new index projects a nearly 1% drag on real GDP one-year forward.

Does it mean recession is indeed coming? Keep in mind, this index has been in headwind territory for economic growth since the middle of last year, which would project a drag on recent growth, yet Q3 grew at a 5.2% annual rate.

Despite the pains, it's a strong economy.

For perspective on the outlook, let's take a look at what this financial conditions index looks like with some longer history …

As you can see in this longer term chart, these current levels tend to be turning points for financial conditions.

Remember this is projecting the effect on growth one-year forward. If we look at stock market performance one-year forward from these historical turning points (in the chart), stocks do very well in the subsequent 12-month period . . . and small caps outperform.

This aligns with the rotation trade we discussed in my last note, where money appears to be moving out of the dominant big tech stocks (which put in technical reversal signals last week) and into small caps, which have (dramatically) lagged in performance on the year.

Attached below are two chartbooks from Gryning | Edge & Gryning | Capital - please forward and share with those you feel may find them of value.