Fed's Bluff & Strategy

Macro Perspectives

The WSJ wrote a lengthy piece yesterday on the topic we've been discussing here in my daily notes.

This is the Fed lamenting the disconnect between the markets, and the narrative the Fed wants the markets to follow (and using the journal as the mouthpiece).

The narrative: The Fed is working to expeditiously bring inflation down - that implies rapidly rising rates and much tighter financial conditions (more expensive money and tougher to come by).

The markets: The 10-year yield has fallen back from 3.5% down to 2.88%. Stocks have rallied 17% off of the lows. All of this in the past two months.

Translation: The market has stopped believing the Fed's hype.

And for good reason. They have been bluffing!

Remember, the former Fed Chair, Ben Bernanke, once said that the Fed can raise rates in 15 minutes to deal with inflation, if needed. Well, the current Fed has certainly made it clear that the present inflation situation is a significant threat. So, have they done a one-off, large scale emergency interest rate hike, to recalibrate economic activity and consumer exuberance? No.

First, they watched the clear formula for inflation, as it was launched back in March of 2020 through the Cares Act. Free money was literally dropped into the hands of consumers and businesses, with expectations of more to come.

Next, they had clear evidence of the resulting inflation more than a year ago, as the core inflation rate sustainably spiked to double the level of their target rate of 2%.

Did they act? No. They watched and even denied the durability of inflation (despite the clear formula of cash handouts, otherwise known in the central bank biz as "helicopter money"). And then, after they verbally pivoted and promised an outright attack on the inflation problem, they continued to execute their QE program for another five months (i.e. they continued to juice the economy and fuel the very inflation they were promising to attack).

Fast forward to today, and here we are with inflation at 8.5%, and the Fed Funds rate at just 2.5%.

Remember, historically, to beat inflation, short-term rates need to rise above the rate of inflation. The Fed is not close. Add to that, after telling us they would aggressively drain the liquidity they have added to the financial system over the past two years, they have done just a tiny fraction of their scheduled plan, thus far.

Bluffing.

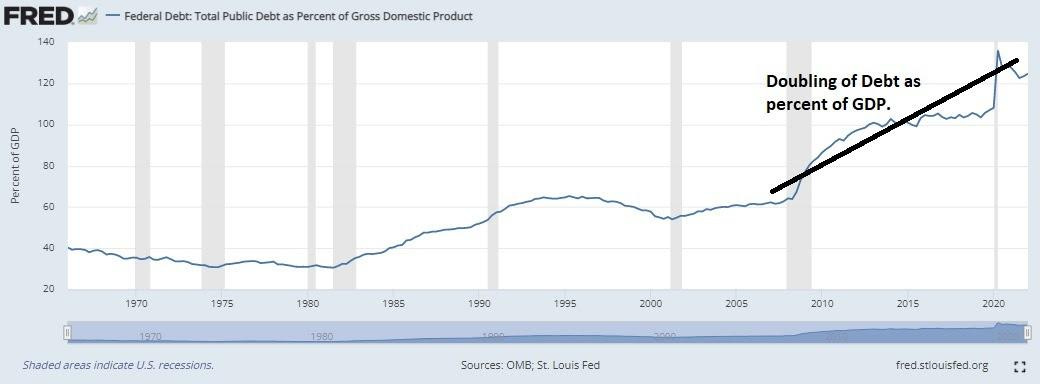

Why? Unsustainable sovereign debt (not just in the U.S., but globally). As you can see below, U.S. debt as a percent of GDP has doubled since the Great Financial Crisis. If the Fed were to raise rates by the 600 basis points, to the level of current inflation, the annual interest the U.S. would pay on the debt would balloon to over $1.5 trillion (from the current $400 billion).

And as we've discussed, even if the U.S. could handle it, the rest of the world couldn't. It would set off a cascade of sovereign debt defaults.

The strategy at work: Inflate the denominator (growth), and inflate away debt relative to the size of the economy.

Short Squeeze Candidate

Bed Bath & Beyond has been in news - Twenty-year-old Jake Freeman amassed big stake (~6%) in struggling retailer before share price soared, making $110 million.

https://www.ft.com/content/1b21bb08-6590-49c6-8baa-5ad8c527fbcc

My Thoughts: This young man played a blinder. It was a short squeeze play but less of a meme stock play - had the share price dropped whilst he held, he would have likely got himself onto and enacted management change a la activist hedge funds.

Out of interest I scanned the market for short squeeze candidates and Transocean Ltd stood out (despite the 8.83% uptick yesterday). This is not part of my investment mandate, so I purchased 1 (one) option as a means to keep track - sharing this as an observational post.