Fed: Risk skewed towards?

Macro Perspectives: Fri 07 Jan 22

The comparisons are being made between the current wind down of QE (and projected rate tightening cycle), and the "taper tantrum" of 2013.

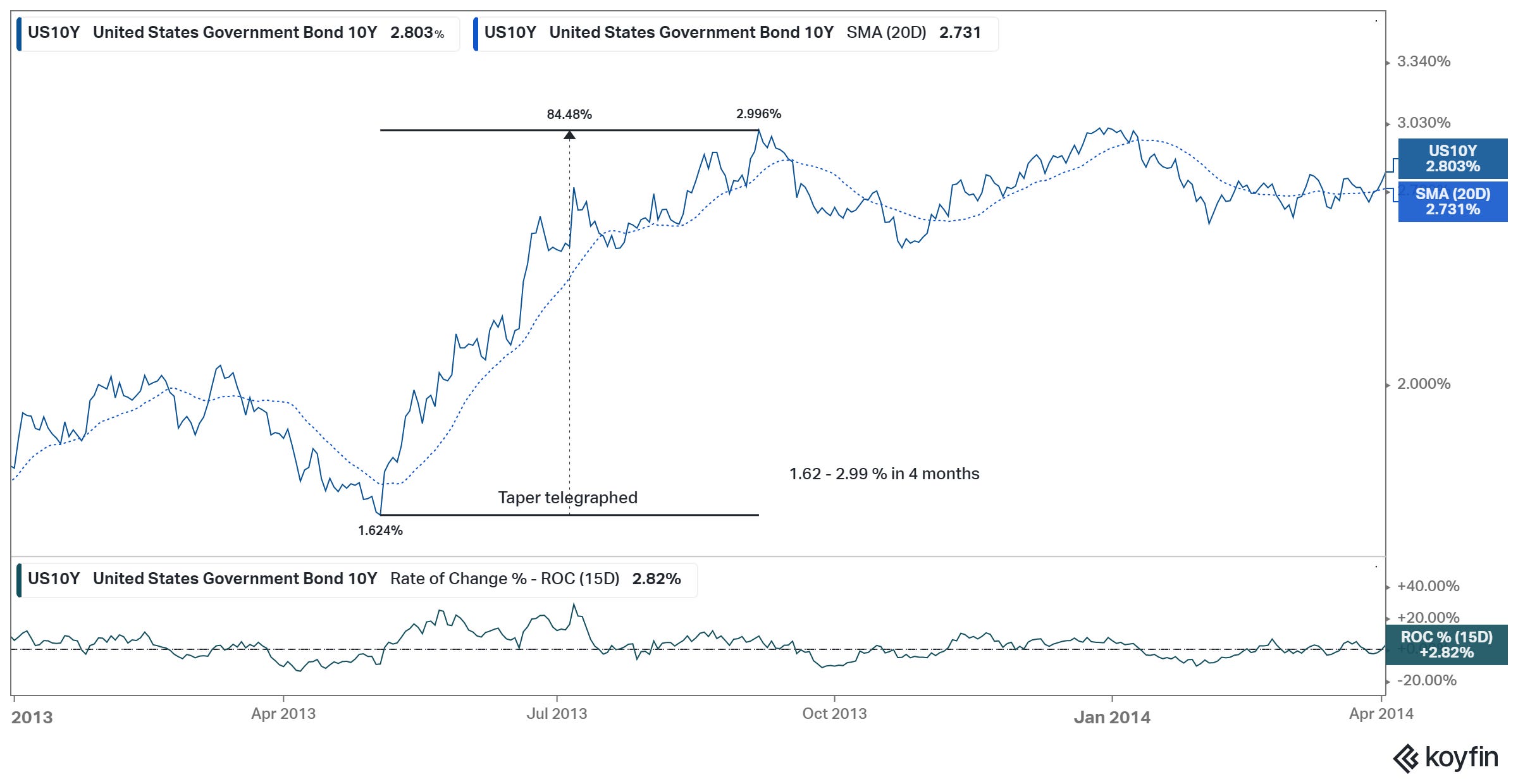

To recap, back in May of 2013, after three rounds of QE, Bernanke indicated that the Fed would begin winding down QE by the end of the year. The interest rate market did this...

This time around, the Fed's July 2021 minutes hinted toward a tapering of QE by year end. The 10-year yield has since done this...

What was/is a big difference between now and then?

In 2013-2014, with a soft-fragile economy, and inflation running around 1.5%, the risk of a Fed policy mistake was skewed toward the Fed being too aggressive (pre-mature) and crushing feeble growth. With that, after the knee-jerk reaction in the interest rate markets, the 10-year yield ultimately gave way to a more rational level of around 2%.

What about this time? Inflation is hot, the economy is hot. The risk of a policy mistake is skewed toward the Fed being too late, and not aggressive enough. With that, the likelihood of a sharp spike higher in market interest rates, after the Fed exits the bond market in March, is high.

For perspective, the last time inflation was here (6.8%) the 10-year yield was 13.6% (March of 1981).