Fed as Expected, Summer Rate Hike.

Macro Perspectives: Thu 04 Nov 21

The Fed announced the beginning of the end of QE. The plan looks very much like the plan we discussed in my Tuesday note - they will cut their monthly bond buying program in equal amounts, to end in June of next year.

This "tapering" plan is coming earlier and with a faster timeline than they led us to believe and this timeline opens the door for the possibility of a mid-year rate hike.

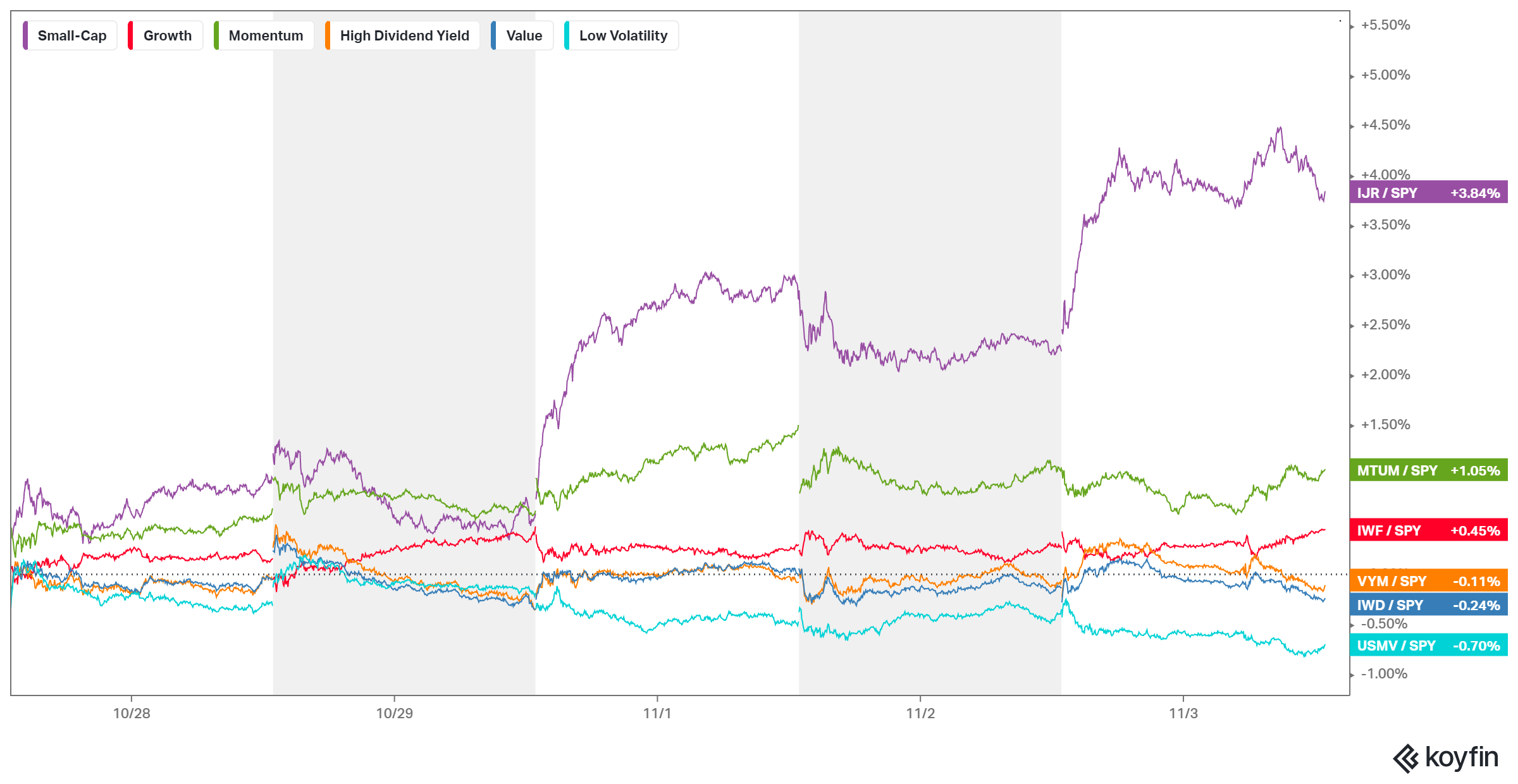

But in his press conference in the afternoon, Jay Powell wouldn't go anywhere near a discussion on the liftoff of interest rates. Powell danced around the scrutiny over the interest rate outlook, justifying the Fed's position by pointing to the labor situation, and the uncertainty surrounding the forces that are driving inflation (will they abate?). His subdued tone on inflation and the rate outlook was/is fuel for stocks - stocks traded to another new record high.

He, however, did have more uncertainty introduced overnight. The gubernatorial elections in Virginia and New Jersey may have changed the policy winds on Capitol Hill. These proxy votes on the radical and disruptive policies of the democrats, should only embolden intraparty resistance to the "big spend" agenda.

As we've discussed in past notes, at this stage, a smaller deal, or (even better) a no deal, would be among the best outcomes for markets and the economy. It would be a relief valve on inflation pressure and it would remove the obstruction of uncertainty on a recovering economy that already has $5 trillion of excess money floating around.