Fed - all about the Tightening...

Macro Perspectives

The Fed meets on policy today.

Following Friday's hot inflation report, the market has now priced in a more aggressive 75 basis point rate hike - that would take the effective Fed Funds rate to 1.5%.

The problem is, as we discussed last month, there are three supply issues that are driving inflation, that the Fed's interest rate ammunition can do nothing about.

1) The reset of wages at the low end of the scale. Thanks to pandemic unemployment subsidies, the government established a new (higher) living wage that's being passed on to consumers through higher prices.

2) The global supply chain disruptions from the lockdown period have been exacerbated by war in eastern Europe and zero covid policies in China.

3) High energy prices, sustained by a self-inflicted supply shortage, by the design of global anti-fossil fuel policies.

These factors will keep a fire under prices, regardless of whether the Fed sets interest rates 50, 75 or even 100 basis points higher. From this point, a more aggressive rate path will ensure a lower quality of life, more so than it will ensure lower prices. And that is being projected in this chart...

This is the spread between the 10-year and 2-year Treasury yields (the yield curve) - the yield curve is near a second inversion in three months.

Why does this matter? Each of the six recessions, dating back to 1955, were preceded by a yield curve inversion. Recession followed between 6 and 24 months.

Now, what we should be watching closely is what the Fed says about quantitative tightening - it officially started on 01 June 2022.

As we've discussed here in my daily notes, there's one thing we know about historical central bank exits of QE - they don't last long…

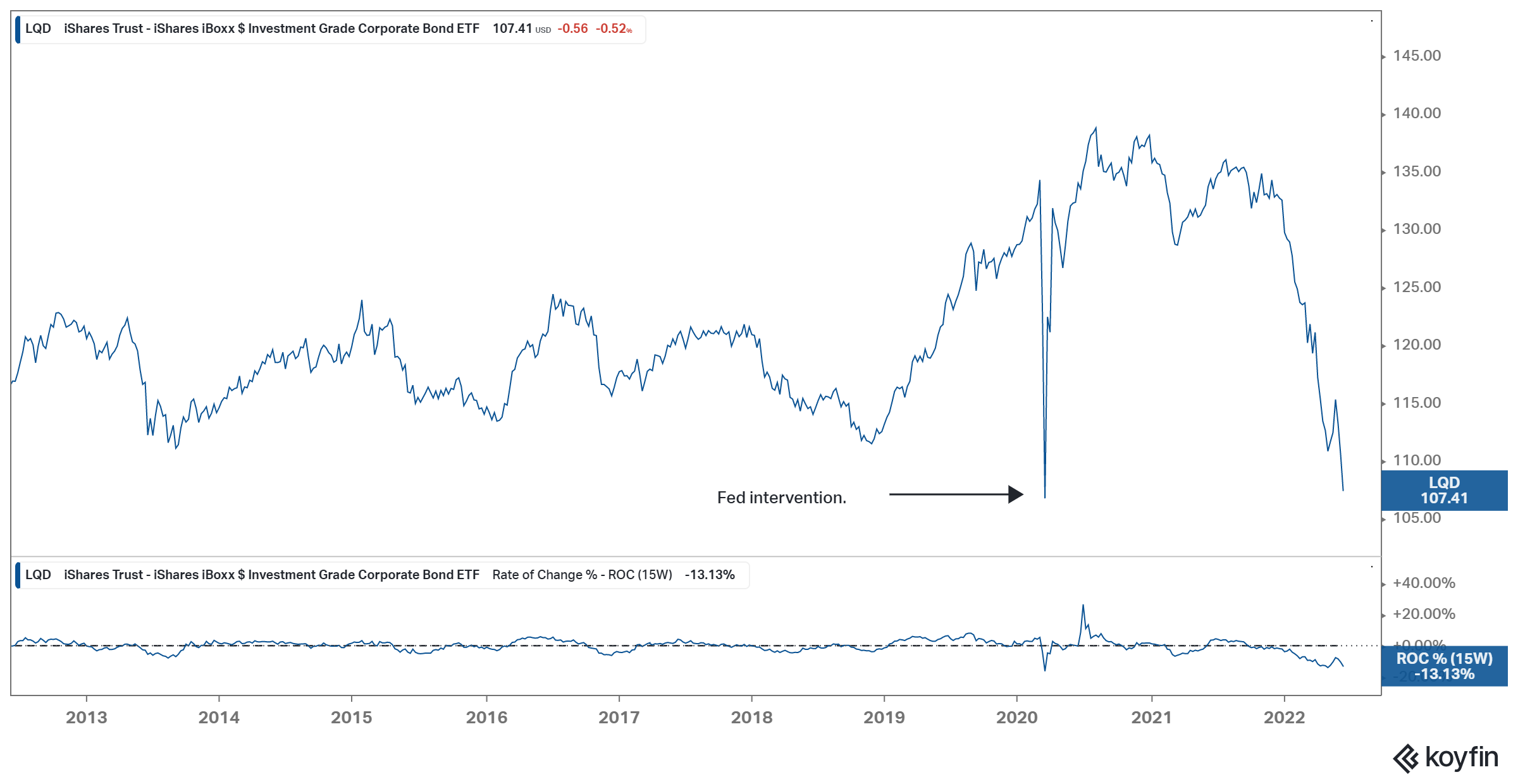

Things tend to break. Already, the bubble has been pricked in the latest iteration of the internet boom, including the end of the mania in crypto currencies. But the real trouble, when central banks start extracting liquidity from the economy, tends to come from the interest rate market. Back in the depths of the lockdown-induced financial market crisis, the Fed wasn't able to get markets under control until it tamed the corporate bond market.

It did so by crossing the line - and outright buying corporate bonds (individual bonds and ETFs). You can see how that Fed intervention/rescue looked in the biggest corporate bond ETF, and you can see where it's trading now (back to the depths of the crisis).