$FB - Growth play at low Valuation

Macro Perspectives: Wed 09 Feb 22

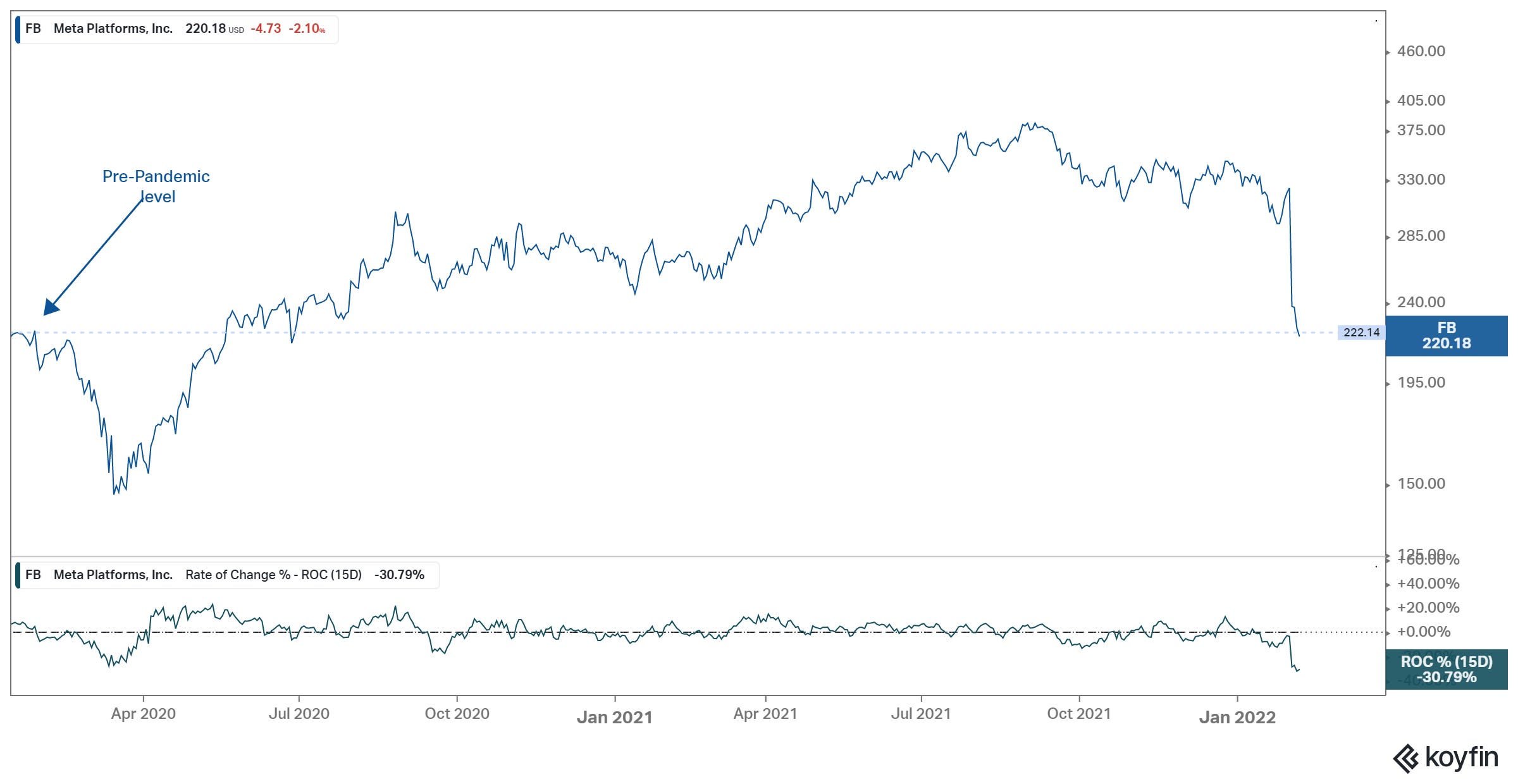

Let's take a look at Facebook.

The stock closed below pre-pandemic levels - down 34% in just the past five trading days.

As we've discussed for quite some time, a rising interest rate environment is bad news for high valuation, high growth stocks.

Despite its size and maturity (being part of the "big tech" oligopoly, and having garnered a trillion-dollar valuation just months ago), Facebook remains a high growth stock. For 2021, the company grew revenues at 37% and operating income by 42% (year-over-year).

With that, as Wall Street contemplates factoring in a discount rate (interest rate) in their valuation models, the valuation comes down. But how far is too far?

Consider this: Facebook was trading north of 25 times earnings before Jay Powell's pivot on the inflation outlook late last summer. Today, it's 16 times. That's now in-line with the long-term broader market multiple and its the cheapest valuation on Facebook since becoming a public company (which means, in the history of the company, including its history as a private company).

So, today you get a high growth company with a dominant market position, with 40% operating margins, at a long-term average broad market multiple. It's a buy.