Expanding of the Fed balance sheet is not QE.

Macro Perspectives

The Fed hiked another 25 basis points - that takes the Fed Funds rate to the 4.75%-5% range.

The Fed Funds rate is above the rate of inflation, where, historically inflation has been beaten - core PCE, the Fed's favored inflation gauge is 4.71%.

That said, after the rate hike, Jerome Powell (Fed Chair) actually made a strong case for why they should have done nothing (paused). He talked a lot about the credit tightening that they think is "quite real," in his words. In fact, he said directly that the banking stress of the past two weeks, and related credit tightening, has an equivalent effect of a rate hike, and will weigh on inflation.

With that said, given that the level of interest rates has been a catalyst for breaking things in the financial system, why did they take the risk of another rate hike, and do so unanimously (no dissenting voters)?

The market had priced it in, and there was plenty of Wall Street and media commentary suggesting that a pause would signal to markets that the Fed was aware of some deeper trouble in the banking system - it does appear that the Fed caved to that sentiment.

Still, up front, in prepared remarks, Powell assuaged concerns about financial system risks, saying the actions they've taken (providing liquidity to the troubled venture capital-related banks) "demonstrate that depositors' savings and the banking system are safe."

Overall, the markets were satisfied with the idea that the Fed said the banks are sound and depositors are safe, AND that they were likely done with rate hikes, while (importantly) back to expanding the balance sheet.

Stocks went up.

Commodities went up.

Market-determined interest rates went down.

The dollar went down.

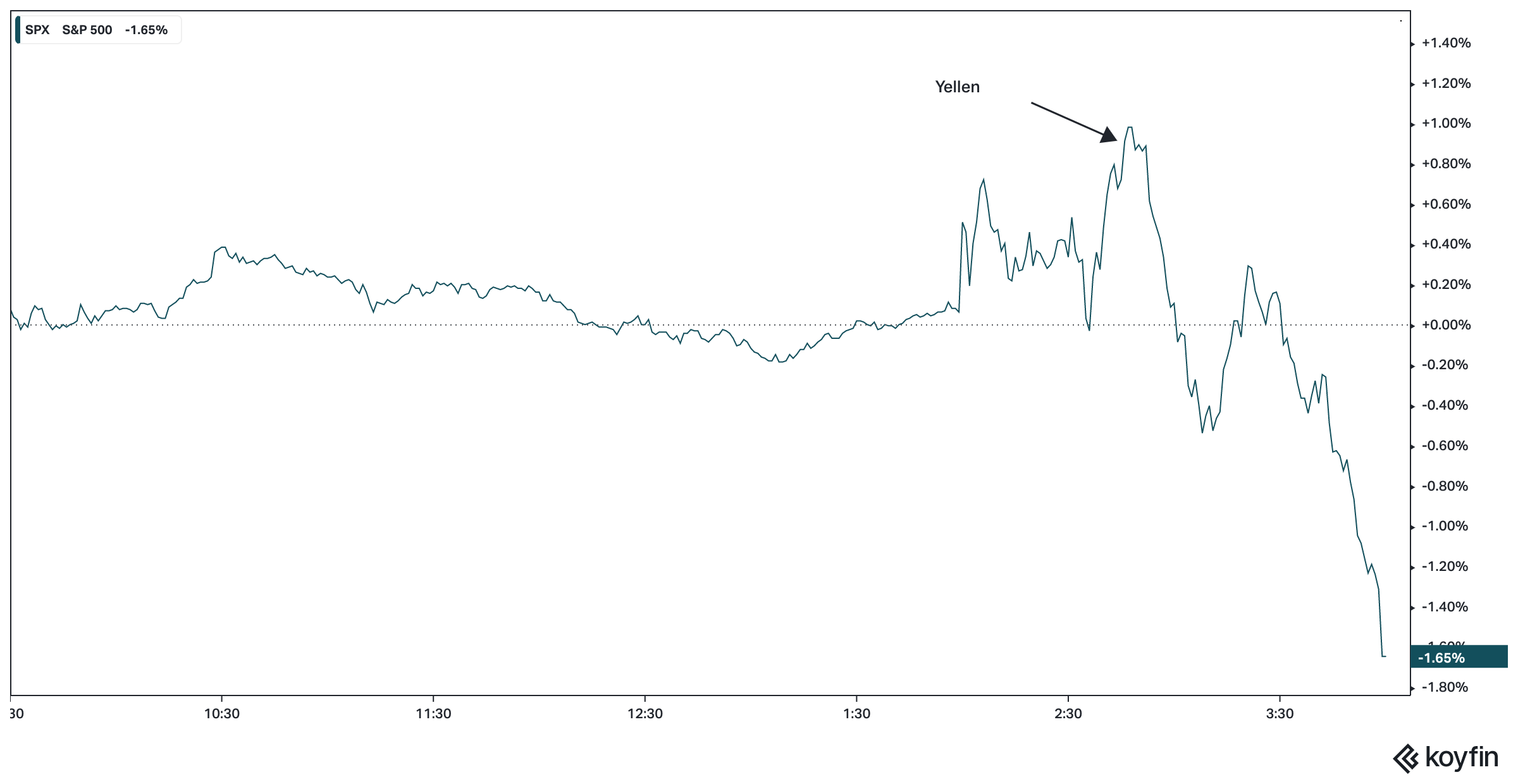

All market signals that the Fed is done. But then stocks did this…

As Powell was holding a press conference, Janet Yellen (the Treasury Secretary) was sitting before the Senate Appropriations Subcommittee. Just after Powell implied "all depositors" are safe, this comment from Yellen hit the wires:

"We are not considering insuring all uninsured bank deposits."

In fairness, it was a response to a question from a Senator about the requirement of Congressional approval to increase FDIC insurance limits. Nonetheless, you can see in the chart above the impact that comment had on the stock market, particularly because of this stock (below), which has been the one of the three troubled U.S. venture capital-related banks that is still standing (barely)…

First Republic has already had an infusion of deposits from a consortium of big banks (arranged by the Treasury). They may have to do more. If so, they will (Fed, Treasury). For perspective, this continues to be confined to a few unusual banks, with unusually high uninsured deposits, and with concentrated groups of depositors.

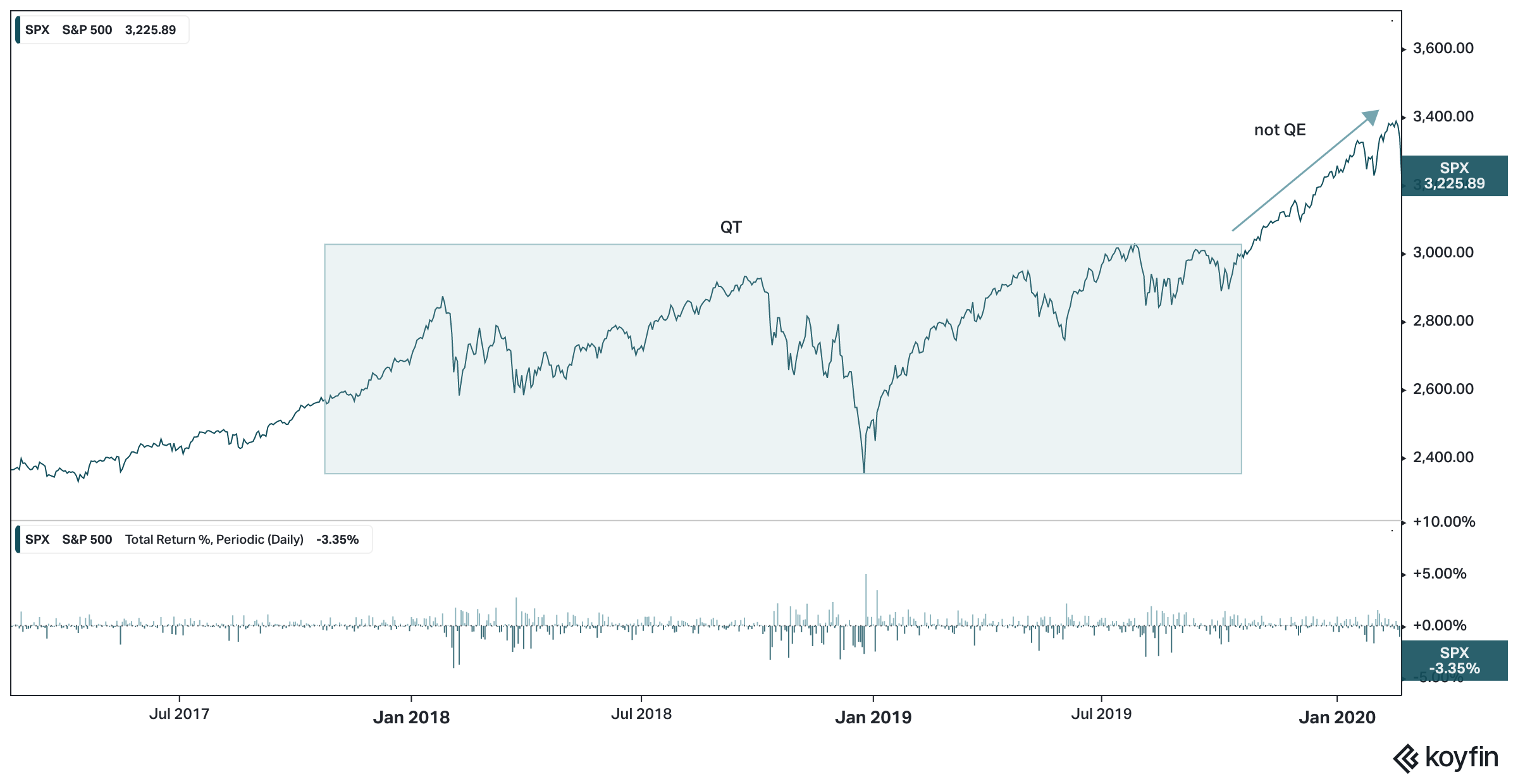

On a final note, Powell was asked about the Fed's return to expanding the balance sheet (in response to the confidence shock in part of the banking sector). He wanted to make clear that this "expanding of the Fed balance sheet," is not QE.

This sounds familiar.

From 2017-2019, the Fed attempted to shrink the balance sheet (quantitative tightening), trying to reverse its massive response to the Global Financial Crisis (three rounds of quantitative easing - QE). Things started breaking in the financial system - specifically, we had a 300 basis point spike in the overnight lending market.

By late 2019, they quietly returned to expanding the balance sheet again.

By the time Jay Powell acknowledged it, in a prepared speech (in October of '19), they had already bought $200 billion worth of assets. When questioned, he downplayed it, saying it was "not QE."

Stocks behaved as if it was QE...

GRYNING | Gamma is how you access AI powered stock picking.

Get unique insights, boost your portfolios, and make smart data-driven investment decisions.

GRYNING | Portfolio is for those looking for long-term market insights with tactical trading strategies, technical and uniquely agnostic views.