Election Flows

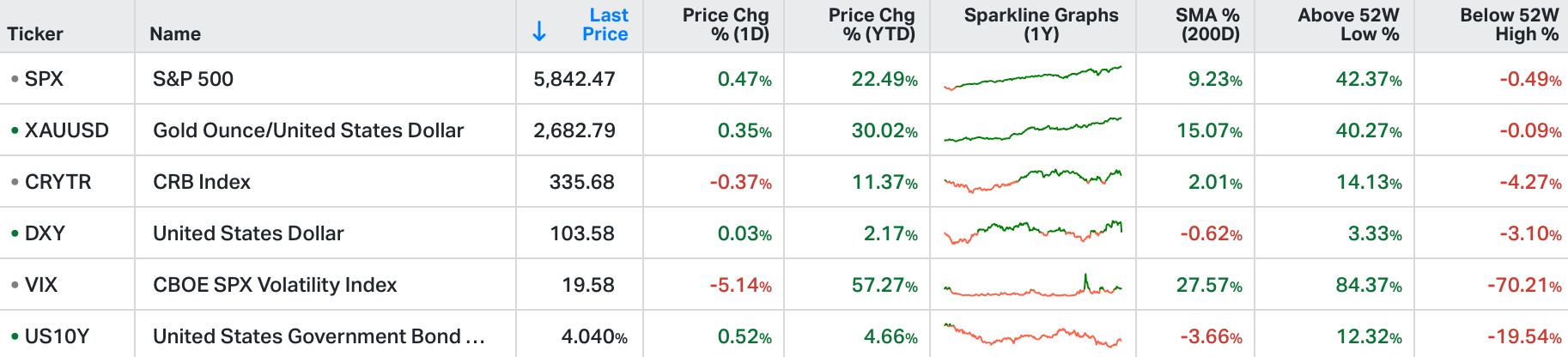

Stocks in the US closed mostly higher on Wednesday, partially recovering some of the previous session’s losses.

The S&P 500 gained 0.5%, the Dow Jones advanced 337 points to close at fresh record, while the Nasdaq 100 finished marginally higher.

Traders continue to focus on corporate results with Morgan Stanley gaining 6.5% after the company's earnings and revenue topped estimates.

Also, Abbott added 1.5% as its quarterly results were slightly stronger than expected.

Meanwhile, Intel lost 1.4% after the Chinese cyber association called for review of Intel products sold in China.

Yesterday we talked about the view on the U.S. presidential election from the betting markets. A swing in favour of Trump took place last week, and has continued through this week.

Are there any reflections of this outlook in financial markets? Maybe.

Sector performance over the past week has been led by financials.

What performed best into the end of the year following the 2016 Trump election? Financials ($XLF) rose 17% from election day into the end of 2016, after Trump was elected.

Energy, industrial and material stocks also did very well in that immediate aftermath of the 2016 election. The Russell 2000 and Dow are heavily weighted in financials, energy, industrials and materials stocks - both indices are outperforming the S&P 500 and Nasdaq since early last week.

Part of the Trump economic agenda is defending the "right to mine Bitcoin." Bitcoin is up 9% from early last week.

And as you can see below, as the betting market on the probability of a Harris win has declined, so has the biggest Clean Energy ETF (an investment theme contingent on the Biden/Harris agenda).

Where else might we see market positioning for a rising probability of a Trump presidency?

The Chinese central bank offset Trump tariffs during his term by weakening the yuan against the dollar (making Chinese goods cheaper in dollar terms to mitigate the impact of a cost increase to end users from tariffs). The yuan is down 1.5% from early last week.

In the seven weeks surrounding the 2016 election (early October through late November), the Chinese central bank made the largest seven week devaluation of the yuan since adopting the managed float exchange rate regime back in 2005.