Economy Waning, Revenue Hot.

Macro Perspectives: Fri 29 Oct 21

Third quarter GDP did indeed come in softer than expected.

Yesterday we talked about the prospects of a negative surprise in this number, maybe even a negative number (i.e. economic contraction) - it came in at just 2% (annualised quarterly rate). That's below long-term trend growth for the economy and it's very soft in a world that is still bouncing back from an economic shutdown, and teeming with economic stimulus.

For perspective, we started the year with estimates for growth for the full year to be better than 6% - and maybe even as high as double-digits. In the first and second quarters, the economy was indeed running at a better than 6% rate (6.3% and 6.7%, respectively).

As we discussed yesterday, the drag was already showing in the consumption data - dating back to the August consumer sentiment survey, we knew that consumers were pulling back. Let's take a look at the BEA's report for just how much they reined in spending in the quarter.

Consumption is about 70% of U.S. economic output and as you can see in the table above, that measure (Personal Consumption Expenditures) fell off a cliff in Q3: going from +11.4% (Q1), to +12% (Q2), to +1.6% in Q3.

The big drag? Durable goods. People stopped buying big ticket items. Is it because of prices? Is it because, by the third quarter, it was clear that these items wouldn't be delivered to your doorstep anytime soon?

In my previous note I pointed to the economist(s) that conducted the August University of Michigan Consumer Sentiment survey explaining it this way: "The reaction of consumers to rising prices has been to postpone purchases, given their fears of falling future living standards..."

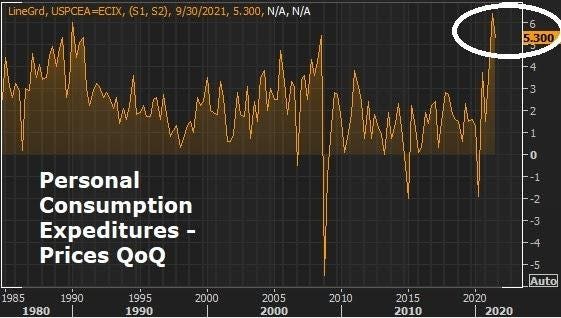

How did prices look in the quarter in the face of waning demand? Still hot.

So, how are companies putting up record earnings for Q3, when the economy slowed?

It may have a lot to do with the order backlog. The widget you ordered in the first quarter, isn't officially revenue until it's delivered to you (maybe in the third quarter, in this logistics environment). So corporate America may have plenty of revenue fuel for the coming quarters, even while seeing softer demand.