ECB & global sovereign debt default contagion.

Macro Perspectives

We talked yesterday about the big barrier to meaningful interest rate increases - Sovereign Debt.

Debt is at record levels. And it's growing, thanks to the even deeper (than pre-pandemic levels) deficit spending that first backstopped consumers and businesses from a lockdown apocalypse, and later funded the global political agenda. With that, if we add a slowing economy, to rising debt service costs (from central bank tightening), we get a formula for a debt spiral.

The central banks know this. That's why they are attacking demand, verbally, to influence confidence (down), and therefore demand (down) - they get the desired effect of slowing the economy, without having to meaningfully raise rates.

The European Central Bank meets today on rates. Inflation there is running 8%. Yet they've continued with pedal-to-the-metal policy - negative deposit rates, and QE. The expectation is for the ECB to announce the end of QE, and project a first (post-pandemic) rate hike in July.

ECB policy, and the related outcomes in Europe, are very, very important to global economic stability (or instability) - the biggest risk of a global sovereign debt default contagion comes from Europe.

It was only a decade ago that Mario Draghi (ECB President, at the time) averted disaster for Europe and the global economy - a contagion of global sovereign debt defaults were lining up in Europe. The second most widely held currency in the world, the euro, was vulnerable to a break-up. To stop the meltdown, Draghi publicly threatened/vowed to become the backstop in the European government bond market.

Here's what he said in a July 2012 speech: "the ECB is ready to do whatever it takes to preserve the euro. And believe me, it will be enough.”

The imminent risk was sharply rising yields in the big, dangerous weak spots in Europe: Spain and Italy. Speculators were hitting the bond market, yields were rising to unsustainable levels. Spain and Italy were on the path of default - and once one went, the others would fall. The next step would mean these countries leaving the euro, returning to national currencies and inflating away the debt through currency devaluations.

It didn't happen because Draghi stepped in.

With the statement above, he threatened to be the unlimited buyer of these troubled government bonds, which was enough to purge the speculators from the market, and reverse the capital flight - the yields on those bonds plunged.

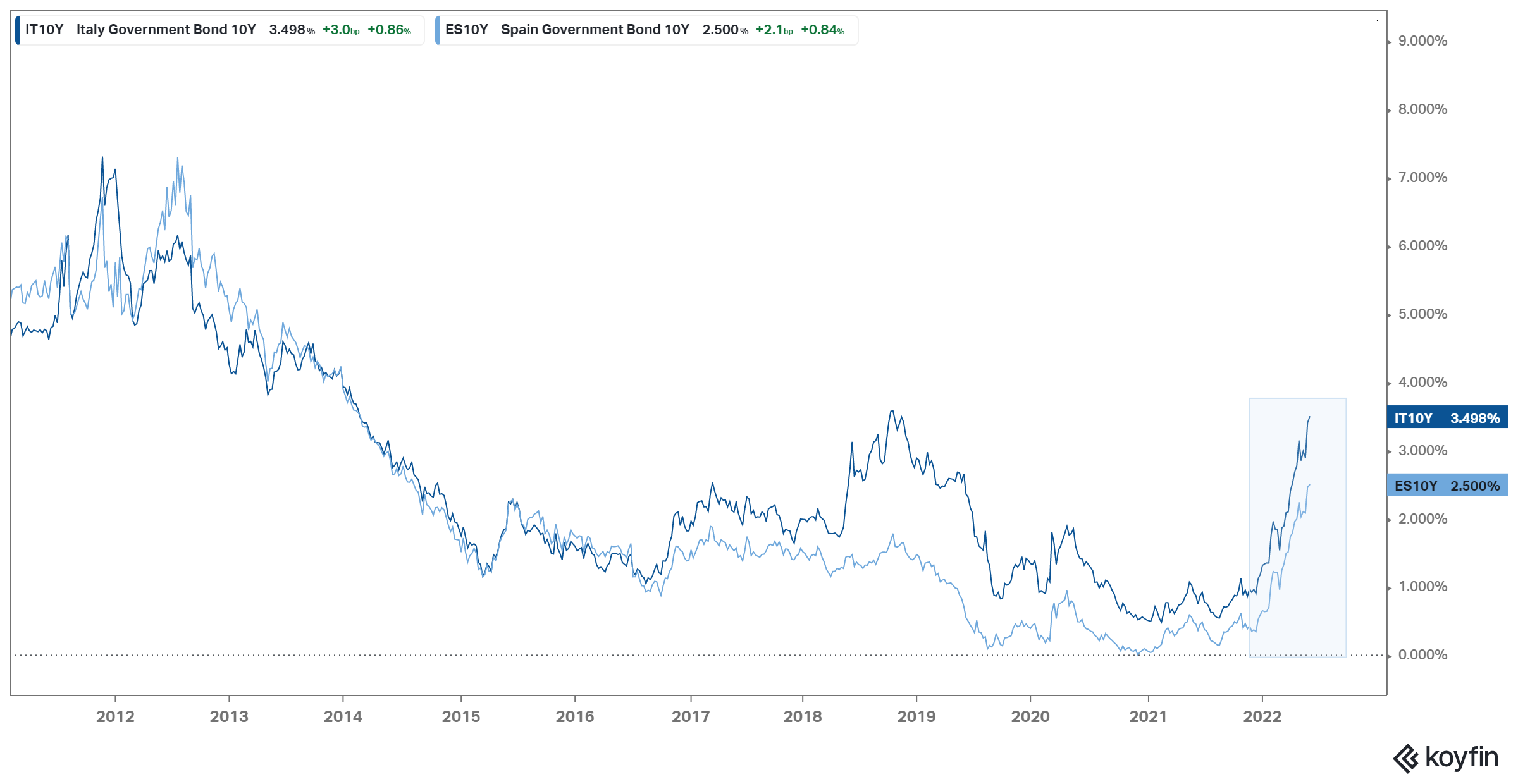

Here's what the chart of those bond yields looked like before and after Draghi's line in the sand...

As you can see in the chart, when yields for both Italy and Spain were around 7%, back in 2012, they were on default watch; Italy's debt load was 126% of GDP, Spain's was 90%.

Now, fast forward to today...Though deposit rates are at negative 50 basis points in Europe, and the ECB is still buying assets (which include government bonds in Europe), sovereign bond yields in the weak spots in Europe, Italy and Spain, have been on the move, higher.

Today Italian yields have popped to 3.5% and Italian government debt is 150% of GDP. Spanish yields are at 2.5%, with debt at 118% of GDP.

It doesn't take much imagination to see the danger zone for these two countries emerging quickly, if the ECB were to telegraph a series of rate hikes, while simultaneously ending QE (which has been their explicit tool to outright control the bond yields of these fiscally fragile countries).