Earning's Season Kick Off

Macro Perspectives

We've spent the week talking about the setup for a weak inflation report, and a bullish breakout in stocks.

We got the former. The latter is yet to be determined.

As expected, there were well-placed Fed speakers, lined up, following the morning's inflation data, ready to counter the optimism about the prospects of a less restrictive Fed, with promises that they would not be less restrictive.

The credibility of the Fed's tough talk is rapidly deteriorating, as the monthly change in prices, over the past seven months, averages to just 0.12%. Annualise that, and inflation has been running below the Fed's 2% inflation target, for many months now.

The focus now turns to earnings and the health of the economy. How much damage has the Fed done to consumer and business behaviors?

Earnings season will kick off today, with Q4 reports from all of the big banks. The head of the largest bank, Jamie Dimon, said earlier in the week that the consumer is still strong, balance sheets are in good shape, and "they are spending more than pre-covid."

Those comments give us nice clues on what the banks should say today. With this in mind, let's take a look at how the economy performed during this Q4 period.

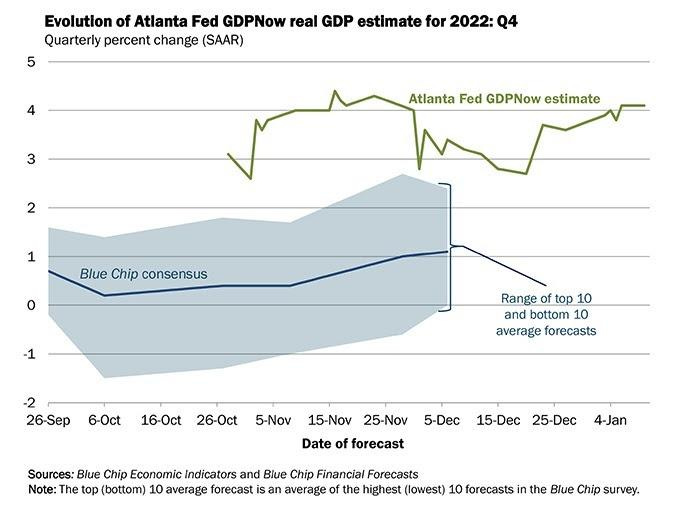

As you can see in the above, the Atlanta Fed's model (the green line) has Q4 GDP growth at better than 4% annualised. Importantly, you can see in the same chart that Wall Street's projection (the blue line) has been much lower, all along the way.

If we look at Q4 earnings expectations, it should be no surprise that the Wall Street analyst community has spent the past several months dialing down earnings expectations for Q4. They've gone from expecting 3.5% earnings growth (back in September), to the expectation of a 4.1% decline now.

So, we'll see in the coming weeks, if the street was as wrong on earnings as they appear to have been on Q4 growth.