Early Stages Bull

Macro Perspectives: Mon 28 Feb 22

There has been plenty of attention given to Russia/Ukraine, and the swings in stocks over the past week.

Let's start the week with some perspective on global markets and asset prices, as we approach the Fed's official end of emergency policies (just weeks away).

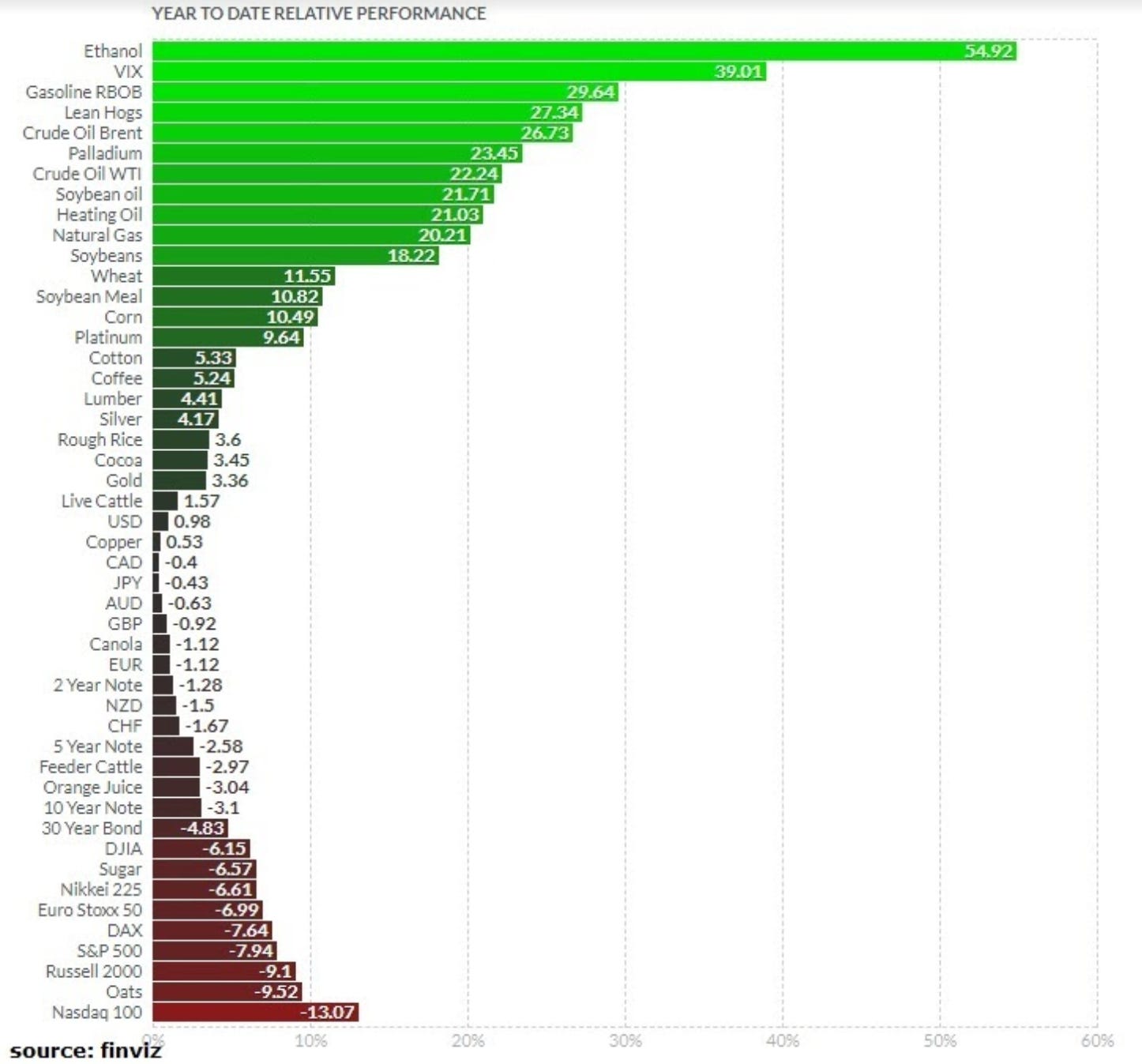

In the graphic above, you can see commodity prices continue to rise. This is consistent with an inflationary environment, where the Fed has intentionally left themselves behind the curve, to let prices run hot.

But there is more to it. This is a longer-term secular trend underway - a repricing underway of real assets, relative to financial assets.

As we've discussed over the past few years, commodity prices have been at historically cheap levels, relative to stocks. In fact, only two other times on record, have commodities this cheap:

at the depths of the Great Depression in the early 30s,

in the early 70s (which was at the end of the Bretton Woods currency system).

Commodities prices went on a tear both times.

The last time commodities were this cheap, relative to stocks, a broad basket of commodities returned 50% annualised for the next four years - up seven-fold over 10 years.

We've looked at this chart many times…

Along with the deflationary forces of the post-financial crisis, commodity prices were flashing depression-like signals. We may not have recognised it so easily, given the buffer of trillions of dollars of central bank intervention (which manufactured sluggish growth).

Now, we have a massive government spending response (fiscal), inflation, a boom in commodities, and likely the early-stages of an aggressive economic expansion (finally).

With that, the new bull trend in this chart above is in the early stages.