Drunkenmiller & Liquidity

Macro Perspectives: Thu 10 Sept 2020

One of the great macro-traders of all time, Stan Druckenmiller, was interviewed yesterday.

Having followed his career and thoughts throughout my time in the financial markets, I find his view points particularly interesting - he tends to understand the big picture as well or better than anyone, particularly as his view is shaped by global liquidity, and he has a lot of influence.

As we know, with the Fed and Treasury acting in coordination (together and with other global central banks and governments), the world is swimming in money. With that, in environments where central banks are active, Druckenmiller tends to have a very valuable perspective.

Back in early December of 2018, Druck said he was "on red alert" for markets to crack. At the time, the Fed and the ECB were combining to land a one-two punch for global markets and the global economy. The Fed was overly aggressive in tightening into a slow growth, low inflation economy, while the ECB was simultaneously ending its three-year QE program. Liquidity was being extracted.

Despite some warning signals, the Fed went through with another rate hike in mid-December, and stood its ground on the policy path - the gut punch. U.S. stocks collapsed 18% in fifteen days, and by the beginning of the year the Fed was walking it back and ultimately reversed course.

As we headed into 2020, Druckenmiller was interviewed again. This time, he thought the Fed was on the wrong side again - swinging the pendulum too far in the opposite direction (overly easy). He thought global growth would positively surprise and he thought the Fed would be caught behind on inflation.

A month into the year, all appeared to be on the path, until the pandemic hit. So, for a "liquidity" driven investor, we now have trillions of dollars of new money in the economy. What does he think now?

He thinks we are set up for an inflationary boom (if they get it right), or a deflationary bust (if they don't) - with a low chance of getting it just right.

He says valuation on stocks doesn't matter, because of the Fed/Treasury liquidity, with inflation able to hit 10% in the coming years.

This is in line with much of what we've been discussing here in my daily notes. For what it means, let's look back at an excerpt from my Aug 28 note...

"Remember, this will be a recovery juiced by trillions of dollars of excess money from the policy response (well in excess of the damage). That means the Fed will likely have to chase inflation at some point, to contain it, with a rapid succession of rate hikes, they will still let it run hot, early on. This is still a good scenario. That bad scenario is deflation, due to economic collapse, which means a very bad outcome for all, and unlikely salvageable by even aggressive policy actions.

Let's stick with the optimistic (high probability) outcomes…

Guess what will 'inflate' along the way in these inflation scenarios: Nominal GDP - measures the market value of the goods and services. So, price goes up, GDP goes up.

If we look back to the inflation spikes of the early 70s and early 80s, nominal GDP grew by an annual rate of better than 10% during those periods. If we had a similar spike, we would regain peak levels of GDP by middle-to end of next year, and we would be on the way to a $30 trillion economy by 2024, which would (by design) go a long way toward repairing, if not resolving, our debt as a percent of GDP problem."

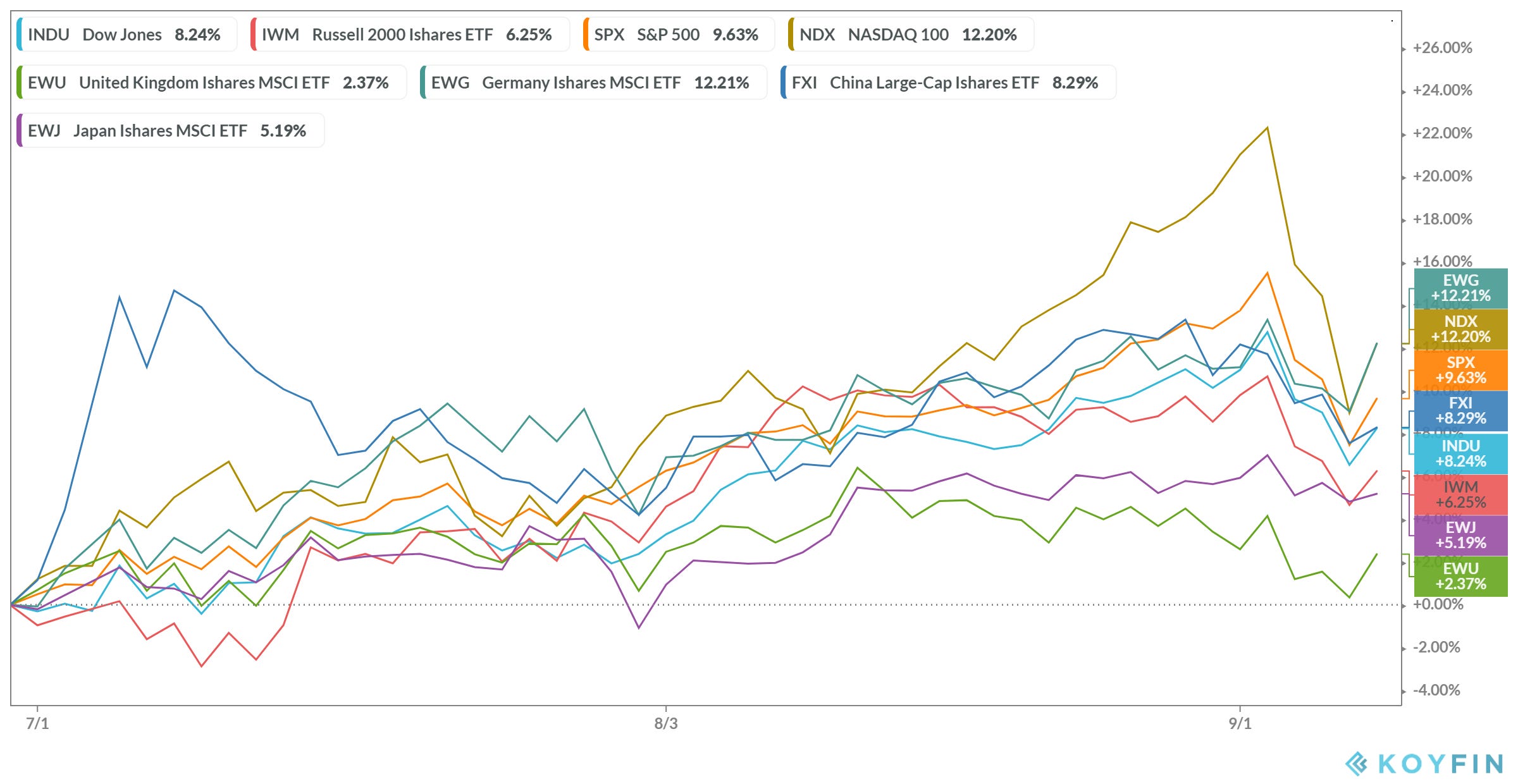

With just under 3 weeks left in Q3 andaccounting for the recent pull-backs in global equity, here is how we stand going into the business part of H2.