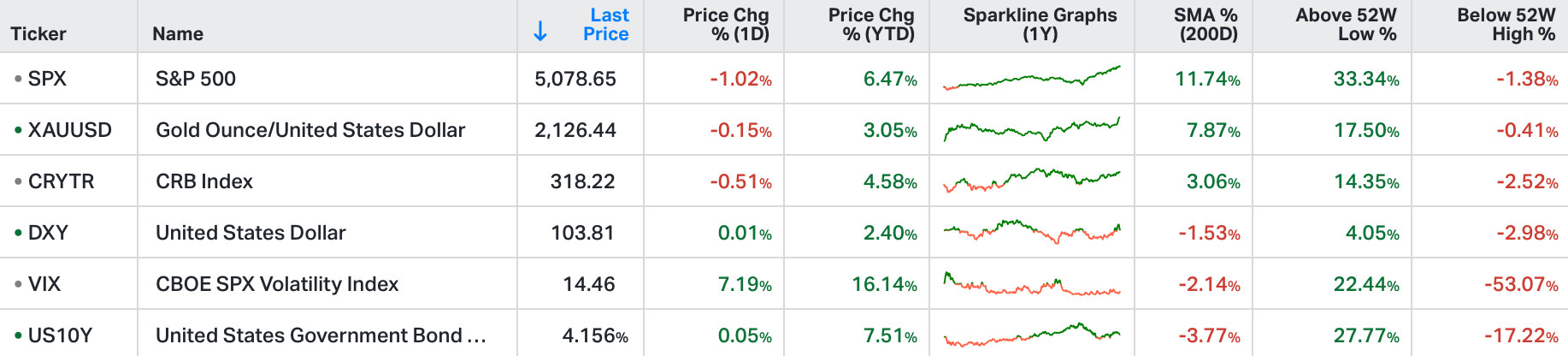

Wall Street’s major averages slid on Tuesday, building on losses from the previous session driven by a widespread sell-off in the technology sector and growing concerns about a potential economic slowdown.

The S&P 500 lost 1%, the Dow Jones plunged 404 points, and the Nasdaq slipped by 1.6%.

Leading the sell-off in tech shares, Apple's stock dropped 2.8% following a report from Counterpoint Research indicating a significant decline in iPhone sales in China during the first six weeks of 2024.

Mecagap stocks were already under pressure, following big gains last week.

Tesla lost 4% and Microsoft (-2.9%), Amazon (-1.9%) and Meta (-1.5%) all ended in the red.

Stocks traded broadly lower, with the Nasdaq leading the downturn - uncharacteristic of late.

Even though it was only down a little more than 2%, and off of record highs of just one day ago, the market behaviour suggested some hedging was taking place (bonds up, the VIX up). That said, by the end of the day, Nvidia had reversed to close in positive territory.

The takeaway: Even the very shallow dip was bought in the most important company in the world (the leader in delivering the technology to power generative AI).

Let's talk about the recent messaging from the Fed, and the events of the next two days …

Jerome Powell will give the first half of his semiannual Congressional testimony today (second half on Thursday). This comes exactly two weeks before the March Fed meeting. We come into this testimony with the interest rate market having dramatically dialled down expectations on interest rate cuts this year.

Remember, in early January, the market was pricing in seven rate cuts (175 basis points) by the end of the year. Now, it's just three.

That swing in the outlook has come from very deliberate perception manipulation by Fed officials. One of the more vocal voting Fed members, the Atlanta Fed President, has been on the media tour projecting only two cuts by year end.

Keep in mind, the Fed has real interest rates (Fed Funds rate minus inflation) at nearly 300 basis points - very tight levels.

Additionally, in December, the Fed projected inflation to be at 2.4% by year end, and to be accompanied by three rate cuts (75 basis points). Inflation is there now, but the Fed has made no progress on reducing interest rates.

That said, Jerome Powell's prepared remarks today will likely repeat the recent mantra of "needing more confidence" in the falling inflation trend, in order to start executing rate cuts. But given the subject matter of Fed speeches in recent days, we should also expect him to talk about the risks to the employment situation, if the Fed stays too tight for too long. After all, they have been mandated by Congress to pursue both price stability AND maximum employment.

As voting member, Austin Goolsbee, recently said, if they stay this restrictive for too long, they will turn one problem (inflation) into another problem (unemployment). Not coincidentally, his colleague at the Fed (and voting member), Adrianna Kugler, addressed just that in a speech this past Friday.

Moreover, we should expect Jerome Powell to address the Fed's balance sheet: discuss when and how to begin the end of quantitative tightening. Not coincidentally, Fed Governor Chris Waller addressed this topic in a recent speech.

With all of the above in mind, it's unlikely that we will hear anything from Jerome Powell that would represent a hawkish surprise for markets. Rather, both the market expectations and the likely subject matter set up for a dovish surprise - which would be fuel for markets.