$Dollar Cycle - Bearish

Macro Perspectives: Mon 10 Jan 22

We ended last week talking about rising interest rates - that has been the theme influencing all markets for the new year.

Importantly, it's not US-centric.

Following on from our discussion(s) last month, when the Fed laid out a timeline for the end of QE and a potential liftoff in rates, it signalled the end of globally coordinated easy money policies. Amongst the biggest shifts in the interest rate market that has come so far, and will likely continue to come, is Europe.

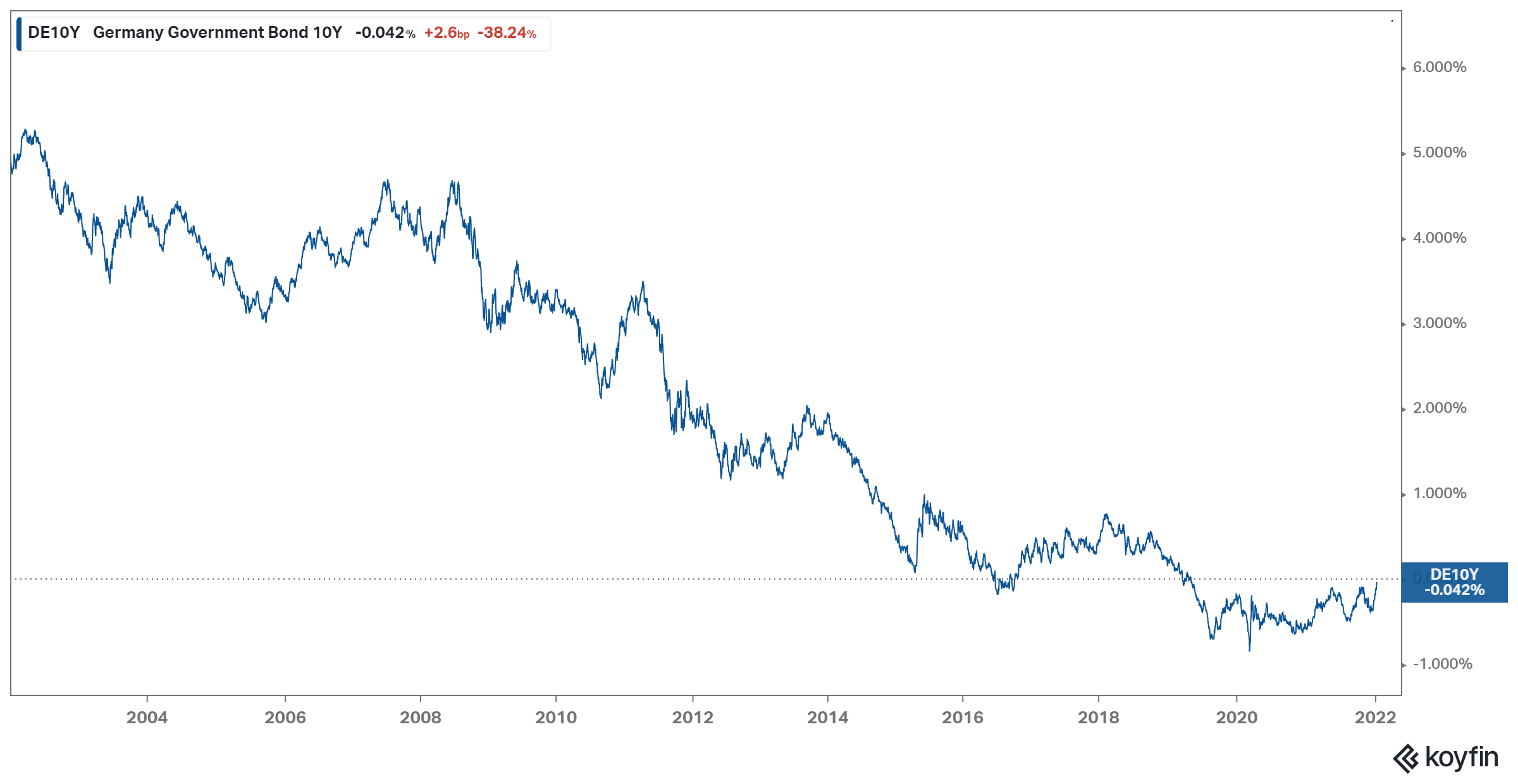

After a near debt-default explosion in Europe ten years ago, and consequently, the near demise of the single currency (the euro), Europe has had three bouts with deflation over the past twelve years. With that, the European Central Bank went bold in 2014, taking interest rates negative - a stimulative policy that forces banks to lend, or pay interest on their excess capital.

This negative rate policy should be coming to an end, quickly - especially after Friday’s (7 Jan 2022) eurozone inflation number...the highest on record

With this, the benchmark German 10-year yield nearly traded into positive yield territory during the day, for the first time in two-and-a-half years (this is bullish for the euro and European equities).

With the above in mind, we opened the week (and new year) talking about the three spots to watch (in addition to a decline in growth stocks): gold, the dollar and bonds.

Thus far, in a world of ultra-accommodative fiscal and monetary policy, still running in the face of hot inflation, bonds have begun the move we should expect (down, interest rates up).

Gold hasn't yet responded. Nor has the dollar.

Friday's inflation data from Europe may be the catalyst to get the dollar moving lower.

As we know, fiat currencies have been devalued over the past two years against asset prices - by the design of the massive fiscal response(s) to the pandemic. But the relative value of major currencies have been stable. That may be changing, and it would be driven by two factors:

1) the U.S. government spending recklessly beyond a rational crisis response,

2) a Fed that denied the inflationary impact of such a fiscal response for too long.

This fundamental case for punishing the dollar would align with the technical (cyclical) case.

We've looked at my chart of the long-term dollar cycles many times.

If we mark the top of the most recent full cycle in early January of 2017, the bull cycle matched the longest cycle in duration (at 8.8 years) and came in just shy of the long-term average performance of the five complete cycles. This means we are now five years into a bear cycle for the dollar, and thus far, it would be the shallowest in performance on record. That would argue the next two years (to complete an average cycle) could be dramatically lower for the dollar, to the tune of a more than 40% decline against major currencies.

That would, of course, align with the outlook for a continuation of a young bull cycle in commodities prices (lower dollar, higher commodities prices).