Did the ECB Intervene before Nvidia beat Bigly?

Macro Perspectives

We had a big move in the interest rate market, starting yesterday with a sharp drop in the vulnerable spots of the European sovereign debt market.

Both Spanish and Italian 10-year yields dropped significantly, even as the U.S. 10-year yield (the global anchor interest rate) traded to new 16-year highs. It's important to note that the European Central Bank was forced to step in, again, and backstop these government bond markets back in June of last year, when;

Italian yields were 4.28% (back in June). Yesterday: 4.41%.

Spanish yields were 3.21% (back in June). Yesterday: 3.75%.

The relief valve in the global interest rate market was pulled. European government bond yields have all reversed around 25 basis points in about 24 hours. And the U.S. 10-year yield has done this (circle) . . .

Is it driven by soft manufacturing data from Europe? Was it driven by the sharp slowdown in U.S. housing turnover in Tuesday’s data? Does it have anything to do with what ECB President Lagarde might say at Jackson Hole on Friday afternoon? Or, did the ECB simply do what they've told us they would do if yields reached levels that created (solvency or liquidity) risk to the euro zone (particularly, the weak spots)?

Probably the latter. Nonetheless, the pressure in the interest rate market may be abating.

Let's talk about Nvidia.

In my Tuesday note ( here ), we talked about the significance of this Nvidia earnings report for markets, as "even more important than Friday's Fed event."

It was three months ago that Nvidia's CEO shocked the world, declaring "the beginning of a major technology era." He had the numbers to back it up - they grew revenues by 19% in Q1 compared to the prior quarter, and they guided to 52% growth for Q2 (shockingly huge). From the "steep" data center demand, they expected revenues to jump from $7.2 billion to $11 billion in just one quarter.

That brings us to today. So how did they do in Q2?

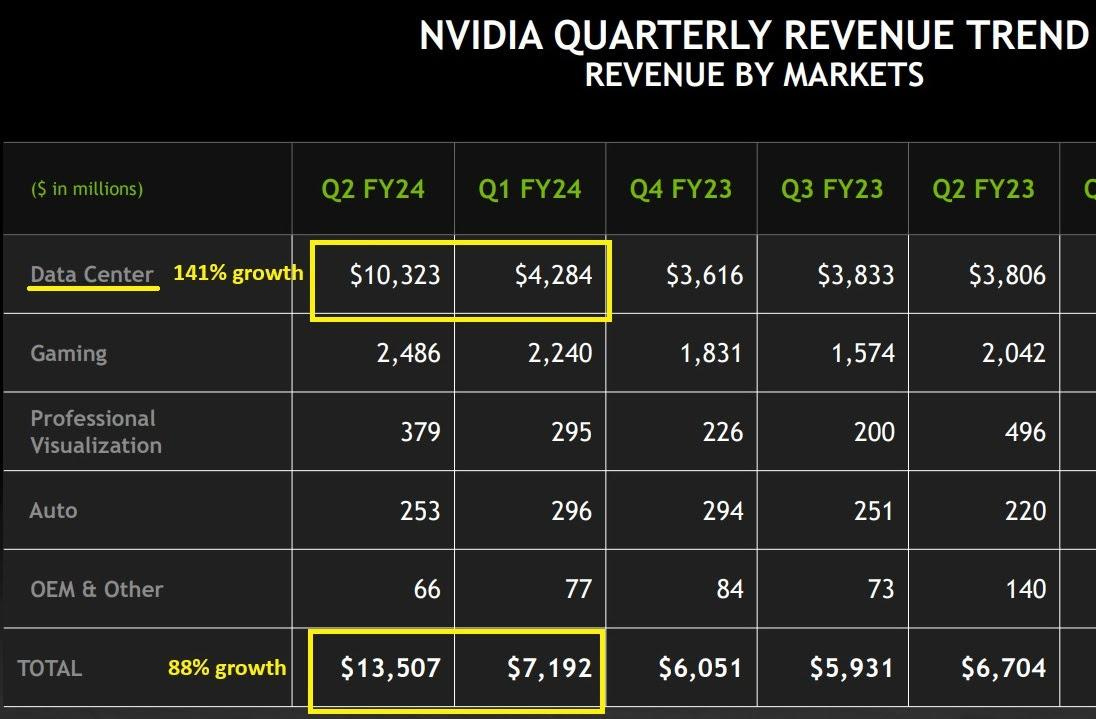

It was another jaw-dropper. They did $13.5 billion in revenue for the second quarter. It was driven by the data center (which more than doubled from Q1). Moreover, they guided revenue of $16 trillion for Q3.

I mentioned after the May earnings report ( here ), it's a "big wake-up call on the massive technological transformation underway (and just in the early stages)." For those that weren't awakened last quarter, this report should do the trick. As you can see in the graphic below, the explosive growth is indeed coming from this data center "retooling."

Keep in mind, Huang has continually been asked how long this demand might last, and he continues to reference this trillion-dollar transition from traditional to accelerated computing. Nvidia has 80% of the market on the GPU chips that power this "retooling." So, even at a $10 billion quarter (in data center revenue), the numbers will get much, much bigger.

It's very early.

With that, even after an 8% move in the stock on earnings, Nvidia became cheaper than it was prior to the report, and cheaper than it was prior to the Q1 report, on a multiple of revenue (price/sales).

Going into that May Nvidia earnings report ( here ), my thoughts were:

More on AI . . . My view: The automobile is to mobility, as AI is to productivity.

A productivity boom is coming, and it is well needed.

Productivity growth is the key to improving living standards. As ChatGPT says, "sustained productivity growth of around 2% per year has historically been associated with positive economic outcomes and improvements in living standards."

We averaged just 1% for the decade prior to the pandemic, and negative 0.7% since the fourth quarter of 2020.

Just as the 1920s were defined by innovation (the automobile and widespread access to electricity), we have the formula here for another "roaring 20s."

Huang said that he expects companies to realize trillions of dollars of productivity gains, from generative AI