Interest Rate Hike Cycle at an End?

Macro Perspectives

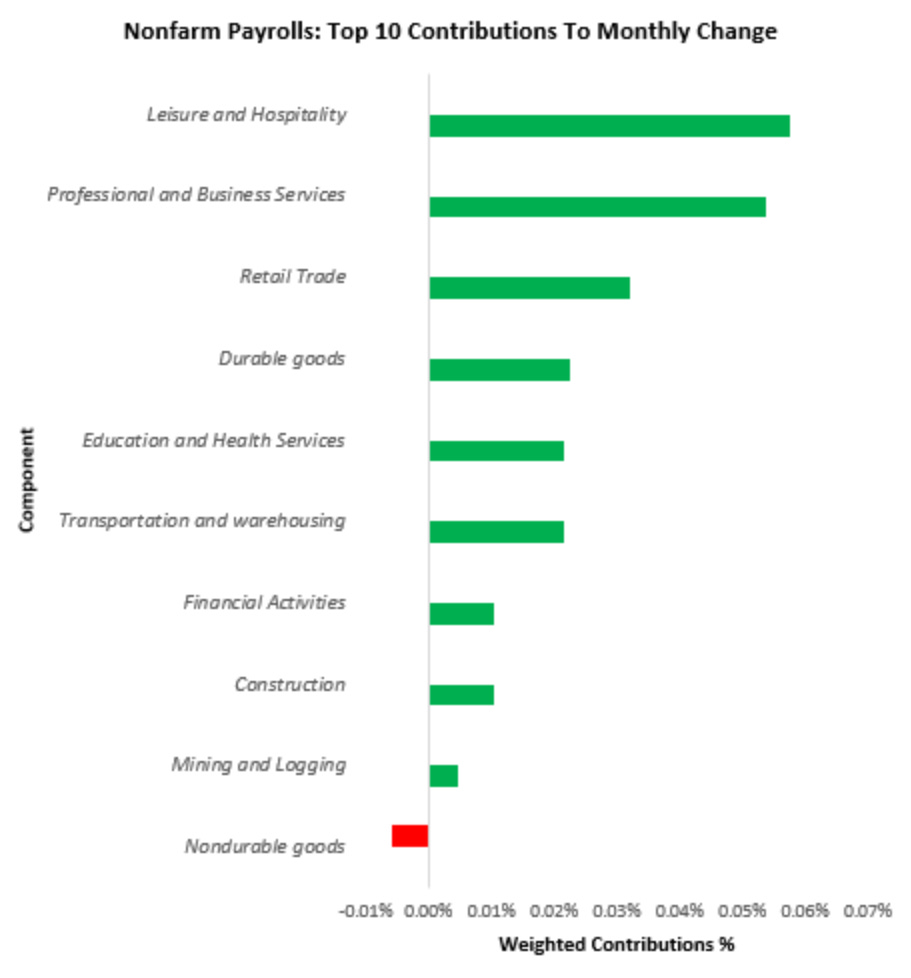

Following our conversation last Thursday, the Fed has been focused on loosening up the jobs market, as a means to relieve inflation pressures.

The report released Friday morning on the August employment situation is a key input in the Fed's "data-dependent" decision-making process (on rates).

So, what did the report say?

Unemployment ticked up.

Hours worked ticked down.

The monthly change in wages was modest.

That's all going in the direction of a cooling employment situation

The next big data points will be;

September 13th: We'll get the August inflation data, which should be on the decline (given the sharp fall in gas prices last month).

September 21st: We'll get the next Fed decision on rates.

The data is telling us that the exuberance in the economy has exhausted and inflation is softening - thus we should expect the Fed to be at or near the end of this rate hiking cycle.

What could be a catalyst to not only end this cycle, but to reverse it?

Europe.

As we’ve discussed previously, the European Commission has threatened to intervene in the energy market, to offset skyrocketing energy prices in Europe with government subsidies.

Related to that effort, G7 countries are stepping up threats to put price caps on Russian energy exports, shown below, (capping the price at which they would pay). Meanwhile, Putin is responding by taking the Nordstream 1 pipeline offline, indefinitely (for "maintenance").

The Western world thinks they can starve Putin of revenue. Putin thinks he can starve Europe (particularly Germany) of energy.

The energy void is unlikely to be filled by OPEC. Iran? We will see.

Nonetheless, it looks like a lose-lose scenario may be approaching, if not here. Cutting more fossil fuel supply, into a structural global shortage, would mean higher prices. And if governments want to subsidize energy, they will do so at the expense of solvency.

PS: If you, or someone you know, would like to out perform the market with an institutional approach, subscribe below.