Could the BOJ act next week?

Macro Perspectives

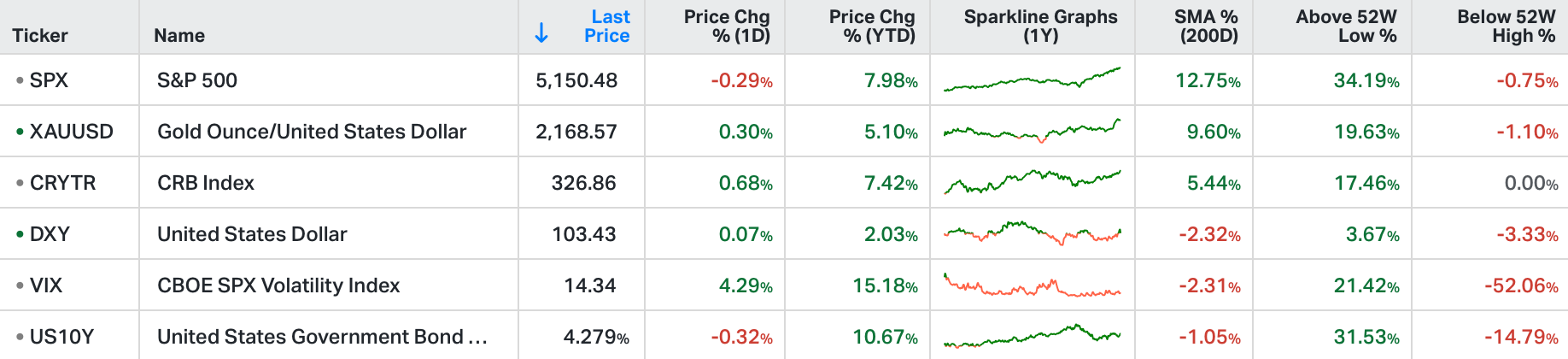

US stocks were sharply lower in the final trading hour on Thursday, reacting to another set of higher-than-expected inflation data that pushed yields higher.

Investors were questioning the timing of the interest rate cuts and its effect on the stock market rally.

Producer prices rose more than expected last month and initial claims unexpectedly declined, but retail sales disappointed.

Real estate, utilities and health were the worst performers while the energy sector managed to stay in the green after oil prices reached to a 4-month high level.

On the corporate front, Nvidia lost about 4% and Tesla fell 5% after a Wells Fargo analyst said there’ll be zero growth in sales volumes for the electric-vehicle maker this year.

Stocks were broadly down, globally. Bonds were down, globally (yields up). Most commodities (excluding energy) were down.

The selling was largely attributed to hotter than expected producer prices in February (another inflation data point), whilst retail sales for February "rebounded."

Does that mean the Fed's going to push the beginning of rate cuts out further. Does it mean they won't cut? Does it mean that they might return to the view of raising rates again?

None of the above. Keep in mind, the producer price index has been under 2% (year-over-year change) for ten consecutive months. The "rebounding" retail sales, rebounded from a contraction in January, which was revised even lower in yesterday’s report.

So, for perspective, if we look at where we are today, compared to where we were going into last Friday's jobs report: The market has simply priced out a small possibility of a fourth rate cut this year.

Remember, the market view in early January was for six quarter point rate cuts this year (with a small chance of seven), while the Fed had projected just three. Over the past two months, the Fed has successfully manipulated the market view to align with the Fed's projections of just three quarter point cuts this year.

That's where we stand heading into next Wednesday's Fed meeting, where the biggest news will likely be, what numbers the nineteen meeting participants determine to go in these yellow boxes (projections of PCE inflation and the end of year Fed funds rate).

We head into this Fed meeting with most advanced economies in the world preparing to cut interest rates (ease monetary policy) after the fight with four decade high inflation. We should expect them to do it in coordination, as they did with the response to the pandemic, and with the response to the related inflation.

In coordination, the major global central banks were able to curtail record inflation, without having to raise interest rates above the rate of inflation - the historical inflation beating formula, but also a formula that would have crippled the economies of the Western world.

That victory over inflation has only been made possible by the liquidity that continued to pump into the global economy from Japan.

With that, there has been a clear effort from the Bank of Japan (BOJ), over the past several months, to start setting expectations in markets that they will, at some point, exit emergency level policies. Communication to markets has been dialled up in recent days, telegraphing the end of negative interest rates in Japan.

The rumours now are that it could come as early as next week's BOJ meeting.

Negative rates and QE in Japan have been the BOJ and Japanese government's strategy to fight decades of entrenched deflation. Only with the post-pandemic global ballooning of money supply, might they have it beat. But an exit at this point seems premature, unnecessary, and (possibly) dangerous.

What's dangerous about it? Japan's negative rates (and unlimited QE) have promoted (implicit and explicit) investment into global stock and bond markets. Importantly, the BOJ bought a lot of sovereign debt of the Western world to help keep important global rates in check, while central banks were fighting inflation.

With that in mind, while the U.S. inflation data got a lot of attention, it was another report that likely triggered the sell-off in stocks, and this spike (below) in yields. News was circulating that the BOJ could act as early as next week.