Yesterday we talked about the latest hot inflation data. The increase in prices (CPI) from September to October was 0.9% - that's the second time in the past six months that the month-over-month reading has measured that high.

Again, if we extrapolate out that 0.9% monthly inflation number to an annual rate, it would project double-digit inflation.

Additionally, we have plenty of drivers at work, and new drivers being introduced (like more fiscal spending), that will only increase the rate at which prices are rising.

With that, let's revisit a couple of key inflation hedges, to see how these markets are responding. First, gold...

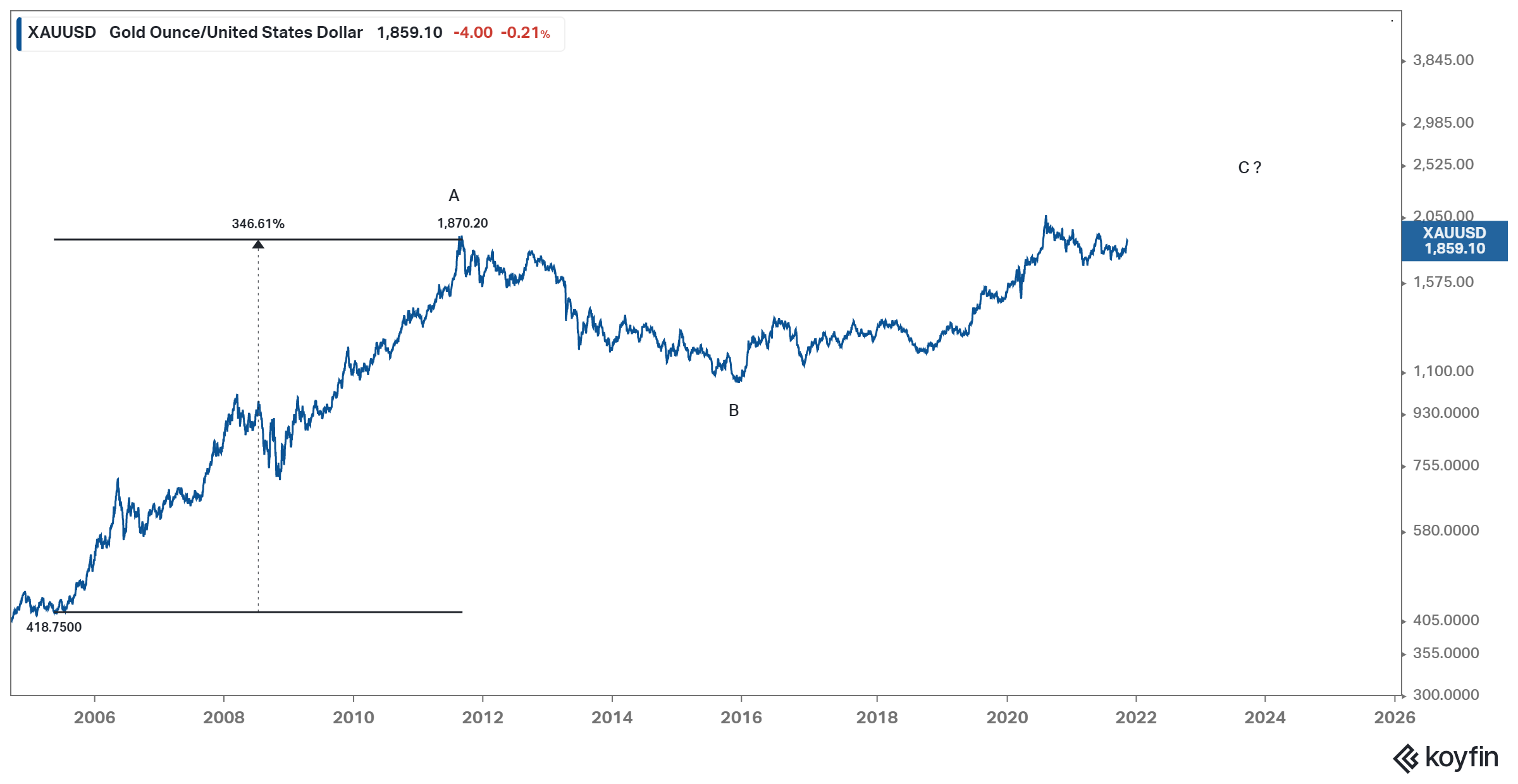

We've looked at gold quite a bit in my daily notes - this is the historically favored inflation hedge. Despite the hottest inflation we've seen in decades, gold is down for the year (still). As you can see in the chart, when the inflation data hit yesterday, gold broke out of this technical downtrend.

If we look at a longer-term chart, you can see that this technical downtrend looks more like a short-term correction in a long-term bull market. For those that appreciate the value of technical analysis, this ABC pattern (from Elliott Wave theory) projects a move to $2,700.

Now, let's look at copper…

Unlike gold, copper is up on the year, big (+25%). It's winning on two fronts: 1) an inflation hedge, and 2) copper plays a key role in renewable energy (from solar, to wind, to electric vehicles). The upside case for copper (from here) remains very strong.

As you can see in the chart, we've had these types of moves in the price of copper. If this recent run is on par with the history of the past two decades, copper has at least another 25% upside ($5.50), and a move towards $7 comes into sight.

The producers of copper, who know the supply/demand dynamics better than anyone, think prices will go well beyond the projection in my chart.

Here's how the CEO of one of the largest copper producers in the world put it, on an earnings call earlier this year:

"China has been the driver of copper demand growth over the past two decades. Now the source of new demand is expanding...copper is essential to the transition to a global clean energy future. Roughly 70% of copper is used to deliver electricity. As clean energy initiatives are implemented, copper intensity in the economy expands in a major way. The outlook for copper has never been better. Significant demand growth is inevitable. Supply to meet this growth is severely challenged. It's going to require meaningfully higher prices to support mine investment. The combination of rising demand, scarcity of new supplies point to large impending structural deficits, supporting much higher copper prices than previously anticipated."