Coordinated Rate Cuts

Wall Street major indices closed firmly higher on Wednesday, driven by a tech rally led by AI-darling Nvidia, amid optimism that the Federal Reserve might lower interest rates later this year after slightly weak labor market data.

The stock is up over 140% this year and 200% over the last year.

The S&P 500 and the Nasdaq 100 jumped to record highs, adding 1.2% and 2%, respectively, and the Dow finished 96 points higher.

Other chip makers also outperformed, with TSMC (6.8%), Broadcom (6.2%), AMD (3.8%), Qualcomm (3.7%), Micron Tech (5.6%) and Intel (2.5%) all closing sharply higher.

On the data front, the ADP report showed that private businesses added fewer jobs than expected, in line with other data that points to a softening, albeit healthy labor market.

Back in March ( Cycles to Materialise ) we discussed the Swiss National Bank's surprise quarter point rate cut.

"if there were doubt on whether or not this easing cycle would materialise, there shouldn't be now."

The major central banks of the world had coordinated closely throughout the crises of the past 15 years. They all went to ultra-easy emergency level policies in response to the pandemic, and then all (exception Japan) took interest rates ABOVE the rate of inflation (restrictive territory).

And as we discussed back in that March note, we should expect them to all be cutting rates, in coordination, in the coming months, mostly to ensure that global liquidity doesn't become too tight, and (related) that their respective government bond yields (borrowing rates) don't run away (higher).

We've since had the beginning of the easing cycle in Sweden. And yesterday morning, in Canada (with a quarter point cut from the Bank of Canada).

And this morning (I write my notes at 07:00 CET), the European Central Bank should be cutting rates, after taking rates up 450 basis points in fourteen months.

That leaves the Bank of England, which has perhaps the easiest case to make for cutting rates at its June 20 meeting.

And, of course, the Fed meets next Wednesday.

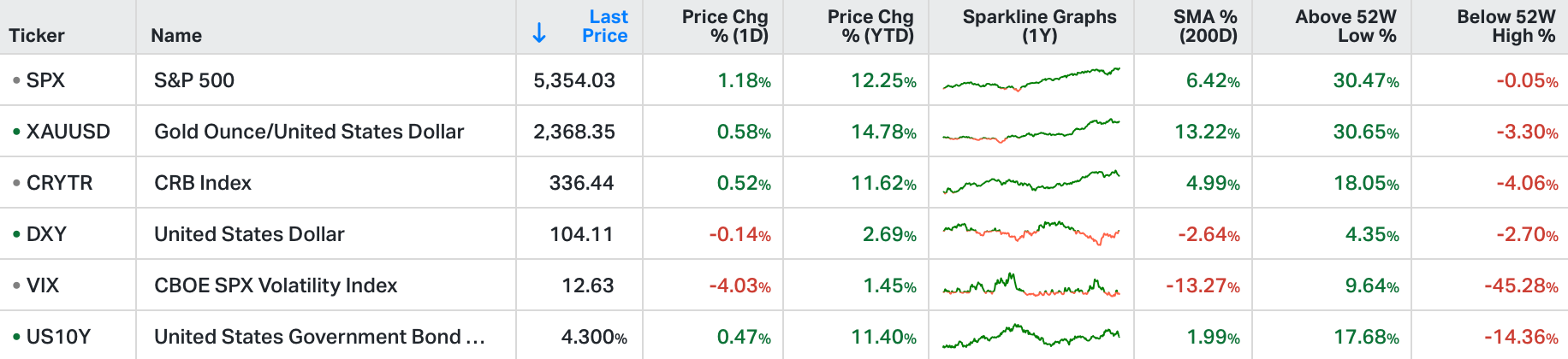

Is the market getting the message on the easing cycle? Stocks are back on record highs, the U.S. 10-year yield is down 36 basis points in five days!

As you can see in the chart, yesterday it traded below the levels of the May 15th CPI report (April inflation) - 4.28% on the 10-year is the lowest level since April 1st.

That was the Monday after the Good Friday PCE report (where the market re-opened to digest the report). Both of those prior inflation reports took yields higher. The recent PCE report has resulted in lower yields.

ps: Today is our - Sweden’s - National Day. To celebrate, yearly memberships to GRYNING AI will be automatically upgraded to two years.

I guess the question remains, is inflation truly beaten. I know many are certain, but I do not see it, and I fear that even the Europeans will find that "the last mile" to 2% is going to be very tough. I continue to believe that they will simply ignore inflation and let it run hot in order to cut rates, but I do believe the Fed will cut at least once this year.