Following last week's economic data, the interest rate market is now expecting the Fed to hold steady on rates, when it meets on September 20th.

That should be good news for stocks. It was, for much of Friday. Yesterday, not as much - that's mostly because of what's happening here . . .

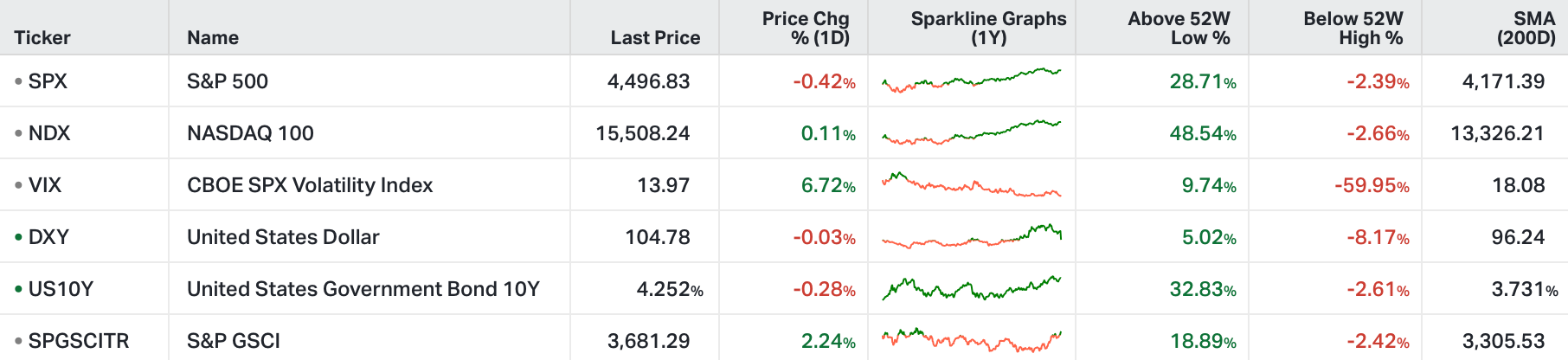

This is a chart of the U.S. 10-year yield - heading into the jobs report this past Friday, this important barometer on global interest rates was falling back toward 4% (trajectory denoted by the red line).

The fall in rates was driven by softening U.S. economic data, and the expectation that Friday's jobs report would (further) confirm that inflation pressure from the labor market was being choked off.

The jobs report delivered, on that front. But the interest rate market did an about face, and as of yesterday afternoon was UP 20 basis points from Friday's low.

What's going on? Remember, the Fed has claimed to be "data dependent" in determining the rate path from here. They've been looking for softening data to validate a pause, if not the end of the tightening cycle.

They've gotten it.

With that, most would expect some relief in the interest rate market (which would translate into some welcome relief in consumer rates).

We've gotten the opposite, thus far. Is the cooling in the data too perfect? Cool enough for the Fed to hold rates steady here, but not cool enough for the recession doomers to feel confident (any longer) in a big rate cutting campaign next year.

The interest rate markets seem to be adjusting for that picture.