Central Bank Coordination is Bullish

Macro Perspectives

If you're a hedge fund or trader, and you're leveraged 10, 20, 50, avoiding corrections or trend changes is critical to your survival.

Getting it wrong can mean your portfolio blows up and maybe goes to zero. That's the mentality the media is speaking to, and frankly, much of Wall Street, when addressing any market decline.

The bottom line: 99.9% of investors aren’t leveraged and shouldn't be overly concerned with U.S. stock market declines, other than saying to themselves: “Do I have cash I can put to work at these cheaper prices? And, where should I put that cash to work?”

So, for the average investor, dips are an opportunity to buy stocks at a discount.

Warren Buffett has made a career out of "being greedy while others are fearful." And there is certainly a lot of fear in the air. Buffett's successor, Greg Abel, was buying Berkshire Hathaway shares last Thursday. He bought 168 shares at an average price of around $406,000 a share-that's over $68 million worth of stock and about 15% of his net worth if the Forbes net worth estimates are anything to go by.

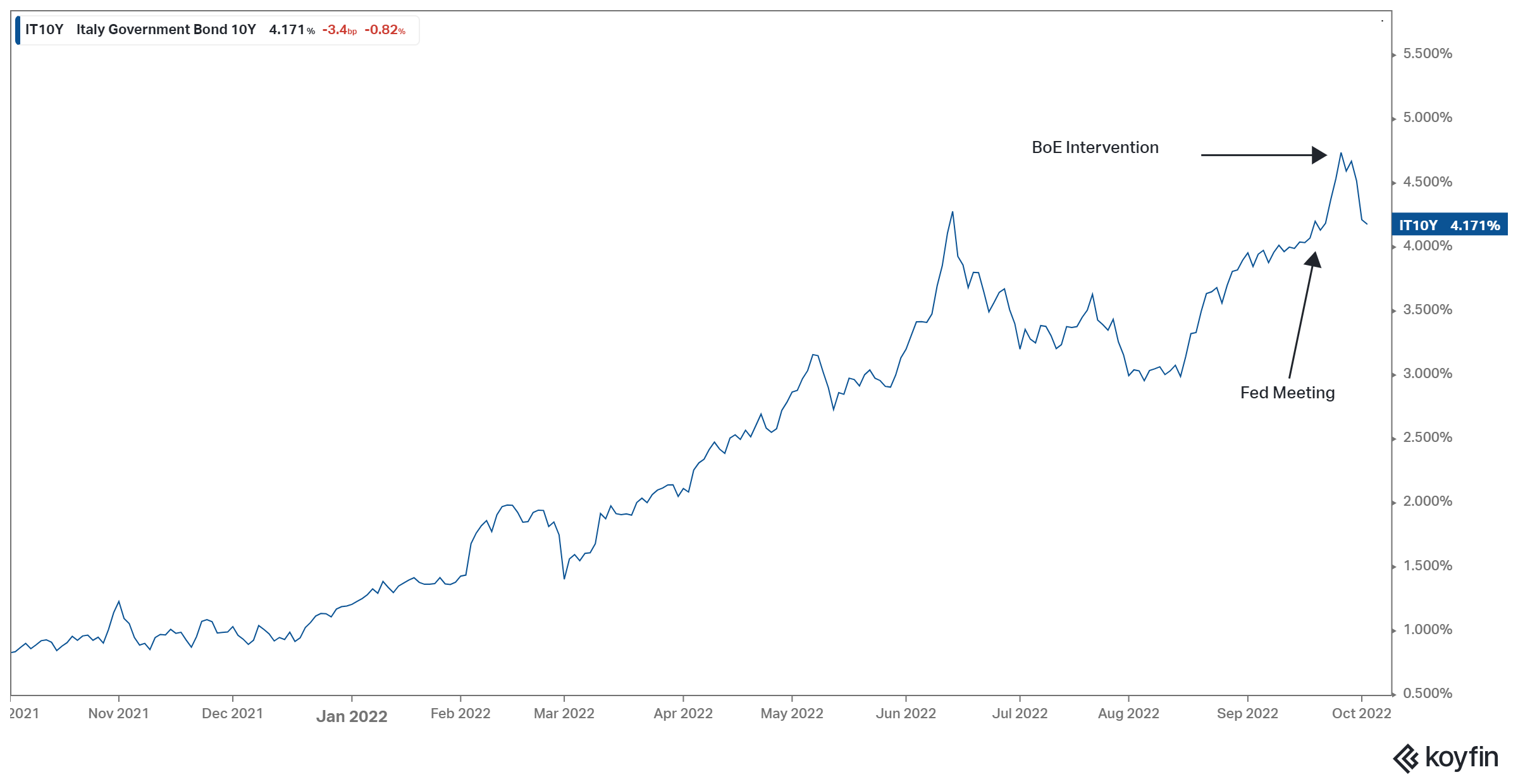

This purchase came the day after the Bank of England intervened to calm the UK bond market.

If we look back through history, major turning points in markets have often been the result of some form of intervention (i.e., policy action or adjustment). So far, the action taken by the BOE has done the trick for the vulnerable government bond market:

Yields on 10-year UK gilts are down 65 basis points from Wednesday's high, back under 4%.

U.S. yields are down 38 basis points.

Italian (the most imminently dangerous major global government bond market) yields are down 73 basis points from Wednesday's high.

This calming in the global sovereign debt markets has translated into higher stocks.

We start the week with a strong reversal in stocks, after making new lows on the year (and another technical reversal signal signal, this time in S&P 500 futures, Dow futures, and Nasdaq futures).

That said, let's get back to the overhang of "fear" in markets…

There were rumors going around all weekend that a major global bank was on the verge of failing—Credit Suisse. The CEO wrote a memo to staff on Friday, assuring them of the liquidity and strong capital base of the bank, although they are restructuring. Still, the market has been placing bets on its failure, and another "Lehman moment" for the world—where the failure of a major global trading bank can quickly result in a freeze of global credit.

Allow me to digress: the 20 to 25% (251 bps in image below) default probability that is being thrown around in the media conveniently, for the headline makers, leaves out the 5 year time span.

Additionally, CET1 capital adequacy was at 13.5% - within the bank's own target and above the 10% Swiss hurdle. During 2008, 5%< CET1s were common place.

For the sake of variety, Morgan Stanley CDS in 2011-2012 was twice as wide as Credit Suisse is today.

Lastly, those of you that want to mess around with CDS calculations (click here).

Note: Change D20 to 40% and D24 to 2.5%. Set LIBOR (D22) to 0% for ease. Assume B12:B16 are constant. Find the values such that E71 is zero.

Keep in mind, the effects of the global financial crisis have left a bias in market participants-they have for the past 14 years seen crashes everywhere.

Whilst at times the fundamentals may justify the view, there is a big difference between now (into perpetuity) and 2008-there is no question what central banks can and will do.

To avert disaster in the global financial crisis, they ripped up the rule books. There are no longer any rules of engagement for central banks. They will do "whatever it takes" to maintain financial stability and to manufacture their desired outcome. This comes with one very important condition: the "no rules" era of central banking requires coordination among the major global central banks... and they are coordinating.