We had the December jobs report on Friday morning.

The labor market remained tight last month, despite a Fed that has been verbally attacking jobs for the better part of the past year.

Why does the Fed want to induce a softer job market? Wages.

In a labor supply shortage, employees should have leverage in negotiating higher wages, particularly in what has been a hot inflation environment. The Fed fears an upward spiral in wages, where wages feed into higher prices, which feeds into higher wages ... and so the self-reinforcing cycle goes.

It hasn't happened. Wages have well lagged the inflation of the past year, and the wage component of the December jobs report showed no signs of trouble with wage growth.

How did markets react? Yields fell sharply. Stocks were up big.

But much of the action in the markets was driven, not by jobs, but by another December report that came later in the morning.

The ISM services report showed a contraction in business activity in December, after 30 consecutive months of growth.

The last two times the services industry contracted;

Covid.

Great Financial Crisis.

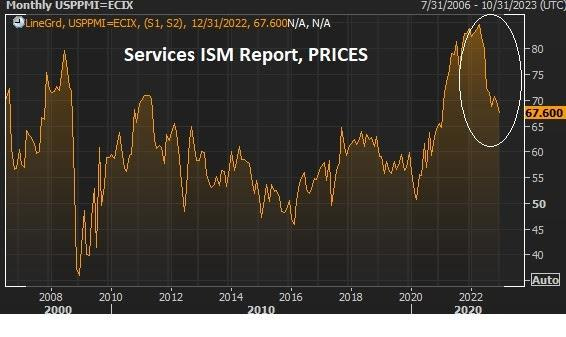

Related to this, take a look at the chart of services prices from the morning's report ...

This is important: While goods prices and energy prices have been falling in the government's inflation report, it has been services prices that have been persistently hot - that has been the Fed's rationale for "keeping at" the inflation fight.

As we've said here in my daily notes, the real-time data has been telling us for months that those services prices have been rolling over. It just hasn't been reflected yet in the stale government inflation report. This chart above supports that view.

With that, the bond market is telling us that the Fed that has overdone it on rates, already.

The Gryning Portfolio offers actionable insights with the goal of focusing solely on what matters in order to make money trading global financial markets. Join below, it’s less than a coffee a day!