Bond & Yields . . . US, ECB & BOJ

Macro Perspectives

Stocks followed a rout Tuesday, with some relative calm yesterday.

That came, in part, because of some relative calming in the treasury market. Let's talk about why … First, let's take a look at the U.S. 10-year government bond yield.

Following the inflation report, the U.S. 10-year yields traded just two basis points shy of the June high of 3.5%. Back in June, this 3.5% level was a big deal, for this reason: It put upward pressure on global interest rates.

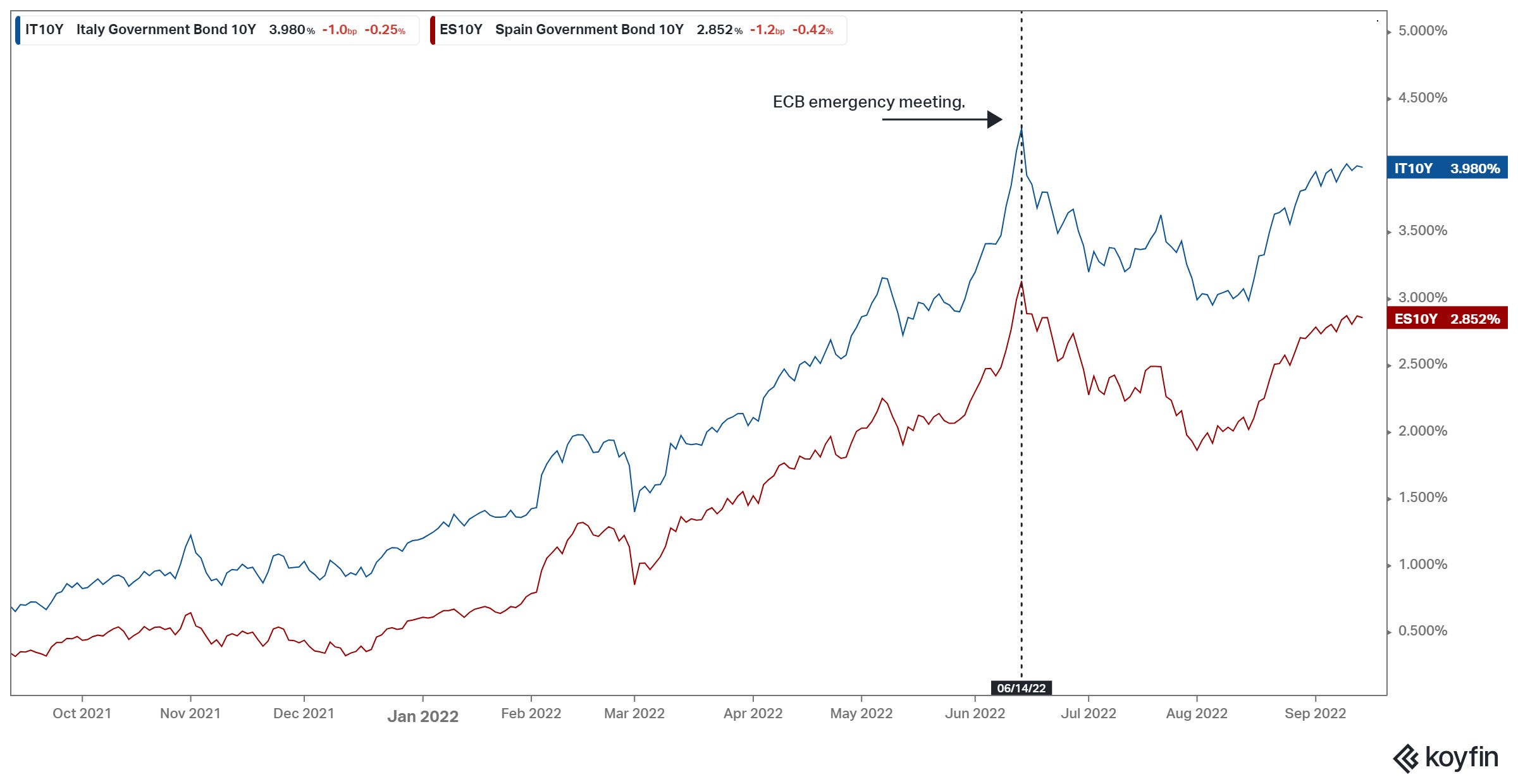

This includes the fiscally fragile countries in the eurozone - the two most vulnerable countries in Europe to rising interest rates, are Italy and Spain. These were the two sore spots back in 2012 that nearly triggered a contagion of sovereign debt defaults and an implosion of the euro (the second most widely held currency in the world).

The fiscal position for both countries is worse now, not better.

And at a 3.5% 10-year yield in the U.S, back in June, Italian yields ran up to 4.28% with Spanish yields ran up to 3.21%. That was the danger zone. With that in mind, here's what Italian and Spanish yields look like today ...

Italian bond yields traded up to 4.09%. When yields were in this territory back in June, the ECB responded with an emergency meeting - they crafted a game plan to defend against the rise of these vulnerable eurozone sovereign debt yields. It was a new QE plan, by a different name (the "Transmission Protection Instrument").

So, we should expect these levels (or near here) to force the ECB back into the game of bond buying.

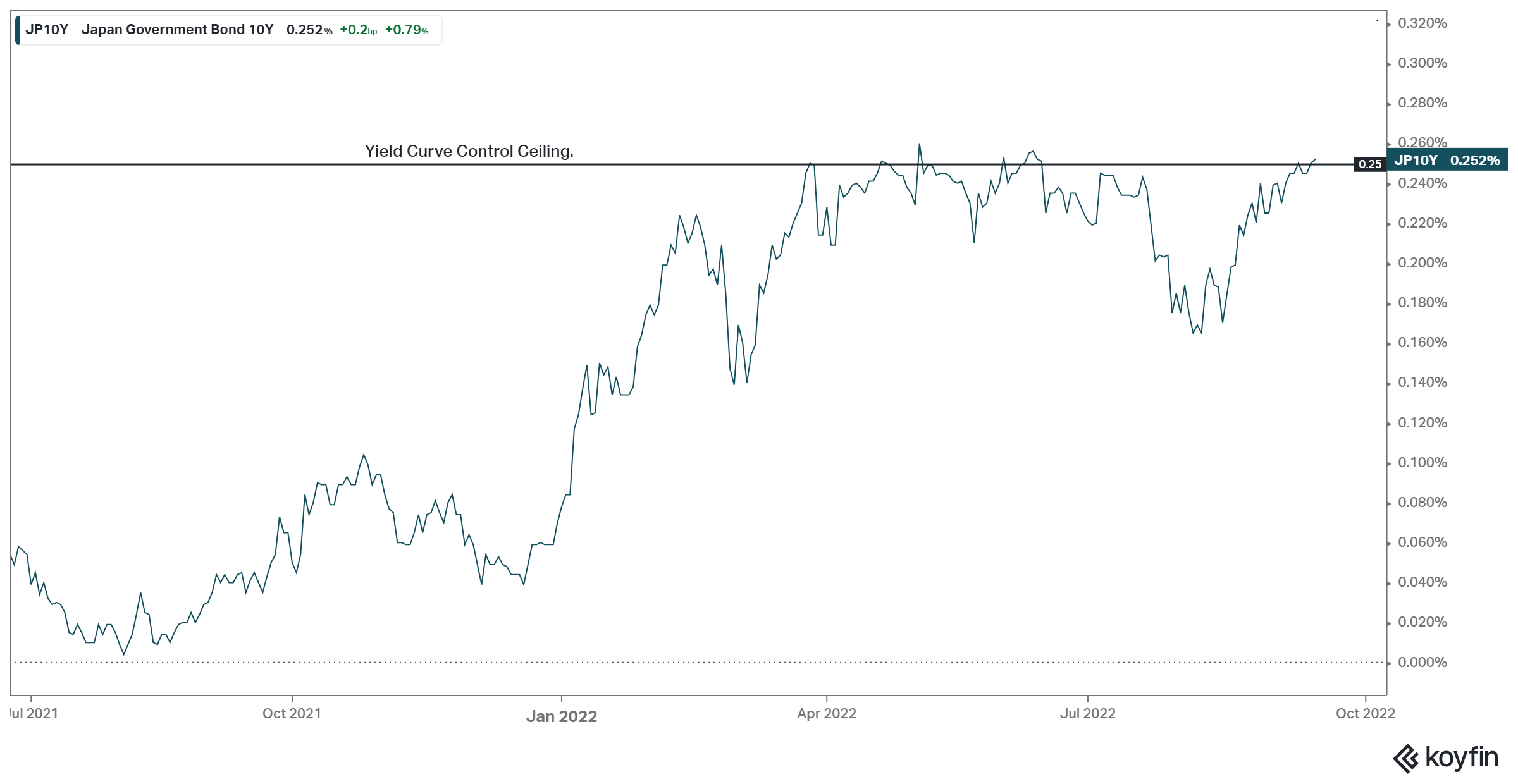

This level in the U.S. 10-year yield has also put upward pressure on Japanese bond yields. Why does that matter? Because the Bank of Japan is defending a cap on their yields, through their "yield curve control" program. Similar to above and similar to June, Japanese yields are again bumping into the top side of their acceptable range (0% yield, with 25 basis points on either side).

What does the Bank of Japan do when JGB yields are hitting their yield curve control ceiling (of 25 basis points)? They print yen, and buy unlimited amounts of JGBs, to push bond prices higher, yields lower.

So, as we discussed yesterday, despite the perceived "normalization of monetary policy" being led by the Fed, we still have two (very powerful) central banks in the position to defend against shocks, and pump liquidity into the global economy.

This building scenario supports the point we've discussed all along: QE is like Hotel California, "You can check out, but you can never leave."

PS: If you, or someone you know, would like to better align yourself with the market - join us below for less than the price of a coffee a day.