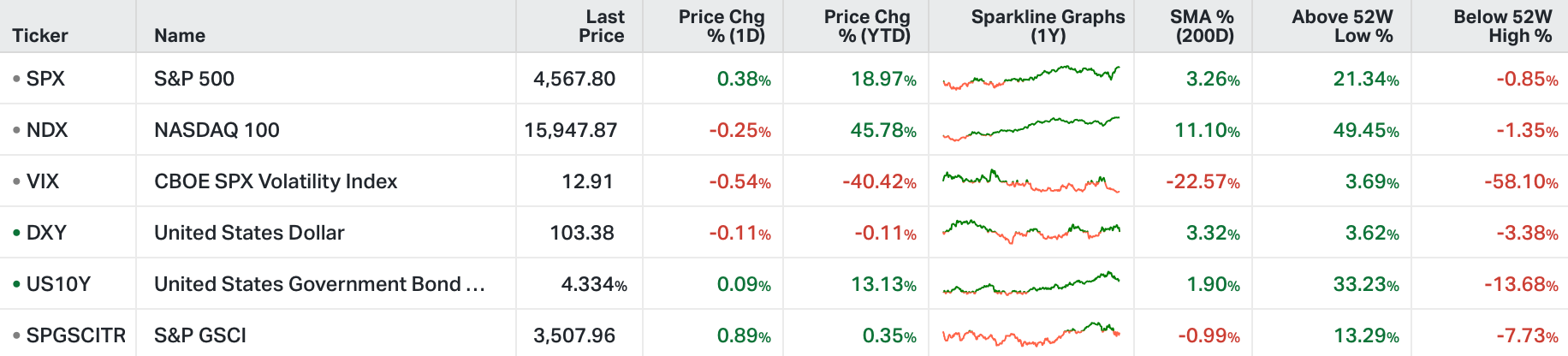

We had the report on the Fed's favored inflation gauge, core PCE - it confirmed the continuation of a steady decline, with a fall to 3.5% year-over-year change.

The Fed has historically beat inflation by taking interest rates above the rate of inflation. If we measure that by the Fed Funds rate (interest rate) against core PCE (inflation rate), the Fed has been there (above inflation) since March. That "restrictive monetary policy" position puts downward pressure on inflation, and economic activity.

As we discussed on Tuesday, as inflation continues to fall, the level of restriction rises (i.e. real rates rise).

With that said, we'll hear from Jerome Powell today. He's speaking at an event at Spelman College. We should expect him to comment on the sharp slide in bond yields since the Fed's last meeting, particularly because it was the preceding sharp rise in bond yields that gave the Fed pause on doing more.

Does it mean he will convince markets that a December hike is back in play? Highly unlikely. The reality of rising real rates, and an economy running at a much more modest rate in Q4, relative to Q3, should keep the market focused on aggressive rate cuts next year.

Let's talk about the big tech stocks . . .

Last month, we talked about the technical reversal signals that were flashing in the interest rate market. First it was the 2-year Treasury yield, then the 10-year, then the big corporate bond and Treasury bond ETFs - that indeed predicted the turn in the bond market.

Now we have a reversal signal (yellow box in chart below - “outside day”) in big tech stocks. It came in Microsoft, at the record highs . . .

We have the same signal (yesterday) in Google, Apple and Meta.

Is this a predictor of some regulatory uncertainty (brakes) to come, related to AI? Maybe.

It comes as these stocks are up 80% on the year, as an equal-weighted basket. Meanwhile the equal-weighted S&P is up less than 5% on the year. Small cap stocks are up just 3%.

This looks like a rotation out of big tech, and into value.